Cite report

IEA (2021), Cross-Border Electricity Trading for Tajikistan: A Roadmap, IEA, Paris https://www.iea.org/reports/cross-border-electricity-trading-for-tajikistan-a-roadmap, Licence: CC BY 4.0

Report options

Opportunities for electricity trade

In this section we consider Tajikistan’s opportunities for electricity trade with neighbouring countries. The main features assessed are demand patterns, prevailing cost of generation and infrastructure requirements.

- Demand patterns are favourable if they are complementary to Tajikistan’s seasonal profile of summer surpluses and winter shortages.

- A high prevailing cost of generation in a neighbouring country increases the favourability for exports, whereas a low prevailing cost of generation provides opportunity for imports. The estimated average marginal cost of generating electricity in Tajikistan is USD 6/MWh (RTE and ADB, 2020).

- Infrastructure requirements such as new transmission interconnections can significantly prolong the commencement of trading, given the financial challenges of the country.

The potential degree of integration that could be feasible between Tajikistan and its different neighbours in the next ten years is assessed. Ultimately of course, these are choices to be made by the relevant stakeholders and their perception of trade opportunities and risks relative to their respective resources.

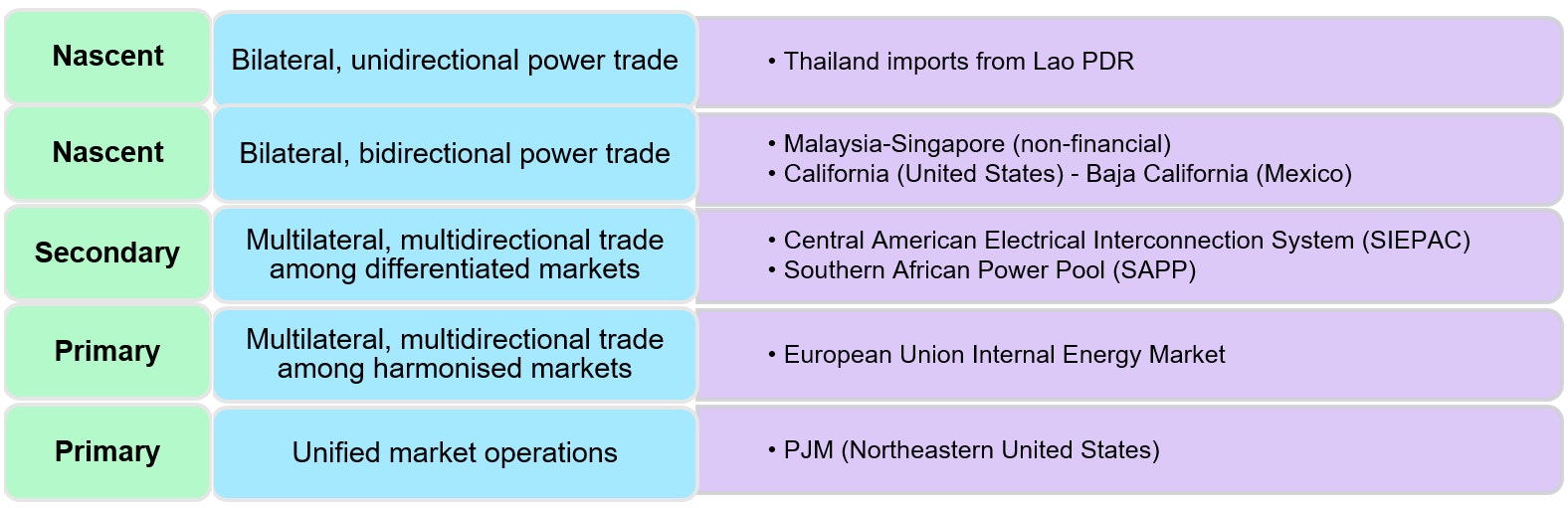

The figure below shows a hierarchy of power system integration models. These vary from ones that are very limited, e.g. the simplest model being unidirectional power trading, to ones that can be considered complete. The fully integrated model is represented by the PJM system in the United States, which organises markets, supports transmission planning and manages generator dispatch across a wide geographic area that includes multiple jurisdictions. Different models require varying levels of cross-border collaboration and resource sharing, from low levels in bilateral trade models to high levels in more unified models.1

Degrees Of Cross Border Power System Integration From Limited To Complete

Open

{kind=link}

Higher degrees of integration generally allow for more optimal use of common resources such as transmission grids, thereby shortening the payback periods and maximising the economic outcome for the participants.

- Nascent trading arrangements such as bilateral trading arrangements are between two countries. In this model, often each trade is negotiated separately, and hence the volume of trade and the margins need to be sufficient to cover high transaction costs and to justify any required grid investment. Where transmission infrastructure exists, a market arrangement can be developed relatively quickly as it does not require high degrees of harmonisation.

- Secondary trading is a model in which domestic electricity markets are cleared first using respective domestic generation with any surplus or deficit traded and balanced with the trading partners. It requires a higher degree of system harmonisation and political agreement among participants although it does not require the same domestic market structures. Examples of a secondary market are the Southern Africa Power Pool and the Central American Electrical Interconnection System.

- Primary trading is a model in which a multilateral market is the main platform for trade. Primary trading arrangements require participants to restructure and harmonise domestic frameworks, such that all generators and consumers have equal status across boundaries. Examples of primary arrangements are PJM in the United States and the European Union Internal Energy Market. This arrangement requires high levels of co-ordination and political agreement among the various jurisdictions.

Multilateral trades can coexist alongside other differentiated (market or non-market) arrangements such as long-term power purchase agreements (PPAs) or non-financial power exchanges, wherein the participants are not restricted from such choices. A common feature among these models is third-party access to the domestic grid, so that any generator can directly supply a demand in another jurisdiction for a defined trading period. The assessment of a likely degree of integration depends on the common economic and political interest among the countries.

Multilateral trade in the near term in Central Asia

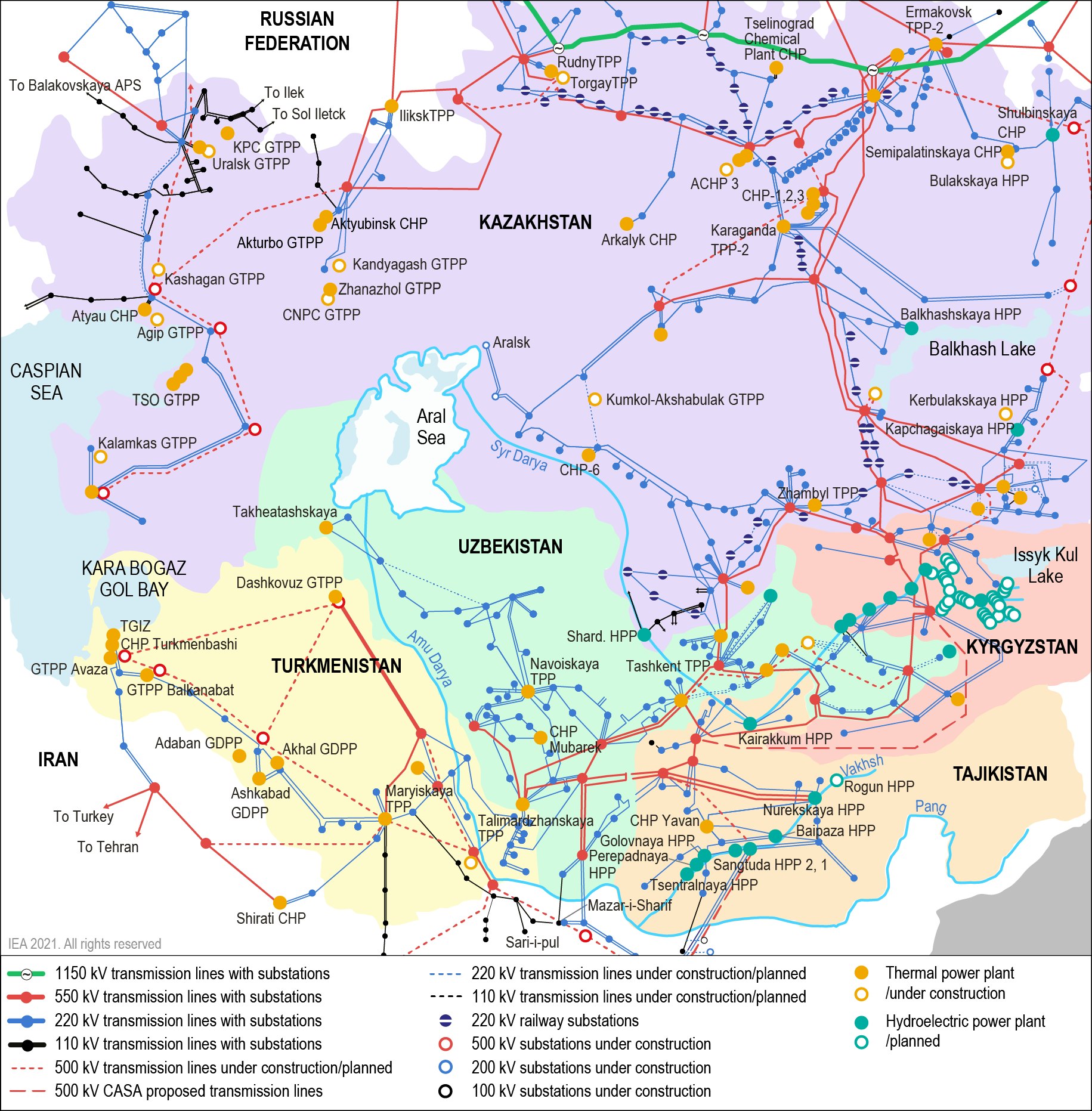

Historically Tajikistan was connected to the other Central Asia2 countries as part of the Central Asian Power System (CAPS) which was built during the Soviet era. The system was slowly abandoned in the 2000s as Turkmenistan disconnected in 2003 for more favourable trading arrangements with Iran, and in 2009 when Kazakhstan and Uzbekistan withdrew, and Tajikistan was cut-off due to transit disputes and disagreements on system usage. There have been several initiatives to resolve these disputes. Tajikistan reconnected to CAPS in 2018 and started electricity trade with Uzbekistan. Initiatives stemming from the Central Asia Regional Economic Cooperation (CAREC) programme by the Asian Development Bank (ADB) and the Central Asia Regional Electricity Market (CAREM) by the US Agency for International Development aim to re-establish co-operation by addressing common concerns such as energy security, water rights, and financial viability and technical capacity of the electric utilities.

Central Asian power system, 2015

Open

{kind=link}

There is a high level of complementarity of resources for the power sector among the Central Asian countries. During the summer, Tajik and Kyrgyz surpluses from hydropower could be exported to the rest of the region, while during the winter thermal power from coal and gas could be exported from Kazakhstan, Uzbekistan and Turkmenistan. Winter peak electricity demand in the gas-producing countries is not as significant as in Tajikistan because those countries have systems and appliances to use gas for heating.

Electricity generation by fuel in Central Asia, 2018

OpenThe average cost of generation in Kazakhstan, Uzbekistan and Turkmenistan is generally higher than the average cost of hydropower in Tajikistan. Prevailing retail electricity subsidies are still common, but there is a clear opportunity for Tajikistan to trade electricity especially as the region adopts more market-oriented and cost-recovery approaches. Given that the transmission infrastructure is in place, the cost of reconnection would be lower than new construction and the region could focus on grid reinforcement to improve system security.

Average cost of generation and range of retail electricity prices in Central Asian countries, 2020

OpenIn addition, if the Central Asian countries move to increase the share of variable renewables in their generation mix, then developing a more integrated market would expand the trade opportunities for Tajikistan and Kyrgyzstan to provide ancillary services. Kazakhstan, Uzbekistan and Turkmenistan have high potential for solar PV and wind energy. Maximising the potential of these renewable resources could serve as an additional driver to deepen integration of the regional electricity market.

Technical potential for installed renewable energy capacity in Central Asia

|

Country |

Small hydro (GW) |

Wind (GW) |

Solar PV (GW) |

|---|---|---|---|

|

Kazakhstan |

4.8 |

354 |

3760 |

|

Kyrgyzstan |

1.8 |

1.5 |

267 |

|

Tajikistan |

23 |

2 |

195 |

|

Turkmenistan |

1.3 |

10 |

655 |

|

Uzbekistan |

1.8 |

1.6 |

593 |

Source: UNDP (2014), Renewable Energy Snapshots.

A recent study assessed the benefits of regional power system co-operation in Central Asia (RTE and ADB, 2020). It highlighted that, based on their abundant hydropower resources, Tajikistan and Kyrgyzstan could provide important secondary regulation. In particular, Tajikistan could increase the volume of activated frequency restoration reserve (FRR) from 4 TWh in a situation without regional co-operation to 17.6 TWh with full cross-border procurement of FRR by 2030. This could provide a significant income stream for Tajikistan in addition to its existing seasonal bilateral exports. The existing and scheduled developments to the grid were assessed to be sufficient for this level of FRR trade. While there would be an increase in generation costs for Tajikistan from the large amounts of FRR mobilised, the study found that as long as those higher costs are reflected in the price of the service, participation in this trade would be a net benefit for the country.

A number of entities are in place that could support stronger market integration. Established in 1993 in Uzbekistan with investments from the five countries, the Central Dispatch Centre Energiya (CDC) (originally as the Unified Dispatch Office) is a key enabling institution to optimise the resources and power systems in Central Asia. The CDC is responsible for calculating transfers between the countries. If a power pool model were to be pursued, the CDC potentially could boost its capacity to serve as the market operator.

In terms of operations, there is the Coordination Electrical Power Council of Central Asia (CPC), which is the governing body of the CDC. The members of the CPC are the power system operators KEGOC (Kazakhstan), UzbekEnergo (Uzbekistan), Kyrgyzstan NPG (Kyrgyzstan) and Barki Tojik (Tajikistan). Turkmenistan has not been involved in CPC or CDC since it disconnected from the CAPS in 2003 to operate synchronously with Iran.

The CPC and CDC increase the institutional readiness of re-establishing a Central Asian Power System, capable of designing and operating a regional multi-directional market-based system that could support optimal resource allocation and utilisation. The stakeholders could aim for a multilateral, multi-directional trade among their differentiated markets similar to the model of the Southern African Power Pool (SAPP). The SAPP operates as a multilateral platform to trade electricity surplus close to real-time alongside other arrangements, which preserves the domestic price-setting approach of the participants as well as to remain rather independent from neighbouring countries for electricity security. For Central Asia, when confidence in the regional market is established and variable renewables increase in the generation mixes, the depth of integration can strengthen. In these conditions, Tajikistan's hydro resources would be a significant contributor.

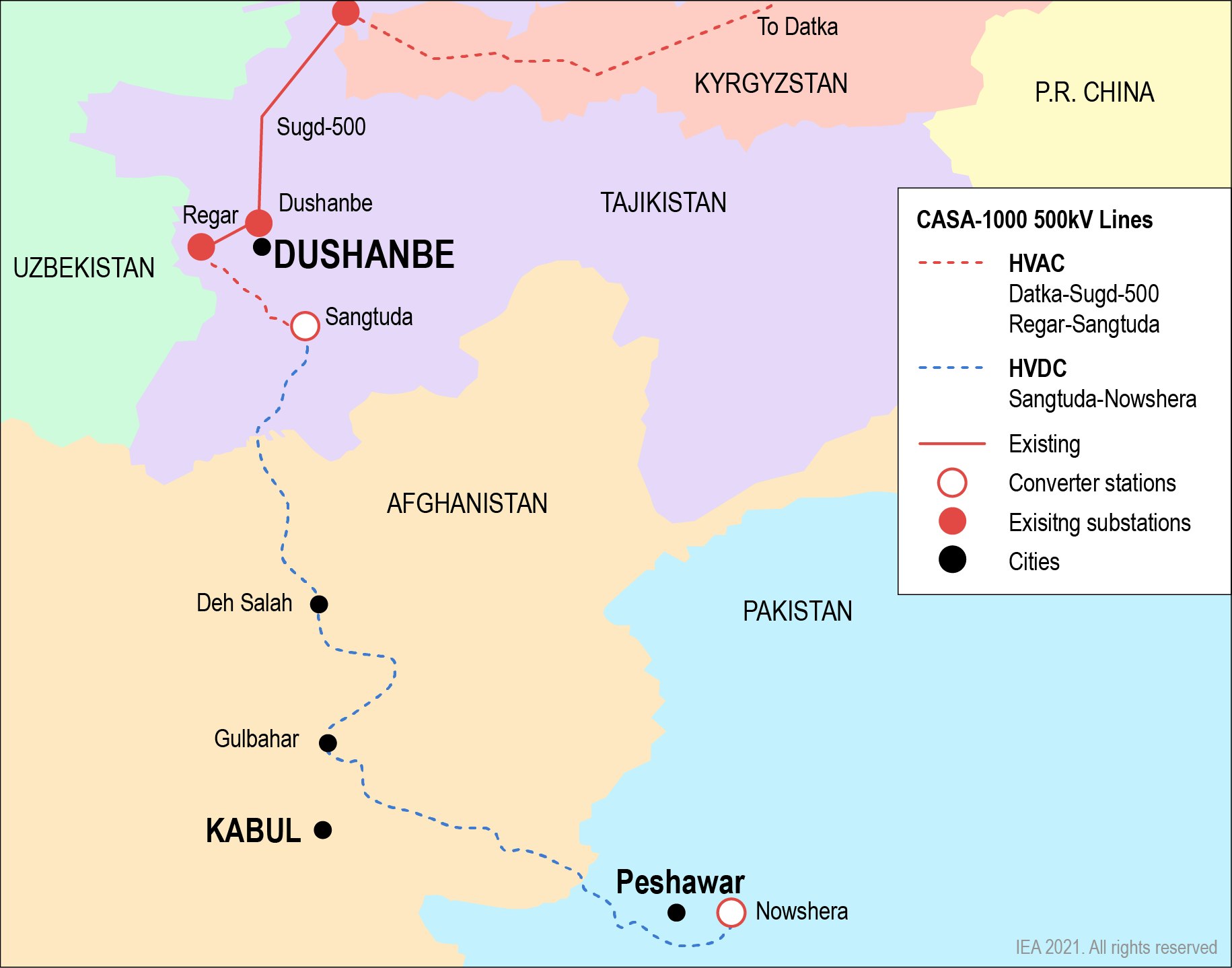

Flexible trading in the near term and increased exports in the long term with Pakistan

Tajikistan’s abundant hydro resources during the summer represent an excellent opportunity to export electricity to Pakistan, its southern neighbour, where shortages are common in the summer due to high cooling demand. In fact, there are planned electricity trade initiatives as part of the new electricity transmission system, called CASA-1000, to connect Tajikistan and Kyrgyzstan, both with abundant hydropower resources, with nearby Pakistan, which suffer from chronic electricity shortages. It includes 500 kilovolt (kV) alternating current (AC) lines in Tajikistan and Kyrgyzstan and a 1 300 MW capacity high voltage direct current (HVDC) line to Pakistan, passing through Afghanistan. Currently, there is a power purchase agreement in place, through a 15-year bilateral contract between Tajikistan and Pakistan (Government of Pakistan, 2015). The terms include:

- Term: estimated start of operation in 2023 and a term of 15 years.

- Tariff and delivery type: firm energy for May to October at USD 94/MWh, with an option to offer excess at USD 64/MWh.

- Transit costs through Afghanistan: USD 12.5/MWh.

- Minimum supply requirements: 1 299 GWh in year 1 to 1 071 GWh in year 15.

Feasibility studies show that Tajik electricity export can be increased further to 2.7 TWh in a co-ordinated operation with Kyrgyzstan (SNC Lavalin, 2011). Short-term flexible trading could pave the way for higher utilisation of the CASA-1000 transmission line. Tajikistan, Kyrgyzstan and Pakistan, the three main countries involved with electricity trading via the CASA-1000 transmission network could consider flexible trading in the near term. Trade contracts for flexibility could be in addition to the 15-year term PPAs. Short-term arrangements for flexibility services could allow Tajikistan to adjust the price and quantity offering depending on its volume of surplus. Short-term arrangements could also allow Tajikistan to export electricity in the winter if domestic demand is served and there is sufficient demand in Pakistan. Moreover, short-term arrangements could provide opportunities in the winter for Pakistan to export surplus electricity to the upstream countries in a reverse flow.

There are no current arrangements for importing. A barrier is the high cost of electricity in Pakistan at around USD 77/MWh (CPPA, 2019). However, if short-term trading is established, it could open possibilities as it would not require Tajikistan to commit resources long term while retaining the option of importing electricity in the winter when domestic thermal plants or cheaper Central Asian imports are unavailable.

Map Of CASA 1000 Transmission Plan

Open

{kind=link}

Increasing exports to Pakistan in addition to the CASA-1000 network could be possible in the long term with new transmission lines. Electricity demand in the summer in Pakistan is projected to increase by about 22 TWh and annual demand by more than 37 TWh in the period to fiscal year (FY) 2024-2025. The average electricity price in Pakistan is expected to remain high at 80 USD/MWh which offers a high margin with the cost of operation in Tajikistan.

Pakistan is planning to build new hydropower plants equivalent to about 2 GW per year in the period to 2031 to meet peak demand in summer. It is conceivable that these summer demand peaks could be met by imports of surplus power from Tajikistan.

Pakistan indicative projects in indicative capacity expansion plan and average annualised cost per MWh, 2020 - 2031

OpenIndicative hydropower projects from 2025 and beyond are expected to have high volumes and economies of scale which would lower the average cost per MWh. Hence, if exports were to increase beyond the capacity of the CASA-1000 network (1 300 MW), new transmission infrastructure would need to keep costs and risks to a minimum in order for the cost to remain competitive with domestic hydro generation in Pakistan. Shared investment among the Central Asian countries could help distribute the risks and benefits of new transmission projects.

Tajikistan is geographically situated at a central point between Central Asia and South Asia, an advantage to facilitate integration of the two markets. If common principles in grid operation, wheeling charge methodologies and dispute resolution mechanisms applied in Central Asia were to be adopted for the CASA network, then the two markets could be more easily integrated over time. A broader market would provide Tajikistan with more opportunities to expand its exports and to benefit from transit fees.

Moreover, if additional transmission capacity with Pakistan is to be built, then a co-ordinated approach among the Central Asian countries could facilitate a quicker deployment of capital and a wider distribution of risks. Tajikistan should weigh the risks and benefits of pursuing a simple bilateral-unidirectional export to Pakistan compared to a highly optimised line with multilateral participation.

Increase exports in the long term to Afghanistan

With little domestic generation capacity, Afghanistan is reliant on year-round electricity imports. Tajikistan exports electricity surplus in the summer to Afghanistan and occasionally in the winter depending on its domestic supply conditions.

Trade arrangements and transmission infrastructure: Tajikistan and Afghanistan

|

Term |

Type |

Transmission voltage and capacity |

Tariff and delivery type |

|---|---|---|---|

|

2003 (renewed 2014) |

Unidirectional from Tajikistan to Afghanistan |

110 kV with estimated 50 MW capacity |

|

|

2010 - 2030 |

Unidirectional from Tajikistan to Afghanistan |

220 kV with 300 MW capacity |

|

Source: Corporate Solutions, ADB and MEWR (2017). TA 0213 (TAJ) Power Sector Development Master Plan. Fichtner and ADB (2014). TA 8475 (AFG) Addendum to the Afghanistan Power Sector Master Plan.

The outlook is for electricity demand in Afghanistan to increase to about 16 TWh by 2032 with increasing electrification and gradual recovery of the economy (Fichtner and ADB, 2013). It is important to underline that the main driver of electricity imports is the lack of domestic generation rather than seasonal shortage as the case in Pakistan. In fact, peak demand in Afghanistan is in the winter, similar to Tajikistan. Hence, the attractiveness of exporting Tajik electricity surplus in summer depends on its price competitiveness relative to other exporters.

The cost of domestic electricity generation in Afghanistan is high. This suggests sufficient margin for electricity exports from Tajikistan even with competition from other exporters. Nonetheless, increasing Tajik electricity exports to Afghanistan would not be as straightforward relative to exports to Pakistan.

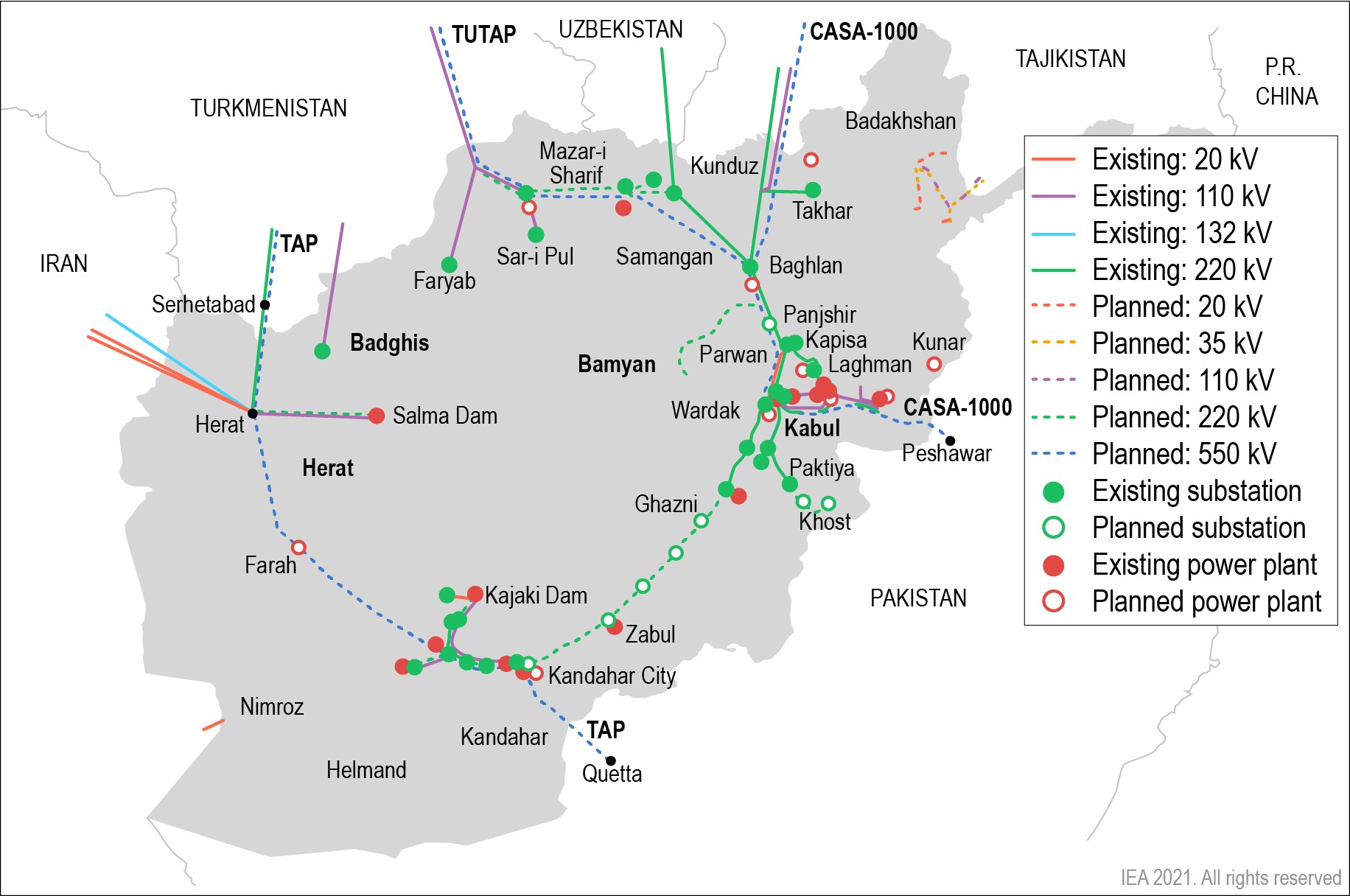

Existing and planned transmission infrastructure in Afghanistan, 2018

Open

{kind=link}

Afghanistan has no central transmission grid; several regional grids operate with no interconnection. Various donor plans look to connect the grids such as the Turkmenistan-Uzbekistan-Tajikistan-Afghanistan-Pakistan (TUTAP) project that aims to integrate grids in Central Asia with South Asia, and a 500-kV line between Baghlan and Kabul to connect the northern and southern regions of Afghanistan to facilitate larger import options (ADB, 2020).

There are issues of synchronisation which need to be tackled prior to connecting the domestic grids. Turkmenistan, Tajikistan and Uzbekistan have not operated synchronously in the past. As part of reconnection to the CAPS, Tajikistan is in the process of operating in parallel with Uzbekistan and with the rest of Central Asia by 2022 (ADB, 2018). Turkmenistan is still operating in parallel with Iran. Hence, investment in back-to-back converters or changes in cross-border operations would be needed prior to grid integration.

Afghanistan has expressed interest in joining the CAPS in the future (ADB, 2020). Tajikistan could further expand electricity trade with Afghanistan in the context of a regional electricity market with additional transmission capacity and resolution of synchronicity issues.

Electricity trade and transit in the long term with China

Tajikistan’s east borders China’s Xinjiang Uyghur Autonomous Region. The Xinjiang province is one of the most energy resource-rich regions in China, both in terms of fossil fuels and renewable resources. Xinjiang province ranks first in China in coal, oil and natural gas reserves, second for wind and solar potential, and fourth for hydroelectric potential (Duan et al., 2016).

Xinjiang province has a high level of industrial activity yet relatively low electricity consumption (290 GWh in 2019) compared with the more developed and urban eastern provinces such as Guangdong (670 GWh), Jiangsu (626 GWh) and Shandong (453 GWh) (NBSC, 2020). Hence, a significant portion of the electricity produced in Xinjiang is exported to other provinces.

Power generation, export and electricity demand in Xinjiang province, 2019

OpenData on the cost of generation in Xinjiang province are not available. So the retail price serves as a point of comparison to consider the competitiveness of Tajik hydropower. In resource-rich Xinjiang province the electricity price is lower than in other provinces in China. The benchmark price for coal-fired power in Xinjiang is about USD 38.5/MWh while in a high demand area such as Shanghai it is around USD 64/MWh and in Guangdong about USD 70/MWh. While prices for hydropower in Xinjiang province are bilaterally negotiated and are not publicly available, a survey of hydro tariffs across China range from about USD 40/MWh in Sichuan to about USD 67/MWh in Guangdong (Zhihui Photovoltaic, 2020).

The seasonal availability of the Tajik electricity surplus would be a major factor. Xinjiang experiences peak load during the summer months with winter months of November and December reaching above 90% of the annual peak load. Hence, there could be a preference for generation technology with higher availability even during the winter season. The installed hydro capacity in Xinjiang province is 2.55 GW and has an average capacity factor of 20-30% during winter, while the economically exploitable hydro resources in the province are around 16 GW (Hai et al., 2018).

In contrast to economic dispatch, the current practice in China is that all generators are dispatched for an equal amount of hours irrespective of their marginal cost. This implies that electricity imports from Tajikistan would not have a cost-competitive advantage. China’s power sector is undergoing reforms towards more market-oriented measures, though it is doing so in a stepwise manner. For example, a modification in early 2020 was to allocate 10% of coal-fired power generation to be priced in the market while 90% remains pegged to administratively set benchmark prices. This suggests that prevailing power prices in Xinjiang are likely to remain low, so Tajik summer surplus electricity exports are unlikely to be attractive on a cost basis. Other provinces in China do import electricity to a limited degree; the northeast region imports from the Russian Federation (hereafter, “Russia”) and the Democratic People’s Republic of Korea, and Yunnan province imports from Myanmar (EPPEI, 2018).

An alternative driver for an interconnection between Tajikistan and China could be as a transit country for electricity trade with higher demand regions such as Uzbekistan or to balance high levels of variable wind power installations energy in the region.

Massive construction of wind power capacity has taken place in Xinjiang in recent years. The expansion has spawned significant levels of wind power curtailment, especially between July and October (Luo et al., 2018). The number of curtailment hours is being progressively reduced. In time, both Tajikistan and China may find value in using Tajik hydro capabilities to manage the variability of electricity supply by providing balancing services.

Wind power and curtailment in Xinjiang, 2016-2019

OpenAny potential for electricity trade for balancing services or as transit for Tajikistan with China would only likely to be feasible in the long term. Transmission infrastructure investment would be required. China has plans to develop HVDC and ultra-high voltage direct current (UHVDC) transmission networks to connect its north-western regions with eastern China, as well as with Central Asia, as part of the Global Energy Interconnection Initiative (GEIDCO, 2016). It has recently constructed a 1 100 kV UHVDC line from Changji, in Xinjiang province to Guquan, in Anhui province to the east capable of delivering 66 TWh (State Grid Corporation of China, 2019). Building a transmission network to connect Central Asia and China requires plans and political agreement among the participating countries involved. Currently, there are no official announcements suggesting such co-operation.

Electricity exports in the long term to Iraq and Iran

Given Tajikistan’s proximity to the Middle East, the opportunity to export surplus electricity to address shortages is considered in this analysis. Iraq, like Afghanistan, has electricity shortages due to insufficient domestic power generation. Peak demand in Iraq occurs during summer. This suggests a possible match for the electricity surplus in the summer from Tajik hydropower.

Peak demand and generation capacity in Iraq, 2014-2030

OpenTo sell electricity to Iraq, Tajikistan would have to wheel power through Uzbekistan and Turkmenistan via a 500 kV transmission line and through Iran. Challenges are associated with each step.

- Electricity transit through Uzbekistan and Turkmenistan would be necessary before delivering to Iran and eventually Iraq. This suggests that it is more sensible for Tajikistan to establish a Central Asian regional market prior to any expanded transit ambitions.

- Turkmenistan has been exporting electricity to Iran and Turkey via Iran through a 220 kV line since 2003. Due to increasing demand, Turkmenistan is planning to build a 400 kV line to increase transmission capacity (Business Turkmenistan, 2021). Tajikistan would have to negotiate with Turkmenistan for transmission access for lines that now are heavily used by Turkmenistan.

- Finally, Iran’s peak demand takes place during summer when its transmission lines are highly used, so using its national grid for solely wheeling could be prohibitive.

Tajik direct electricity exports to Iran faces challenges. Iran has cheap and abundant fossil fuel resources for electricity generation. Tajikistan would need to have a significantly attractive price offer after taking into account the cost of transit through Uzbekistan and Turkmenistan, or through Afghanistan if a new transmission line were to be built. In Iran’s wholesale electricity market, the highest price observed during the peak summer demand is below USD 10/MWh, which is above the Tajik average generating cost for hydropower but perhaps an insufficient margin when the cost of transmission is included. The margins that would be obtained from Iran are lower than those observed in Central Asia, and there would also be the added costs of wheeling over existing or new transmission lines.

Daily average wholesale electricity prices in Iran, 2019

OpenIran aims to become a regional electricity hub and to increase exports to Afghanistan, Pakistan and Iraq (Official Gazette of Iran, 2017). In 2011, it proposed the creation of a regional electricity market to include Central Asia, Iraq, Turkey, Azerbaijan, Afghanistan and Pakistan under the Economic Cooperation Organization. In such a scheme, Iran could import electricity from Tajikistan, but likely with the purpose of increasing its own exports to Iraq, Turkey or Pakistan where it could gain a trade advantage due to its proximity and existing transmission infrastructure. Progress has developed slowly but plans to develop a roadmap are still ongoing (ECO, 2021).

Currently, sanctions on Iran limit options for electricity trade. The possibilities of a larger regional integration of electricity trading could be revisited if these conditions change.

Electricity exports in the long term to India

The CASA-1000 transmission project includes 500 kilovolt (kV) AC lines in Tajikistan and Kyrgyzstan and a 1 300 MW capacity HVDC line to Pakistan, passing through Afghanistan. This will open a pathway to a possible connection to India. This is considered in this analysis since India, like Pakistan, sees peak demand in the summer season when Tajikistan’s hydropower surplus is generally available for export.

India currently has electricity trading relationships with Nepal, Bangladesh and Bhutan. India imports electricity produced by hydropower in Bhutan. There might be appetite in India to import electricity from Tajikistan as well. India and the other South Asian countries are investigating increased electricity trading among themselves as well as with countries in the Association of Southeast Asian Nations (ASEAN) like Myanmar and Thailand.

Although unlikely in the near term, there are two avenues for Tajikistan to export electricity to India. One is to build a direct transmission line to India through Pakistan or China. Another is to wheel via grids in Afghanistan and Pakistan to India.

- The direct line option would involve building transmission lines either through disputed territories or the surrounding mountainous ranges. Either of these routes are infeasible in the short or medium term given the difficulties in getting agreements related to sensitive territories.

- The option of wheeling through Afghanistan and Pakistan would also be infeasible given that these countries encounter high demand during summer. Therefore it is reasonable to assume that Afghanistan and Pakistan would rather use their national grids to satisfy domestic demand rather than for wheeling. Moreover, currently there are no transmission interconnections between Pakistan and India. In 2014, there was a proposal for Pakistan to import 500 MW of electricity from India through the construction of a 1200 MW transmission line, but this did not materialise.

Tajikistan’s opportunities to export electricity to India could be revisited in time based on political and economic conditions. There are two reference points:

- In 2000, the United States Agency for International Development launched the South Asia Regional Initiative for Energy (SARI/EI) which involves eight countries: Afghanistan, Bangladesh, Bhutan, India, Maldives, Nepal, Pakistan and Sri Lanka. Development of electricity trade has been most successful in the east, where Bangladesh, Bhutan, India and Nepal account for the majority of cross-border electricity trade in the region. In terms of the likelihood of electricity trade between Pakistan and India, it is considered to be relatively low given the lack of transmission connections as well as political matters.

- The Turkmenistan-Afghanistan-Pakistan-India (TAPI) natural gas pipeline will facilitate the export of Turkmen gas to the other countries and is expected to be completed in 2022. This will be one of the first examples of energy infrastructure co-operation between Pakistan and India.

It is suggested to monitor updates from the SARI/EI initiative to see if progress is made in the western part of the South Asian region. Likewise, if the operation of the TAPI pipeline proves successful, then it would highlight the value of energy co-operation among the countries and could pave the way for constructing electricity transmission infrastructure.

Recommended trading options

Several options for Tajikistan’s cross-border electricity trading are explored in this report. The analysis indicates that resource availability and variations in seasonal electricity demand profiles in relation to its neighbours provide opportunities for Tajikistan to export electricity. Cross-border trade could improve the viability of its electricity sector by augmenting its income stream through exports and to reduce shortages in the winter with selected electricity imports.

Tajikistan could immediately expand electricity trading opportunities with its Central Asian neighbours in the near term based on existing transmission assets. Because the Central Asian transmission system has been connected previously, enabling institutions for cross-border integration exist. Tajikistan can export to the regional market during the summer season when electricity from hydro production is abundant, thereby lowering the region’s collective generation reserves requirement. In addition, the regional market can be an immediate source of supply for Tajikistan to cope with winter shortages when needed. Expanding beyond long-term bilateral contracts to include short-term flexible multilateral contracts would allow Tajikistan to maximise the value of its hydropower surplus for both its own and the region’s benefit, while not precluding Tajikistan from establishing additional trading relationships with other countries in the future.

Several multilateral institutions have initiatives to rebuild the Central Asian regional electricity market. If the region succeeds to establish multilateral electricity trading that is broader than long-term bilateral contracts, then it would be the first Asian region to accomplish a higher level of integration. As such, Central Asia would be a pathfinder and could provide valuable experience to other regions that are working to establish regional electricity markets.

Pakistan represents an opportunity for Tajikistan to increase its exports. The CASA-1000 transmission line is under construction and is expected to be completed by 2023. The Tajik summer export opportunity is a good match with regular supply deficits in the summer in Pakistan, plus trade volumes could increase in the future if there are attractive margins. Facilitating short-term flexible contracts would support a more optimal use of the existing transmission line and could foster integration of the CASA countries (Tajikistan, Kyrgyzstan, Afghanistan and Pakistan) with a wider Central Asian regional market. Integrating the markets could pave the way for other countries to use the CASA-1000 transmission line in the future and provide additional transit income for Tajikistan. It may also serve as catalyst for investment in additional transmission interconnections in the region.

For Afghanistan, its high annual shortfalls in meeting electricity demand will likely last until it installs sufficient domestic generation capacity. In the meanwhile, it is well placed to receive imports of Tajik surplus electricity. However, grid integration and synchronisation issues must be resolved first and Tajikistan will have to ensure that the electricity export prices remain competitive.

China is also an option for future cross-border integration with Tajikistan. However, given that Xinjiang province is rich in renewable and fossil fuel energy resources, it is unlikely to be a viable export market for Tajikistan. It could be possible for China and Tajikistan to make arrangements for ancillary services but it is unlikely to be a firm part of Tajikistan’s 2030 goal of exporting 10 TWh. China could be a long-term option for cross-border integration, though it would require government-level political agreements and significant investment in transmission networks in China and with its Central Asian neighbours.

India is an unlikely candidate for electricity trade with Tajikistan by 2030. This reflects the multiple challenges to build transmission capacity between India and Pakistan.

Iraq and Iran also are unlikely candidates for electricity trade with Tajikistan by 2030. This is due to the wheeling requirements to deliver electricity through transiting countries, which are likely to eliminate any cost advantages that Tajikistan’s hydropower may have.

References

Under unified models, resources are optimised across jurisdictional (e.g. national) borders, which means a high level of integration and a lack of local markets that are distinct from the regional market.

Central Asia here includes the five countries of Kazakhstan, Kyrgyzstan, Tajikistan, Turkmenistan and Uzbekistan.

Reference 1

Under unified models, resources are optimised across jurisdictional (e.g. national) borders, which means a high level of integration and a lack of local markets that are distinct from the regional market.

Reference 2

Central Asia here includes the five countries of Kazakhstan, Kyrgyzstan, Tajikistan, Turkmenistan and Uzbekistan.