Cite report

IEA (2021), Cross-Border Electricity Trading for Tajikistan: A Roadmap, IEA, Paris https://www.iea.org/reports/cross-border-electricity-trading-for-tajikistan-a-roadmap, Licence: CC BY 4.0

Report options

A roadmap for cross border electricity trading for Tajikistan

Cross-border electricity trading can bring a number of benefits to Tajikistan and its neighbouring countries. It has implications for economics, energy security and the integration of variable renewables.

- In economic terms, interconnecting power systems allows the parties to enhance economies of scale by expanding the customer base and maximising a broader portfolio of power system assets. In the case of Tajikistan, it provides a bigger market to which it can sell its hydropower surpluses.

- In energy security terms, interconnecting power systems offers a more diverse energy supply and reduces the impact of disruptions. Supplying electricity to meet peak demand can be more flexible by combining generation units to address varying demand patterns or outages with system resources.

- In terms of the integration of increasing shares of variable renewables, interconnecting power systems provides more flexibility sources for balancing, thereby facilitating their integration at higher levels.

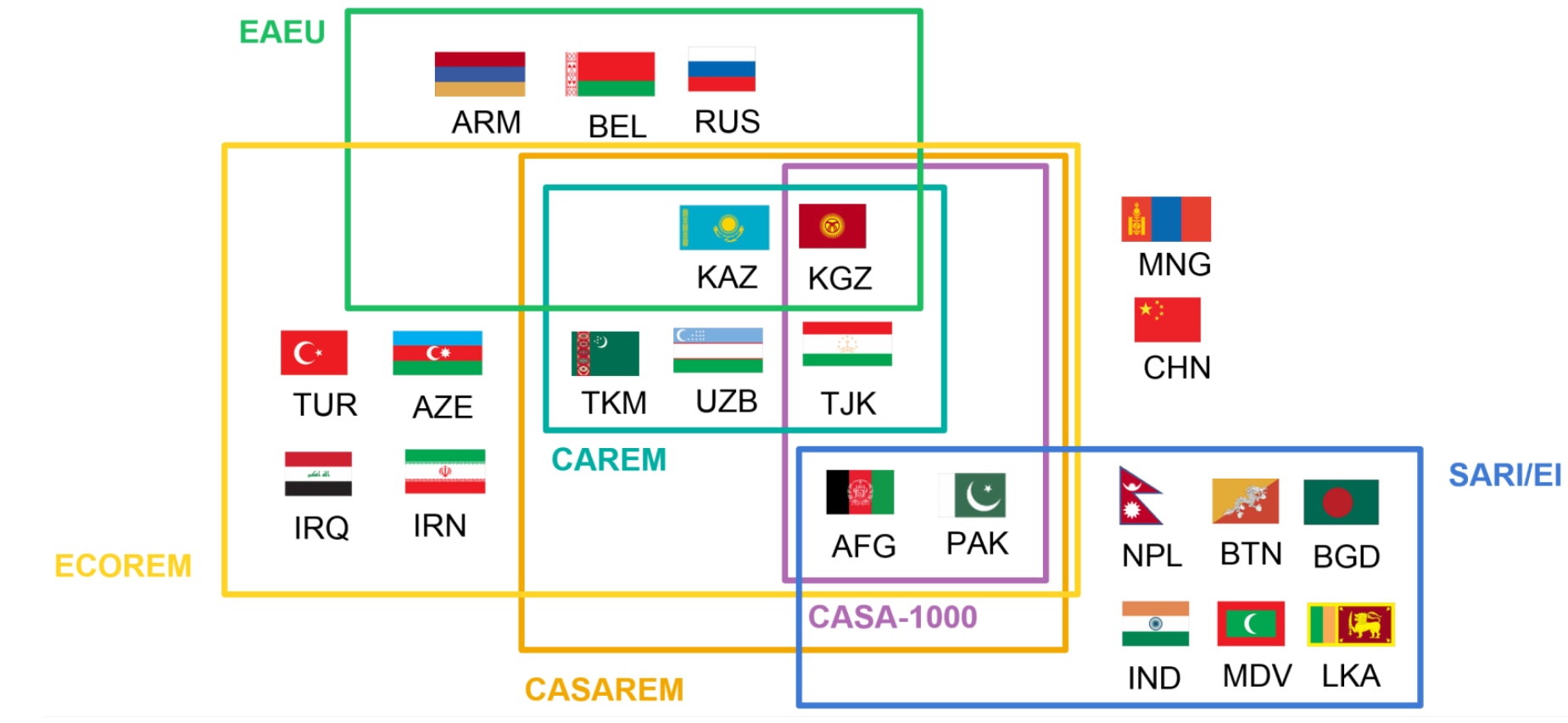

Recognising these opportunities, several initiatives aim to progress regional electricity market integration. Tajikistan has several options to directly or indirectly trade electricity with other countries as these markets develop.

Regional electricity market initiatives in the central, south, west Asian and Eurasian regions

Open

{kind=link}

It is important to note that the benefits of cross-border electricity trade are rarely distributed equally among countries. They can be hard to estimated beforehand, thereby making agreements on shared investment such as transmission system assets more difficult (IEA, 2019c).

Another issue is increased exposure to risk beyond a country’s sole control. For example, a major disruption in another country could affect an interconnected system (IEA, 2019c). Or, failure to deliver on capacity investments or to meet operational requirements in one country may compromise others on the system.

Co-ordination at the regional level for the development and operation of generation and transmission assets for the integrated system is critical. Avoiding under or over investment is a key element to avoid poor performance and ensure investor confidence.

Minimising these risks requires that the design of the electricity market, system operations and governance structures are robust and effective.

For Tajikistan, given its economy and the financial and physical condition of its power sector, regional electricity market opportunities would be attractive. Multilateral trade would allow the use of Tajik’s excess seasonal hydropower for economic gain in the near term. As the region installs more and more variable renewables in the generation mix, Tajikistan can offer valuable flexibility services to an integrated regional market.

Based on these considerations, for Tajikistan to strengthen and expand electricity trade, the IEA recommends a roadmap focused on three key points:

- Ensure favourable conditions to enable multilateral electricity trade.

- Adopt multilateral market models to expand electricity trade.

- Strengthen Tajikistan’s role as a flexibility provider for the region.

For each of these points, the following sections offer examples of international best practice and suggested policies in the Tajik context.

Ensure favourable conditions to enable multilateral electricity trade

Most electricity trading arrangements in Tajikistan today are long-term bilateral contracts with limited options for variations in volumes or price. While Tajikistan can continue this trading model, a multilateral market framework can unlock more opportunities for its hydropower resources, gain revenue and improve the efficiency of resource use for the region.

A regional multilateral electricity market requires a higher level of political agreement among the participants compared with bilateral contracts. Political will is required to implement necessary reforms associated with harmonisation and market functioning.

Tajikistan should increase its institutional readiness for more integrated electricity markets. Effective cross-border trade depends on a reliable power sector at the domestic level. Sustainability of operations, transparency and effective regulation are important to reinforce the functioning of the Tajiki power sector, which can boost confidence among trading partners in more integrated markets. To strengthen its readiness for increased electricity trading, Tajikistan should embrace these principles:

- Financial viability of utilities signals their operational sustainability as market entities – a critical characteristic to ensure confidence with trading partners that rely on electricity supply. Good management and governance contribute to operational and financial discipline, and economic viability. By working with relevant stakeholders which are affected by their operations, well-governed power system entities help to ensure beneficial and enduring business relations with trading partners.

- Transparent and timely data and information underpin effective market functioning.

- Effective regulation enforces market discipline for utilities and can contribute to their financial viability.

In addition to these principles, Tajikistan would profit in appropriately preparing power sector systems and operations for expanded trading opportunities. Capacity building in areas such as financial modelling and optimal dispatch in a regional market would be advantageous. Investment in hardware and software needed for multilateral and flexibility trading would increase Tajikistan’s readiness for opportunities in an integrated market.

Conditions to support multilateral trade: case studies

Institutional arrangements for integration of regional electricity markets

Case studies were analysed by Oseni and Pollitt (2014) to determine the important factors that promote trade in established regional electricity markets. The relevant points for Tajikistan are: to ensure a cost-effective and reliable domestic power sector, and to facilitate additional transmission capacity.

Sufficient generation capacity is essential to participation in a multilateral market. Established in 2000, the West African Power Pool (WAPP) has had almost no electricity trade for more than a decade. Inadequate installed capacity and poor infrastructure among the member countries were found to be major barriers. Interconnection studies and significant investments were made by international development institutions to help encourage trade, but concerns remained on the reliability of the domestic power sectors. In contrast, the South African Power Pool (SAPP) with ample installed generation capacity among its member countries was able to begin trading in its regional market, albeit mostly through bilateral trading.

In addition to sufficient generation capacity among the market participants, adequate transmission capacity is essential. The case studies showed that insufficiency in this regard hampered spot market transactions in the SAPP and the Central American Electrical Interconnection System (SIEPAC) which prolonged a dominance of bilateral trading. In contrast, the case studies highlighted significant transmission capacity underlying the Pennsylvania-New Jersey-Maryland Interconnection (PJM) and NordPool regional power markets. Agreements on cross-border transmission investment can be a challenge reflecting difficulties to determine cost sharing among the parties. In the cases of SIEPAC, WAPP and SAPP, cross-border transmission planning has been supported by feasibility assessments co-ordinated by international development agencies.

Ensuring a reliable domestic power sector capable of attracting sufficient investment can help Tajikistan prepare for expanded regional trade. Though cross-border transmission investment is challenging, having a capable regulatory authority co-operating with regulators in the participating countries can facilitate cost-sharing agreements.

Power sector reform: lessons learned from emerging economies

A World Bank multiyear study, Rethinking Power Sector Reform in the Developing World, tracks outcomes of power sector reforms from the 1990s in several emerging economies (Foster and Rana, 2020). It covers key issues related to governance, regulation, cost recovery, power markets and political economy. Its findings highlight that: cost recovery is difficult to achieve; the private sector has contributed to generation expansion but less so for distribution; and well-run public institutions can be made to function as efficiently as private ones.

Regulatory authorities were found to be widespread, although their level of independence in many countries is debatable. The case studies showed that the regulators perform the function of providing technical advice for the ultimate political decision makers. Some success in effective regulation of private companies was found, though less so for state-owned utilities that lack commercial incentives.

The case studies show that under recovery of cost is common and that even in countries showing progress towards cost recovery, backsliding often happens especially in emergency situations. Removing electricity subsidies is often difficult and citizens displeasure could derail the overall reform process. Targeted subsidies for the poor help to avoid universal under pricing of electricity. Several institutions such as the International Monetary Fund (IMF) and Energy Sector Management Assistance Program (ESMAP) provide case studies to appropriately strategise subsidy reform processes.

As Tajikistan undergoes further reforms in order to improve its governance and cost- recovery goals, it will be beneficial to learn from the case studies and adapt its pace and direction to ensure success.

Key policies to enable multilateral and flexible trading frameworks for Tajikistan

Principal actions

- Improve financial viability and governance in the power sector with continuing reforms and their effective implementation. Ensure appropriate co-ordination with relevant stakeholders, such as regional co-operation on water resources for hydropower.

- Increase transparency by developing open access for supply, demand and transmission, and other relevant data. The scope, frequency and resolution of additional data shared with trading partners would be determined based on the agreed market model.

- Strengthen regulatory authorities through training and capacity building. Ensure their independence and legislate reporting requirements that aid in their decision making.

Specific policies for consideration

1. Progress power sector reforms

- Progress the restructuring of Barki Tojik, the state-owned electric utility.

- Advance cost-recovery efforts through tariff reform with an appropriate strategy to handle current subsidies.

2. Increase data transparency

- Enable open access for key operational data such as demand and supply conditions, and planned or emergency works on power plants and transmission lines that could affect the functioning of an integrated market.

- Provide access to information relevant to forecasts such as water levels, planned works, generation expansion plans and financial statements.

3. Strengthen regulators

- Support training and technical capacity building for regulatory authorities in key areas such as cross-border interconnections and the functioning of various market models. This can boost the regulatory authority’s capacity to review plans for power sector investments, assess public benefits and equity of cost-sharing arrangements.

- Consider establishing institutional frameworks to ensure the independence of a national regulatory authority. This might include elements such as: creation of a body that is independent from a government ministry; assured working budget allocation; and restrictions on pre- and post- employment of staff to reduce conflict of interest risks (OECD, 2016).

- Consider providing the regulatory authority the ability to compel relevant data reporting from utilities on a regular basis.

Adopt multilateral market models to expand electricity trade

Multilateral electricity markets would provide several options for Tajikistan to increase revenue. In addition to the current practice of seasonal surplus electricity sales through bilateral arrangements, daily or weekly surpluses could also be sold in day-ahead or week-ahead markets. The balancing capabilities of reservoir hydro power plants could also be sold in balancing markets.

Establishing a specific trading model would need to take due account of the readiness of countries in terms of their power sector structure and market including third-party participation, as well as experience in cross-border electricity trading.

In the Central Asia region, only Kazakhstan has significant experience in power sector market-oriented operation with private sector participants. Hence, a secondary trading model like the Southern African Power Pool could provide the countries in Central Asia time to pursue national reforms while realising the benefits of increased trade.

In the South Asia region, only Pakistan has significant experience with third-party participation. Tajikistan and Kyrgyzstan in association with Pakistan could develop a secondary trading model which could be a feasible near-term model to optimise the CASA-1000 transmission project.

Power sector structure in the Central and South Asian countries

|

Country |

Structure |

Domestic Market |

Third-party participation |

|---|---|---|---|

|

Tajikistan |

Legally unbundled, with Barki Tojik as the holding company for all activities |

Monopoly |

Limited |

|

Kazakhstan |

Full legal and functional unbundling |

Wholesale and retail markets |

Yes. Currently about 45 privately owned enterprises |

|

Kyrgyzstan |

Legally unbundled |

Monopoly |

Limited |

|

Turkmenistan |

Vertically integrated |

Monopoly |

None |

|

Uzbekistan |

Legally unbundled |

Energo Sotish as single buyer and seller |

Limited |

|

Afghanistan |

Vertically integrated (fragmented) |

Monopoly |

Limited |

|

Pakistan |

Functionally unbundled with private sector participation |

Central Power Purchasing Authority as single buyer and seller |

Yes. Currently several independent power producers |

Source: IEA (2020), Kyrgyzstan Energy Profile; IEA (2019d), Kazakhstan Energy Profile; IEA (2019e), Uzbekistan Energy Profile; MEWR (2021b), Reform of the Electricity Sector in Tajikistan; ADB (2020), Regional Cooperation on Renewable Energy Integration to the Grid.

It is important to note that Afghanistan would not have electricity supplied via the CASA-1000 line and would only benefit from transit payments. Its existing AC transmission connections are with Central Asia. In the long term, when the grids in Afghanistan are connected and additional transmission lines connect it with Pakistan, the Central Asia and South Asia regions could be connected. Stepwise inclusion of new participants is possible when cross-border arrangements have clear procedures and rules.

Moving towards a more primary trading model such as the EU Internal Electricity Market would require the eventual harmonisation of national market structures of the participating countries. Given their varying structure and pace in restructuring, this may be considered as an option for the long term. Certain countries could choose to remain in a secondary trading arrangement while a sub-group could explore a primary trading arrangement in the future. Power pools can start with a small number of countries and grow over time as it offers more chance of steady and deep progress, as observed in the growth of PJM in the United States and Nord Pool in the European Union, rather than prolonged initial development periods (Oseni and Pollitt, 2014).

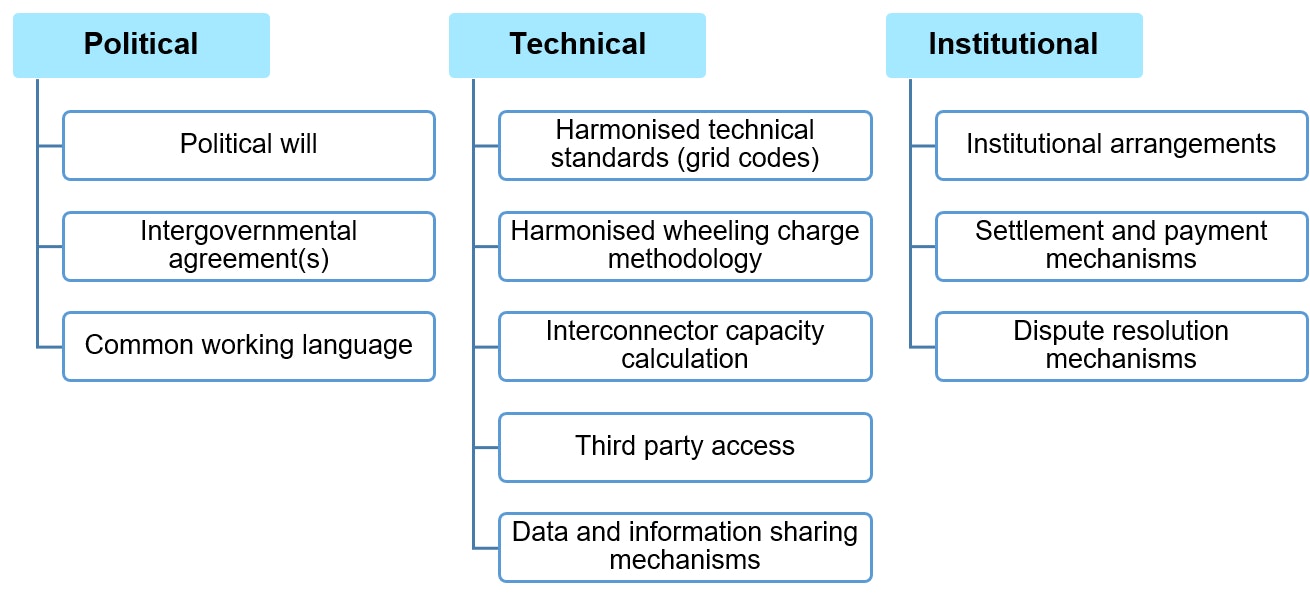

Regardless of the model chosen, there are minimum political, technical and economic requirements that the countries would need to adopt to establish effective multilateral power trading. These minimum requirements are discussed in the key policies section.

Minimum Requirements To Establish Multilateral Power Trading

Open

{kind=link}

Establishing political agreement and executing the necessary institutional changes are vital steps. The Central Asia region exhibits substantial interest to pursue expanded cross-border electricity integration and trade. A number of multilateral donors are supporting various initiatives. Tajikistan and its neighbours endorsed a roadmap to promote cross-border electricity connections as a means to pursue sustainable development.

Roadmap to promote cross-border electricity connectivity

The UN Economic and Social Commission for Asia and the Pacific (UNESCAP) member states endorsed a roadmap to promote cross-border electricity connectivity to support sustainable development. It aims to provide a framework for co-operation in the 2020-2035 period. The roadmap includes the following strategies:

- Build trust and political consensus for cross-border electricity trade.

- Develop a regional cross-border electricity grid master plan.

- Develop and implement intergovernmental agreements on energy co-operation and interconnection.

- Co-ordinate, harmonise and institutionalise policy and regulatory frameworks.

- Create competitive markets for cross-border electricity and enhance multilateral trade.

- Co-ordinate cross-border transmission planning and system operations.

- Mobilise investment in cross-border grid and generation infrastructure.

- Build capacity and share information, data, lessons learned and best practice

- Ensure the coherence of energy connectivity initiatives and the UN Sustainable Development Goals.

- Develop a regional cross-border electricity grid master plan.

Tajikistan and its neighbours across Asia are members of the UNESCAP. It can serve as a common reference point to foster cross-border electricity trading and integration to contribute to the region’s economic development through optimal use of resources. 1

Examples of multilateral electricity trading models to expand trading

This section highlights the key characteristics of primary electricity trading models, such as in the European Union, and secondary trading models such as in Southern Africa and Central America. The case studies summarise the rationale for the choice of the models and how they have developed over the years. These examples can help guide Tajikistan and its neighbours as they proceed to develop a regional electricity market.

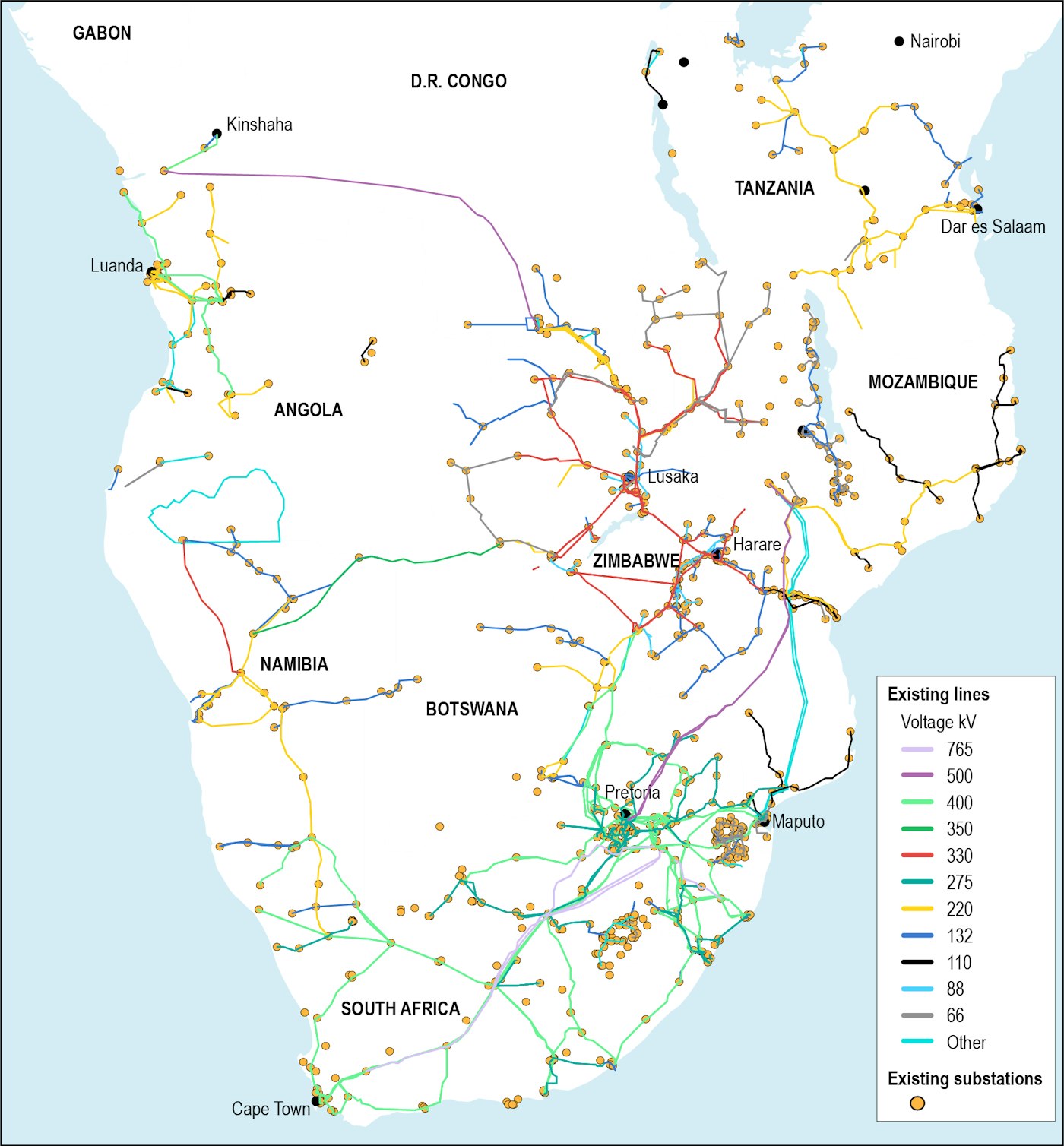

Southern African Power Pool Model

The Southern African Power Pool (SAPP) was created in August 1995 when member governments of the Southern African Development Community (SADC) signed an intergovernmental memorandum of understanding. The SAPP has twelve member countries represented by their respective electric power utilities. The SAPP co-ordinates the planning and operation of the electric power system among member utilities. Its primary aim is to provide reliable and economical electricity supply to consumers in each member country consistent with reasonable use of natural resources and minimal negative impact on the environment. For fiscal year 2018-2019, 2 TWh of electricity were traded in the competitive market, accounting for 32% of total trading while 68% were bilateral trades.

The regional power pool was established even though the electricity markets at the national level had not necessarily been restructured. National utility companies act as buyers and sellers of electricity. Independent power producers (IPPs) are allowed to trade directly. In 2001, the short-term energy market was established and in 2004, SAPP started the development of a competitive electricity market for the SADC region. A day-ahead market was instituted in 2009 and in 2015 the trading platform was upgraded with forward physical markets and an intra-day market.

An important feature of the SAPP is that only excess generation is traded; hence its classification as a secondary market arrangement. Member utilities first ensure that they can cover domestic demand before offering generation capacity to the regional market. Electricity can also be traded through the pool on an emergency basis to meet unexpected shortfalls.

The Regional Electricity Regulators Association of Southern Africa (RERA) was created in 2002 and consists of the national regulators of the member countries. RERA functions only as a co-operative body to facilitate harmonised electricity sector policy, legislation and regulation and does not wield authority in regulatory matters.

Southern African Power Pool

Open

{kind=link}

Central American Electrical Interconnection System (SIEPAC) Model

Another secondary market model is the Central American Electricidal Interconnection System (SIEPAC) which is an interconnection of the power grids of six countries (Guatemala, Honduras, El Salvador, Nicaragua, Costa Rica and Panama). The SIEPAC is a dedicated 230 kV transmission line. It is referred to as the “seventh market”, since it functions on top of the six national markets. The regional institutions are located in various member countries: the regulator, Comisión Regional de Interconexión Eléctrica (CRIE), in Guatemala; the market operator, Ente Operador Regional (EOR), in El Salvador; and the transmission owner, Empresa Proprietaria de la Red (EPR), in Costa Rica.

SIEPAC Transmission Line And Regional Market Institutions

Open

{kind=link}

The SIEPAC market is a supplemental market rather than an integration of the six national markets. It was designed in this fashion to avoid issues with free riders and undesirable price formation issue.

- The free rider issue can arise in a regional market where a member fails to contribute their fair portion to the costs of a shared resource such as adequate generation capacity. It is a type of market failure in which those that benefit do not pay or under pay for use of the resource.

- The undesirable price formation issue can arise when a member with relatively low generation costs is connected with others that have higher generation costs. Resource sharing will lead to an average equilibrium price that could be significantly higher than for the country accustomed to low prices in the absence of international trade. As the costs of generation and the level of electricity subsidies vary in the region of Tajikistan’s likely markets, avoiding a poor price outcome can make trading more appealing.

While these concerns can be addressed with effective regulation and market design, the SIEPAC approaches them by a pre-dispatch modelling of national markets before bidding into the market. Market participants that have not been dispatched in their national markets can bid into the SIEPAC market. In this way the individual countries can utilise their own least expensive resources and any excess or deficit can be covered in the SIEPAC market without increasing prices for consumers in the countries that are fully covered by domestic generation, typically the countries with low cost generation. In this model, high cost generation is replaced by surplus power from lower cost markets.

Trading in the SIEPAC market is mainly short term, but there is progress in setting up firm one-year ahead trades. Long-term investments with cash flow, coupled with available long-term transmission rights could enable larger scale investments that the national markets would not normally support due to their small sizes and projected low demand growth rates.

EU Internal Electricity Market

The European Union Electricity Market is a primary trading model. It has evolved with different levels of restructuring at member state levels since the 1990s as part of the European Council’s objective of achieving increased market integration to improve security of supply, reduce costs and improve economic competitiveness. Four EU directives (1996, 2003, 2009 and 2019) instituted major changes to achieve common market structures, expand competition and increase interconnections (European Parliament, 2020).

In order to increase the participation of the member states, a number of choices were offered to achieve specific goals. For example, the 1996 directive to increase competition in electricity generation provided that member states could set up a wholesale market where all generation utilities could freely enter or to establish competitive procurement through a single buyer. Third-party access to grids could either be through negotiations with an integrated utility or by regulation (Pollitt, 2019).

Given the difficulties associated with assigning costs in new cross-border transmission developments, the European Union established a “project of common interest” status where prospective project developers can take advantage of accelerated permitting, financial incentives and access to loans. In order to obtain this status, a prospective transmission project developer must first submit a cost-benefit analysis following an agreed methodology from the European Network of Transmission System Operators for Electricity (ENTSO-E) and the Agency for the Co-operation of Energy Regulators (ACER). In addition, a cross-border cost allocation agreement process has been established where ACER can step in and mediate disagreements about cost allocation among countries to progress a project (Meeus, 2020). These measures have been used successfully to expand cross-border transmission capacity in the European Union.

For Tajikistan and its neighbours, the process of negotiating a regional market arrangement could involve setting different pathways to reach common objectives to increase the level of participation. In addition, establishing measures to allocate costs for cross-border grid developments and to have mediation procedures could help boost investment and improve integration of a regional market.

Key policies for expanding multilateral trade

Principal actions

- Start with the basics of obtaining political agreement, understanding common goals and ambitions, and common working languages.

- Define technical standards such as harmonisation of grid codes, wheeling charge methodologies, interconnector capacity calculation methodology, third-party access, data and information sharing requirements.

- Define institutional arrangements including settlement and payment mechanism and dispute resolution measures.

- Provide enabling environments to increase trade frequency and integration by establishing regional co-operation among national regulatory authorities.

Specific policies for consideration

1. Obtain political agreement

- Obtain political agreement through appropriate avenues. For example, for the CASA-1000 countries (Tajikistan, Kyrgyzstan, Afghanistan and Pakistan), the system and market operation could be decided in CASA-1000 Intergovernmental Council. Matters relating to the Central Asian regional market could be discussed in the Coordination Electrical Power Council of Central Asia (grid operators in Kazakhstan, Uzbekistan, Kyrgyzstan and Tajikistan).

2. Determine appropriate market models and common working languages

- Determine appropriate market models for Central Asia and the CASA-1000 transmission project based on an assessment the advantages and disadvantages in relation to the participating countries.

- Develop common working languages. Central Asia uses Russian as a lingua franca while South Asia uses English. It may be useful to use both as Afghanistan and Pakistan may elect to integrate with Central Asia in the long term.

3. Harmonise grid codes for Central Asia and CASA-1000

- Develop harmonised grid codes in areas such as connection policies for customers and generators, requirements based on grid connection mode (synchronous versus converter-based) and HVDC connections.

- Establish operational policies in areas such as security, planning and scheduling, load frequency control and reserves, emergency response and restoration measures.

- Set market policies in areas such as capacity allocation and congestion management, balancing, forward capacity allocation, metering and operator training.

Given that the connection with Pakistan is through an HVDC line, the degree of harmonisation would be less compared to AC connections. Nonetheless, harmonisation would be important to ensure smooth system operation and to avoid trade distortions.

4. Establish co-operation among transmission system operators

- Establish a co-operative body of transmission system operators to co-ordinate the development of regional networks, identify projects of common interest and share information. The Central Asia Transmission Cooperation Association (CATCA) initiated by the Central Asia Regional Economic Cooperation (CAREC) programme, which includes both electricity and gas networks, could be a suitable platform.

- Consider reinforcing the role of the Coordination Electrical Power Council of Central Asia to facilitate and sustain a co-operative body of transmission system operators.

- As an independent operator operates the CASA-1000 line, it can serve as the main operator for the four countries. Co-operation of the national transmission system operators in relation to the CASA-1000 operator would need to be formalised.

5. Harmonise wheeling methodologies

- Harmonise wheeling charge methodologies such that the cost of trading is transparent to the parties involved. Key parameters would involve: amount of wheeling capacity, time duration of transmission, entry and exit points, metering of actual flows, agreed balancing procedures and mechanisms for handling losses, and cross-border taxation.

- Ensure that the complexity of the methodology is appropriate for the trades involved and that the wheeling charge is cost-reflective.

- Agree on collection management: market participants could pay directly to transmission owner in a decentralised manner. As trades increase frequency and actual power flows cross multiple borders, then a centralised institution could collect and distribute these charges. This could be achieved through the revival of the functions of CDC Energiya.

Note that as the regional market becomes more integrated, wheeling may become obsolete. In a primary trading model, transmission system operators could be compensated instead with congestion rent or income from the sale of long-term transmission rights. These rules would depend on the market model selected.

6. Harmonise interconnector capacity calculation methodologies

- Harmonise the technical methodologies to assign net transfer capacity limitations for each cross-border line. Take into consideration how to handle deviations between expected and actual power flows.

- As cross-border trading expands, the region can consider more complex calculations of interconnector capacities such as flow-based or model-based capacity determination to maximise use of the transmission systems.

7. Establish frameworks for third-party access to domestic grids

- Provide basic provisions for third-party participants in national grids such as transmission licences, connection and use agreements, and generation licences with export and import capabilities.

- Outline rights and obligations of national utilities: rights to access regional transmission networks; obligations to operate in a secure and reliable manner; to grant grid access to approved producers and consumers; and to allow power transfer through national networks.

- Outline rights and obligations of transmission system operators: rights to interconnect and transmit power; obligations to allow market participants to connect and use transmission networks; to ensure that the operation of transmission assets is in line with the grid code. (Note that if an additional transmission line were to be constructed to connect with Pakistan, an external owner and operator providing merchant transmission could be considered.)

- Outline rights and obligations of independent power producers.

- In restructured markets, rights and obligations such as connections to the grid, and to participate as long as the rules and requirements of the grid code are upheld.

- In vertically integrated monopolies, rights and obligations such as wheeling as long as the rules and requirements of the grid code are upheld.

Countries participating in an integrated electricity trading arrangement will need to agree on how to structure third-party participation. In the example of the Southern African Power Pool, IPPs have rights to sell power to a variety of pool players including national integrated utilities, and transmission system operators are obligated to provide access to wheel power to its destination.

8. Share data and information

- Develop a central institution that can collect critical system information such as operations, cross-border power flows and traded values.

- Share forecasts of demand growth, daily and seasonal peak and power system plans to guide optimal decision making for investment. Provide information on current and potential market participants. This informs the market to facilitate development of the least-cost options to ensure adequate reserves.

The level of shared data should be specified in the cross-border agreements. More integrated and high frequency trading set-ups tend to involve more data in order to improve decision making.

9. Dispute resolution mechanisms

Develop mechanisms for settlement of deviations in trade volumes, failures and for delays in trade or payment.

- Develop mechanisms to settle disputes that may arise in the development of cross-border arrangements and market frameworks.

10. Establish regional co-operation of regulators

- Establish a regional co-operation body of national regulatory authorities. Its objectives would be to facilitate the harmonisation of regulatory matters relevant for integrated electricity markets.

Strengthen Tajikistan’s role as a flexibility provider for the region

Tajikistan is surrounded by countries with high potential for wind and solar. Kazakhstan and Uzbekistan have high ambitions for their development. Integrating variable renewables can be facilitated with regional initiatives. Tajikistan can provide high value, fast-acting regulation reserves to support the integration of variable generation sources.

The higher the ambition of the Central Asian regional market to integrate variable renewables, the greater the appetite will be for hydropower for flexibility. This may lead to additional incentives to develop Tajikistan and Kyrgyzstan’s hydro reserves. With higher variable renewables, the flexibility needs of the system may involve balancing services in minutes and hours. This may add operational requirements to the existing hydro fleet for which it may not have been originally designed.

In addition, in proposing connections to regions with significant shares of wind power like in Xinjiang province, Tajikistan could position a clear offering that takes advantage of its hydro resources as a flexibility provider. If transmission lines are built, then it would have to involve Pamir Energy, the operator in the Gorno-Badakhshan Autonomous Oblast (GBAO) directly bordering Xinjiang province, as a stakeholder.

Key policies to strengthen Tajikistan’s role as a flexibility provider for the region

Principal actions

1. Enhance capacity to optimise hydro operation in different markets

- As different markets are created in Central Asia and South Asia, Tajikistan could consider developing its capacity to optimise its hydro operation for the different markets or trading arrangements that may develop, e.g. long-term bilateral arrangements, day-ahead markets and ancillary services.

2. Undertake refurbishments to adapt to increasing flexibility needs

- Given the advantages of Tajik hydropower capacity, refurbishing or upgrading its hydro plants and facilities to increase flexibility could unlock more opportunities as the rest of the region increases the share of variable renewables generation.

3. Initiate dialogue on additional transmission lines and upgrade existing lines where needed

- Initiate dialogue on exploring additional transmission lines which may serve as “seasonal reserve” (summer surplus with Pakistan), or spinning and regulating reserve (Central Asia).

- Initiate dialogue with extended partners such as China, India, and Iran to explore interest in regional market.

Vision for 2030

Tajikistan’s aim to export 10 TWh of electricity in 2030 requires a power system capable of maximising value from its hydro resources within the existing transmission infrastructure and leveraging its advantages moving forward with expanded cross-border electricity trading. To achieve its goal, Tajikistan will need to take several important steps as suggested by this roadmap. The timeline below indicates milestones. They assume that sufficient resources are available to develop the regional market. Discussions with internal stakeholders and trading partners as well as sufficiency of resources may call for timeline adjustments.

A roadmap for cross-border electricity trading for Tajikistan: A timeline for 2030

References

UNESCAP (2021). Regional Roadmap on Power System Connectivity: Promoting cross-border electricity connectivity for sustainable development.

Reference 1

UNESCAP (2021). Regional Roadmap on Power System Connectivity: Promoting cross-border electricity connectivity for sustainable development.