Cite report

IEA (2021), Hydropower Special Market Report, IEA, Paris https://www.iea.org/reports/hydropower-special-market-report, Licence: CC BY 4.0

Report options

Executive summary

Hydropower is the forgotten giant of low-carbon electricity

Hydropower is the backbone of low-carbon electricity generation, providing almost half of it worldwide today. Hydropower’s contribution is 55% higher than nuclear’s and larger than that of all other renewables combined, including wind, solar PV, bioenergy and geothermal. In 2020, hydropower supplied 17% of global electricity generation, the third‑largest source after coal and natural gas. Over the last 20 years, hydropower’s total capacity rose 70% globally, but its share of total generation stayed stable due to the growth of wind, solar PV, coal and natural gas.

Emerging and developing economies have led global hydropower growth since the 1970s, mainly through public sector investments in large plants. Today, hydropower meets the majority of electricity demand in 28 emerging and developing economies, which have a total population of 800 million. In those countries, it has provided a cost-effective way to expand electricity access. In advanced economies, however, the share of hydropower in electricity generation has been declining and plants are ageing. In North America, the average hydropower plant is nearly 50 years old; in Europe, the average is 45 years old. These ageing fleets – which have provided affordable and reliable renewable electricity on demand for decades – are in need of modernisation to ensure they can contribute to electricity security in a sustainable manner for decades to come.

Hydropower plants also make a major contribution to the flexibility and security of electricity systems. Many hydropower plants can ramp their electricity generation up and down very rapidly compared with other power plants such as nuclear, coal and natural gas – and hydropower plants can also be stopped and restarted relatively smoothly. This high degree of flexibility enables them to adjust quickly to shifts in demand and to compensate for fluctuations in supply from other electricity sources. This makes hydropower a compelling option to support the rapid deployment and secure integration into electricity systems of solar PV and wind, whose electricity production can vary depending on factors like the weather and the time of day or year. With its ability to supply large amounts of low-carbon electricity on demand, hydropower is a key asset for building secure and clean electricity systems. Today, hydropower plants account for almost 30% of the world’s capacity for flexible electricity supply, but they have the potential to provide even more.

Strong sustainability standards are vital to unlock hydropower’s huge potential

Globally, around half of hydropower’s economically viable potential is untapped. The potential is particularly high in emerging economies and developing economies, reaching almost 60%. Over the life cycle of a power plant, hydropower offers some of the lowest greenhouse gas emissions per unit of energy generated – as well as multiple environmental benefits.

Governments have an important role in ensuring hydropower’s potential is realised sustainably. Robust sustainability standards and measures are needed to increase investor confidence and gain public acceptance. Today, environmental assessments of hydropower plants can be very long, costly and risky, which can deter investment. Therefore, hydropower projects need to meet clear and widely accepted sustainability standards in order to make them viable. Ensuring that hydropower projects adhere to strict guidelines and best practices can minimise sustainability risks while maximising social, economic and environmental advantages. This approach also reduces lead times for projects.

Better visibility on revenues is key to attract investment at scale

Policy measures that provide more certainty on future revenues can reduce investment risks and ensure the economic viability of hydropower projects. Since the 1950s, more than 90% of hydropower plants have been developed under conditions providing revenue certainty through power purchase guarantees or long-term contracts. This has happened in both vertically integrated and liberalised electricity markets. Today, challenges concerning complex permitting procedures, environmental and social acceptance, and long construction periods can lead to higher investment risks. In advanced economies, the business case for hydropower plants has deteriorated due to declining electricity prices and lack of long-term revenue certainty. Long-term visibility on revenues, especially for large-scale hydropower projects with long lead times, reduces financing costs significantly and increases project viability, thereby facilitating investment. This is particularly important when the private sector is involved.

Gross hydropower capacity additions by market type, 1976-2020

OpenWithout major policy changes, global hydropower expansion is expected to slow down this decade

Global hydropower capacity is set to increase by 17%, or 230 GW, between 2021 and 2030. However, net capacity additions over this period are forecast to decrease by 23% compared with the previous decade. The contraction results from slowdowns in the development of projects in the People’s Republic of China (“China”), Latin America and Europe. However, increasing growth in Asia Pacific, Africa and the Middle East partly offsets these declines.

The IEA is providing the world’s first detailed forecasts to 2030 for three types of hydropower: reservoir, run-of-river and pumped storage plants. Reservoir hydropower plants, including dams that enable the storage of water for many months, account for half of net hydropower additions through 2030 in our forecast. Cost-effective electricity access, cross-border export opportunities and multipurpose use of dams are the main drivers of the expansion of reservoir projects. Pumped storage hydropower plants store electricity by pumping water up from a lower reservoir to an upper reservoir and then releasing it through turbines when power is needed. They represent 30% of net hydropower additions through 2030 in our forecast. The increasing need in many markets for system flexibility and storage to facilitate the integration of larger shares of variable renewables drives record growth of pumped storage projects between 2021 and 2030. Run-of-river hydropower – which generates electricity through natural water flow with limited storage capability – remains the smallest growth segment because it includes many small-scale projects below 10 MW.

Net hydropower capacity additions by technology segment, 2021-2030

OpenChina is set to remain the single largest hydropower market through 2030, accounting for 40% of global capacity growth in our forecast. However, China’s share of global hydropower additions has been declining since its peak of almost 60% between 2001 and 2010. China’s pace of hydropower development has slowed due to growing concerns over environmental impacts and the decreasing availability of economically attractive sites for large projects. In India, the world’s second‑largest growth market, new long-term targets and financial incentives are expected to unlock a large pipeline of previously stalled projects.

Growing electricity demand and export opportunities are driving faster hydropower expansion in Southeast Asia and Africa. The Lao People’s Democratic Republic (“Lao PDR”) and Nepal are developing projects for exporting electricity. Sub-Saharan Africa is expected to record the third‑largest growth in hydropower capacity over the next decade, owing to large untapped potential and the need to increase electricity access at a low cost. Hydropower development in Brazil, which has historically driven the expansion of capacity in Latin America, has slowed because of the limited availability of economically viable sites, the need for diversification, and environmental concerns. Going forward, Colombia and Argentina are set to lead hydropower growth in Latin America. Turkey’s hydropower development, which already has strong momentum, is expected to drive the largest expansion in capacity in Europe over the coming years. And in North America, electricity export opportunities are set to spur moves to realise some of Canada’s untapped hydropower potential.

Chinese investment accounts for most hydropower growth in emerging and developing economies

Over half of all new hydropower projects in sub-Saharan Africa, Southeast Asia and Latin America through 2030 are set to be either built, financed, partially financed or owned by Chinese firms. China’s role in hydropower development is largest in sub-Saharan Africa, where it is expected to be involved in nearly 70% of new capacity between now and 2030. This includes the largest hydropower project currently under construction on the continent, the Grand Ethiopian Renaissance Dam. In Asia, excluding India, nearly 45% of all hydropower plant capacity that is set to be built through 2030 involves a Chinese company. Pakistan and Lao PDR are expected to see the largest Chinese contributions in the form of financing or construction. In Latin America, over 40% of hydropower expansion is forecast to have Chinese involvement, including notable investments in Argentina, Colombia and Peru.

China’s role in owning, constructing, developing and financing hydropower project capacity, 2021-2030

OpenMore broadly, over 75% of new hydropower capacity worldwide through 2030 is expected to come in the form of large-scale projects in Asia and Africa commissioned by state-owned enterprises. In vertically integrated and single-buyer markets – in China and Africa, for example – the role of the public sector remains dominant. In Latin America and Europe, some countries provide support policies like auctions and feed-in tariffs (FiTs) that lead to higher shares of private sector investment in hydropower plants.

Sector share of hydropower capacity additions and average plant size, 2000-2030

OpenThe modernisation of ageing hydropower plants is necessary to maintain reliable and flexible power supplies

Between now and 2030, USD 127 billion – or almost one-quarter of global hydropower investment – will be spent on modernising ageing plants, mostly in advanced economies. Work on existing infrastructure – such as the replacement, upgrade or addition of turbines – will account for almost 45% of all hydropower capacity installed globally over the period. In North America and Europe, modernisation work on exisiting plants is forecast to account for almost 90% of total hydropower investment this decade. Overall, this spending on modernising plants helps global hydropower investment to remain stable compared with last decade.

However, projected spending on existing plants is not enough to meet the global hydropower fleet’s modernisation needs. By 2030, more than 20% of the global fleet’s generating units are expected to be more than 55 years old, the age at which major electromechanical equipment will need to be replaced. This offers an excellent opportunity to increase the flexbility capabilities of ageing plants. The modernisation of all ageing plants worldwide would require USD 300 billion of investment between now and 2030 – more than double the amount we currently expect to be spent on this. The limited visibility on long-term revenues and the major investments needed to replace equipment can make it difficult to secure the necessary financing. The contractual arrangments and ownership model of each hydropower plant will be key factors in determining whether and when modernising the plant is bankable.

Hydropower’s flexibility is critical for integrating rising levels of wind and solar PV in electricity systems

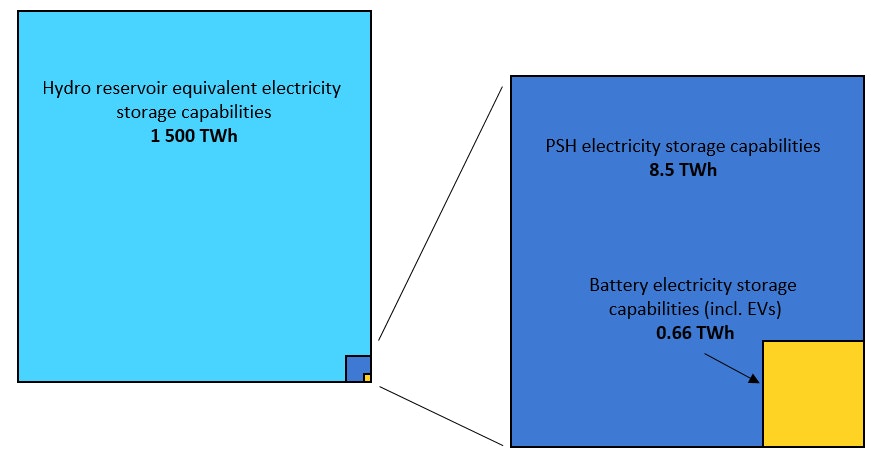

The flexibility and storage capabilities of reservoir plants and pumped storage hydropower facilities are unmatched by any other technology. Higher shares of variable renewables will transform electricity systems and raise flexibility needs. With low operational costs and large storage capacities, existing reservoir hydropower plants are the most affordable source of flexibility today. For the first time, the IEA has estimated the enormous energy value of water stored behind hydropower dams worldwide. The reservoirs of all existing conventional hydropower plants combined can store a total of 1 500 terawatt-hours (TWh) of electrical energy in one full cycle – the equivalent of almost half of the European Union’s current annual electricity demand. This is about 170 times more energy than the global fleet of pumped storage hydropower plants can hold today – and almost 2 200 times more than all battery capacity, including electric vehicles.

Global energy and electricity storage capabilities by technology, 2020

Open

{kind=link}

Pumped storage hydropower plants will remain a key source of electricity storage capacity alongside batteries. Global pumped storage capacity from new projects is expected to increase by 7% to 9 TWh by 2030. With this growth, pumped storage capacity will remain significantly higher than the storage capacity of batteries, despite battery storage (including electric vehicles) expanding more than tenfold by 2030. In addition to new pumped storage projects, an additional 3.3 TWh of storage capability is set to come from adding pumping capabilities to existing plants.

Developing a business case for pumped storage plants remains very challenging. Pumped storage and battery technologies are increasingly complementary in future power systems. Each offers cost-effective storage solutions for different timescales. However, as pumped storage plants are larger and more capital-intensive, investment in them is viewed as riskier than battery projects and is not always adequately remunerated. The economic attractiveness of new pumped storage investments is weakened by a lack of long-term remuneration schemes, low prices for flexbility services, and uncertainty over electricity prices and market conditions.

Despite strong drivers, several barriers are hampering faster deployment of hydropower

New hydropower plants can provide a critical source of cost-effective and flexible low-carbon electricity. Prior to the massive cost declines of solar PV and wind, hydropower was the most competitive renewable electricity source globally for decades. Compared with other renewable options and fossil fuels, developing new large-scale hydropower plants remains attractive in many developing and emerging economies in Asia, Africa and Latin America where there is still significant untapped hydropower potential to supply flexible electricity and meet increasing demand. New pumped hydropower projects offer the lowest-cost electricity storage option. Greater electricity storage is a key element for ensuring electricity security and a reliable and cost-effective integration of growing levels of solar PV and wind.

However, the hydropower sector has a number of challenges that hamper faster deployment. New hydropower projects often face long lead times, lengthy permitting processes, high costs and risks from environmental assessments, and opposition from local communities. These pressures result in higher investment risks and financing costs compared with other power generation and storage technologies, thereby discouraging investors. In emerging and developing economies, where the largest untapped potential for new hydropower lies, the attractiveness of hydropower investments is impacted by economic risks, concerns about the financial health of utilities and policy uncertainties. In advanced economies, current market designs often do not support the business case for pumped storage plants, and there is a lack of incentives to modernise ageing fleets.

Policy support remains limited, with less than 30 countries targeting hydropower. The public sector owns and operates 70% of all hydropower capacity installed globally between 2000 and 2020. Historically, its extensive involvement in developing hydropower plants has ensured adequate remuneration and profitability in the context of long-term energy planning. Today, when the private sector is involved, well-designed government policies are crucial for reducing risks related to permitting, construction and environmental and social acceptance challenges. Beyond electricity supply, hydropower infrastructure enables multiple benefits for managing water resources needed for critical public services such as such as irrigation, flood prevention and water supplies. Acknowledging these advantages and attributing monetary value to them can significantly enhance the business case for hydropower.

Stronger policy attention and greater ambition for hydropower is needed to meet net-zero emissions goals

If governments address the hurdles to faster deployment appropriately, global hydropower capacity additions could be 40% higher through 2030, according to the accelerated case we developed for this report. In emerging and developing economies, faster growth would be possible with increased access to concessional financing and the introduction of innovative business models such as public-private partnerships that allocate risk to the appropriate stakeholder. In addition, faster growth could be possible if project delays due to environmental and social concerns are kept at a minimum through streamlining approval processes, notably in Asia and Latin America. In advanced economies, modifying market designs or introducing policies that provide revenue certainty could boost growth for pumped storage projects. All of these efforts to accelerate deployment would still need to be carried out in a manner that maintains high sustainability standards.

Net hydropower capacity additions over 2021-2030, by scenario

OpenReaching net-zero emissions by 2050 worldwide calls for a huge increase in hydropower ambitions. Our accelerated case provides an outlook for faster hydropower expansion based mostly on implementation improvements. But to put the world on a pathway to net zero by 2050, as set out in the IEA’s recent Global Roadmap, governments would need to raise their hydropower ambitions drastically. In fact, the expansion of global hydropower capacity through 2030 would need to be 45% higher than in our accelerated case. A

The IEA’s 7 priority areas for governments to accelerate hydropower growth

- Move hydropower up the energy and climate policy agenda

- Enforce robust sustainability standards for all hydropower development with streamlined rules and regulations

- Recognise the critical role of hydropower for electricity security and reflect its value through remuneration mechanisms

- Maximise the flexibility capabilities of existing hydropower plants through measures to incentivise their modernisation

- Support the expansion of pumped storage hydropower

- Mobilise affordable financing for sustainable hydropower development in developing economies

- Take steps to ensure to price in the value of the multiple public benefits provided by hydropower plants