Cite report

IEA (2021), Achieving Net Zero Electricity Sectors in G7 Members, IEA, Paris https://www.iea.org/reports/achieving-net-zero-electricity-sectors-in-g7-members, Licence: CC BY 4.0

Report options

Executive summary

The G7 has an opportunity to lead the global energy markets towards net zero emissions by 2050. In June 2021, the G7 Leaders committed to “net zero no later than 2050” and to “lead a technology-driven transition to net zero, supported by relevant policies”. These commitments demonstrate political leadership and come at a critical time, ahead of the 26th Conference of the Parties of the United Nations Framework Convention on Climate Change. G7 members – Canada, France, Germany, Italy, Japan, the United Kingdom, the United States plus the European Union – in 2020 accounted for nearly 40% of the global economy, 30% of global energy demand and 25% of global energy-related CO2 emissions. Implementing the policies, proving the technologies and taking the steps necessary to achieve net zero emissions in a secure and affordable way in the G7 are critical to accelerating people-centred transitions around the world.

Decarbonising electricity is central to reaching net zero emissions, as it addresses the highest emitting sector today and enables the decarbonisation of other sectors. This roadmap for G7 electricity sectors identifies key milestones, emerging challenges, opportunities for innovation and principles of action to achieve net zero by 2035. It builds on the IEA report Net Zero by 2050: A Roadmap for the Global Energy Sector and is aligned with the June 2021 G7 commitment to “an overwhelmingly decarbonised power system in the 2030s”. The G7 roadmap follows the IEA Net Zero Emissions by 2050 Scenario (NZE) global pathway that is consistent with limiting the global average temperature rise to 1.5 °C, although it is not the only pathway to this objective. It was developed within the comprehensive energy modelling frameworks of the World Energy Outlook and Energy Technology Perspectives report, incorporating the latest energy data and the state of technology, and expands on policy settings around the world.

Clean energy transitions in the G7 are underway

The electricity sector accounts for one-third of G7 energy-related emissions today, well below the peak share of nearly 40% in 2007, as electricity sector emissions are on a decline with coal giving way to cleaner sources. The main drivers of these reductions in recent years were cheap natural gas in several markets and strong growth for renewables. In 2020, natural gas and renewables were the primary sources of electricity in the G7, each providing about 30% of the total, followed by nuclear power and coal at close to 20% each.

Momentum is building as governments in the G7 are re-shaping the electricity policy landscape with net zero in their sights. All G7 members have made a commitment to reach net zero emissions, underpinned in each case by a range of policy measures and targets that aim to phase out or reduce unabated coal-fired power while increasing the use of renewables, hydrogen, ammonia and carbon capture technologies, among other things. Over USD 500 billion in government funds have been collectively committed by G7 members to clean energy to boost sustainable recoveries from the Covid-19 pandemic, almost 20% of which is for the electricity sector. G7 members have also pioneered carbon pricing mechanisms and continue to apply these to support the decarbonisation of electricity.

G7 action must accelerate to reach key milestones on the path to net zero electricity by 2035

Scaling up low-carbon technologies is the central pillar to achieve net zero, with wind and solar PV capacity additions scaling up from about 75 GW in 2020 to 230 GW by 2030. On the path to net zero electricity, renewables reach 60% of electricity supply by 2030 in the G7, compared with 48% under current policies. This requires effective government action to remove barriers and design and implement predictable and consistent policies, markets and regulatory frameworks. Nuclear power, low-carbon hydrogen and ammonia, and plants equipped with carbon capture add further to the low-emissions electricity supply.

The expansion of low-carbon electricity goes hand-in-hand with phasing out unabated coal. This means no approvals for new unabated coal plants from 2021, retrofitting existing plants to co-fire biomass or low-carbon ammonia or add carbon capture equipment, and retiring any plants that are not retrofitted in this way. It is also critical to drive down the share of unabated natural gas-fired generation in the G7 to just a few percentage points by 2035 compared with nearly 25% under current policies.

Rapid electrification of end-uses is also needed to achieve net zero emissions by 2050, with energy efficiency moderating electricity demand growth. In the G7, electricity demand rises by one-quarter in 2030 and over 80% in 2050 compared with the 2020 demand level, pushing the share of electricity in final energy demand from 22% in 2020 to 30% in 2030 and 56% in 2050. Electrification of the passenger car fleet and hydrogen production have the biggest impact, and heat pumps come to dominate the provision of heating in buildings. Growing economic activity adds to demand to 2050, but is more than offset by efficiency savings, with the efficiency of key products sold doubling between today and 2030 in the NZE, in line with targets from the Super-Efficient Equipment and Appliance Deployment initiative.

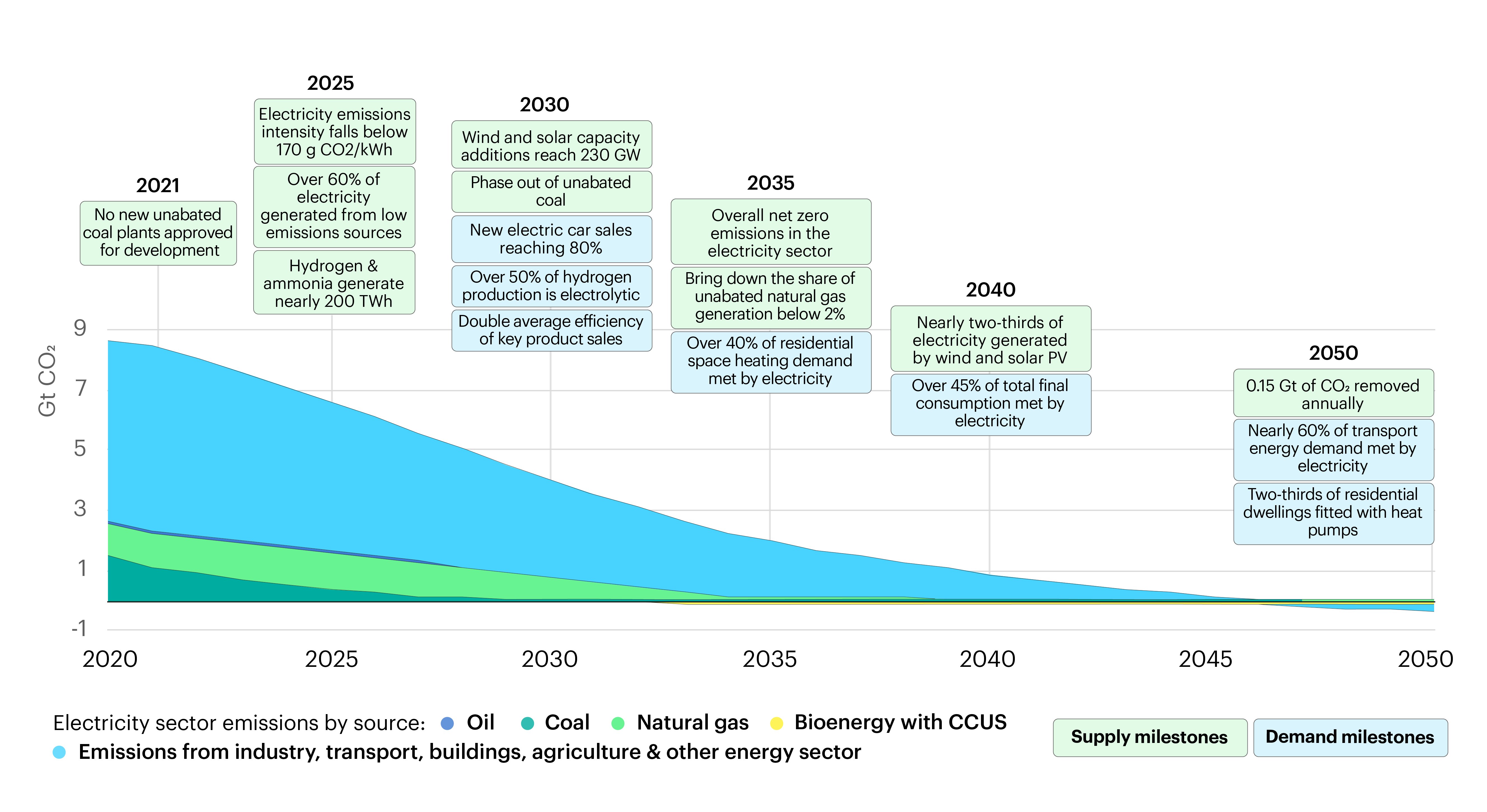

G7 energy-related emissions and electricity sector milestones in the Net Zero Emissions by 2050 Scenario, 2020-2050

Open

{kind=link}

Net zero emissions from electricity in the G7 is part of the broader pathway set out in the IEA Net Zero by 2050: a Roadmap for the Global Energy Sector that establishes over 400 sector-specific and technology-specific milestones. The global electricity sector transitions from the highest emitting sector today to achieve net zero by 2040, enabling other sectors to cut emissions via electrification. Global milestones for 2030 include renewables capacity more than tripling to over 10 000 GW, electric vehicles passing 60% of new car sales, low-carbon hydrogen production scaling up to 150 million tonnes, and all new buildings are zero-carbon ready. In industry, all electric motors are best in class by 2035 and 90% of heavy industry production uses low-emissions technologies by 2050.

People-centred transitions can create new opportunities

Investments in electricity generation within the G7 triple in the coming decade in the NZE, and then stabilise at about twice the current level in the 2030s and 2040s. Over 60% of this investment goes into wind and solar PV in 2030. Investments in networks double by 2030 and decline thereafter. Investments on this scale are far beyond those projected under current policies and need to be underpinned by measures to ensure timely project approvals and coordinate electricity system investments across the value chain.

The decarbonisation of electricity in the NZE creates many employment opportunities, including 2.6 million jobs in the G7 within the electricity sector in the next decade, although 0.3 million jobs are lost at fossil fuel power plants by 2030 plus reduced upstream jobs in fuel supply. In the NZE, job creation across the entire energy industry greatly outweighs job losses in fossil fuel sectors, however, the local impacts can be pronounced. G7 members will need to carefully deploy transition mechanisms and funding to ensure that affected workers and communities are not left behind. The IEA Global Commission for People-Centred Clean Energy Transitions is delivering recommendations to COP26 regarding how to design these transitions to ensure equity and inclusion, and to ensure climate progress can endure political cycles.

The affordability of energy is crucial to ensuring a just and people-centred transition; in the long term in the NZE, households spend a lower share of their disposable income on energy in the G7. While total energy spending across the G7 increases by 0.3% annually between now and 2050, its share of GDP declines from around 7% today to just over 4% in 2050. Household spending on electricity increases, but this is more than offset by a decline in household spending on coal, natural gas and oil products, and total household energy spending in the G7 declines by one-third by 2050. Taking account of additional investments in efficiency, total energy spending per household in G7 countries is about USD 200 less in 2050 in the NZE on average than today. Governments must ensure that all households are able to access these gains, including through tariff designs, by facilitating energy efficiency and, where applicable, supporting the transition to clean options that are more expensive.

Electricity security takes centre stage

New challenges emerge as the share of electricity in total energy demand rises along with the share of wind and solar PV, leading to a tripling of hour-to-hour flexibility requirements in the G7 from 2020 to 2050. The share of wind and solar in electricity generation rises in the G7 from 14% in 2020 to over 40% in 2030 and to two-thirds in 2050. Moving well beyond experience to date, the G7 has an opportunity to demonstrate that electricity systems with 100% renewables — during specific periods of the year and in certain locations — can be secure and affordable. At the same time, the primary sources of flexibility shift from unabated coal and natural gas to demand response and battery storage in the long term, with hydropower as an important source throughout. Robust electricity grids are essential to support transitions and take advantage of all sources of flexibility. The G7 can lead the way in developing technological solutions that address emerging challenges, including the need for seasonal storage, alongside appropriate market structures and system operation practices.

The challenges to electricity and wider energy security in the NZE require a whole systems approach. This extends beyond narrow operational issues to encompass systems resilience in the face of threats such as climate change, natural disasters, power failures and cyberattacks. To accomplish this, G7 members will need to work collectively to share best practices and put cyber and climate resilience at the heart of their energy security policies. The NZE sees a notable reduction in dependency on net energy imports over time for importing countries in the G7, which is a positive from an energy security perspective, but new concerns arise, notably with respect to supply chains for the critical minerals needed for clean energy technologies.

Innovation is essential to reach net zero electricity

Innovation delivers about 30% of G7 electricity sector emissions reductions in the NZE to 2050 by bringing additional technologies to market. Mature technologies like hydropower and light-water nuclear reactors contribute only about 15% of reductions, while about 55% of reductions come from the deployment of technologies currently in either the steady scale-up or early adoption phases. Onshore wind and crystalline silicon PV cells are being scaled up currently while coal with carbon capture, large-scale heat pumps, demand response and battery storage are examples from the early adoption phase. The remaining 30% of G7 electricity sector emissions reductions are delivered by technologies still in the demonstration or prototype phase today. These include floating offshore wind, carbon capture technologies for natural gas or biomass, and hydrogen and ammonia. Without strong international cooperation that includes the G7, the transition to net zero emissions could be delayed by decades. Initial deployment of key technologies could be delayed by 5-10 years in advanced economies and by 10-15 years in emerging market and developing economies.

Innovation can be accelerated through international cooperation, building on existing initiatives, especially in the form of knowledge sharing and coordination of development and demonstration efforts. Such cooperation could bring technologies to market more quickly, for example coordinating multiple demonstration projects in parallel, unlocking emissions reductions and opening new markets. As it has done for nuclear power, solar PV, onshore wind and fixed-bottom offshore wind, the G7 could lead development of floating offshore wind, and also hydrogen and ammonia use in power plants.

Digitalisation would also gain from international cooperation regarding best practices, unlocking benefits such as enhanced demand-side flexibility and approaches to cyber security. Policymakers can help level the playing field for all sources of flexibility, facilitate consumer engagement, develop standards and protocols for data exchanges, and coordinate planning to ensure that investments made in grids and other infrastructure help to unlock the benefits of digitalisation.

The G7 is a key enabler for global net zero emissions

As advanced economies, the G7 must respond to global calls for major economies to go faster, as being a first mover will create spill-over benefits that support other countries' energy transitions. G7 Leaders have shown political leadership through their commitment to reach net zero emissions no later than 2050. Clear roadmaps to cut emissions in sectors like electricity, industry and transport will be critical to drive innovation and cost reductions for key technologies. Implementation of these roadmaps will also expand policy and technology experience, providing benefits to G7 members through new technology opportunities, new jobs created and in making energy more sustainable and affordable. Other countries also benefit from reduced technology costs, reduced uncertainties and expanded operational experience, notably integrating high shares of variable renewables while addressing cyber and climate resilience risks. The IEA is ready to support the G7 to successfully set an example that would set the stage for other countries to scale up their ambitions to reach net zero.