Cite report

IEA (2022), Southeast Asia Energy Outlook 2022, IEA, Paris https://www.iea.org/reports/southeast-asia-energy-outlook-2022, Licence: CC BY 4.0

Report options

Key findings

Southeast Asia has developed rapidly over the past two decades and the region is a major engine of global economic growth, but there are strong country-by-country variations

Southeast Asia’s policy choices will have huge implications for its future energy mix

With today’s policies, energy demand, fossil fuel imports and emissions are set to increase; the region would also fall short on its target to provide access to clean cooking for all by 2030

Governments can introduce policies and measures to boost energy security and affordability, reduce emissions and ensure energy access for all

Energy demand in Southeast Asia has increased on average by around 3% a year over the past two decades, and this trend continues to 2030 under today’s policy settings in the STEPS. Southeast Asian countries are in different stages of their development, but almost all of their economies have more than doubled in size since 2000. The Covid‑19 pandemic disrupted these trends but economic growth is set to return: the region’s economy expands in all our scenarios by 5% a year on average until 2030 before slowing to an average of 3% between 2030 and 2050.

Three-quarters of the increase in energy demand to 2030 in the STEPS is met by fossil fuels, leading to a near 35% increase in CO2 emissions. Energy access has been improving in Southeast Asia in recent years: around 95% of households today have electricity and 70% have clean cooking solutions such as liquefied petroleum gas and improved cook stoves. However, these shares remain very low in Cambodia and Myanmar, and the recent surge in commodity prices threatens to set back progress. In the STEPS, universal access to electricity is achieved around 2030, but even by 2050, more than 100 million people in the region do not have access to clean cooking. The region also sees a steady worsening in its energy trade balance as fossil fuel demand outpaces local production.

Governments across Southeast Asia have set out long-term plans for a more secure and sustainable future. For example, six Southeast Asian countries have already announced net zero emissions and carbon neutrality targets. The SDS maps out a way to achieve these goals in full, and also sees enhanced efforts to achieve universal access to energy in 2030. Fossil fuel subsidies are phased out, efficiency improvements temper the growth in overall demand, and there are concerted efforts to boost clean energy technology deployment in power generation and end-use sectors. For example, in the SDS, 21 GW of renewable capacity are added on average each year to 2030 (triple the level of recent years) and nearly 25% of the cars sold in the region by 2030 are electric. These efforts also help reduce the region’s fossil fuel import bill. Delivering electricity and clean cooking access to all by 2030 is achieved with an investment of USD 2.8 billion a year (about 2% of average annual energy sector investment in the region to 2030).

Each country has its own pathway, and the range and diversity of countries and situations in Southeast Asia mean that delivering on these interrelated goals will be a challenge. Intraregional co-operation and international support will be critical, especially to boost innovation and support the development of related infrastructure.

The region’s fuel import needs and energy security vulnerabilities will rise sharply in the decades to come without a strong effort to accelerate transitions

Russia’s invasion of Ukraine highlights the importance of mechanisms to safeguard the region’s security of supply, alongside policies to reduce energy security risks over time

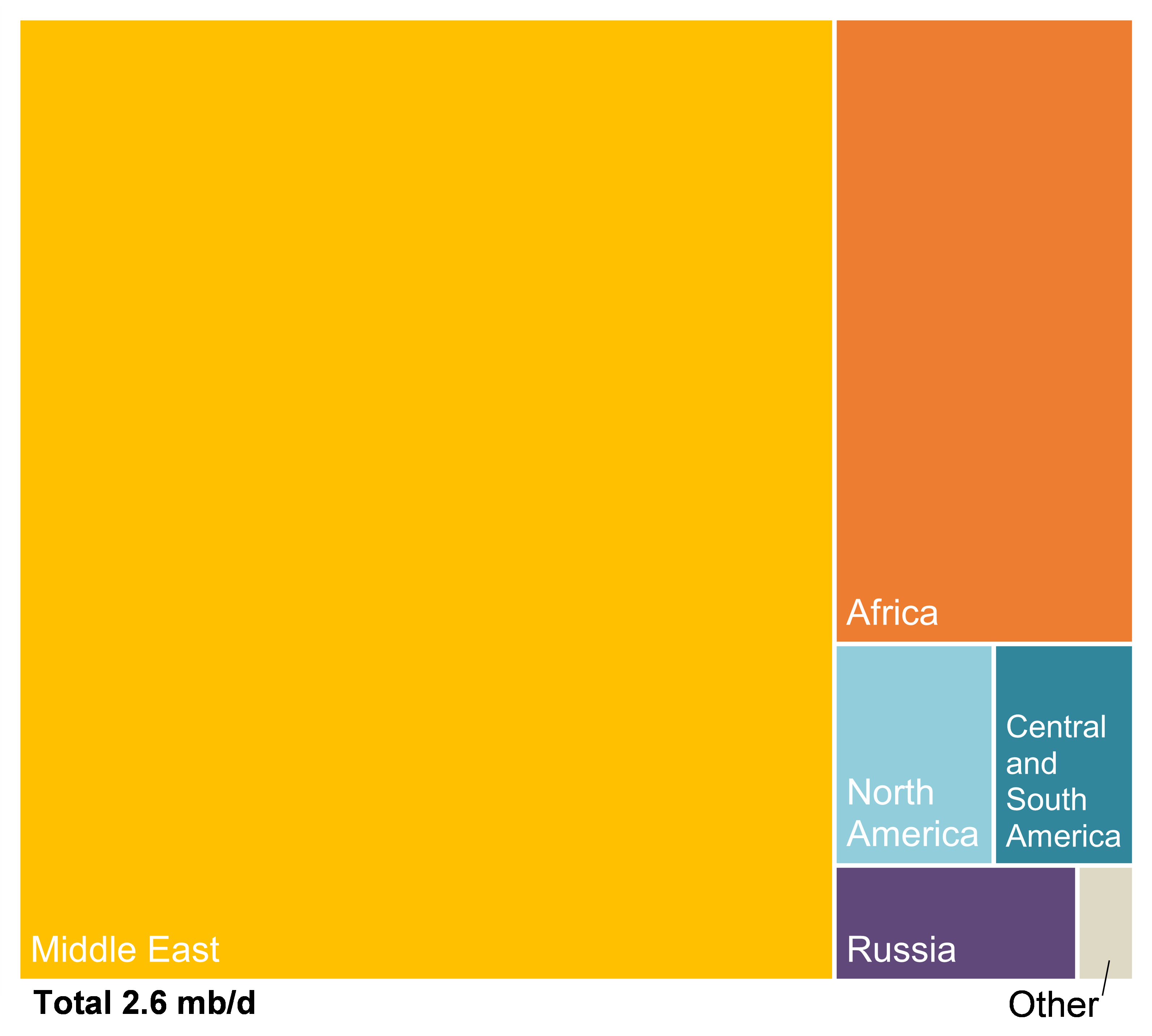

Seaborne crude oil trade to Southeast Asia from around the world, 2020

Open

{kind=link}

Oil stockpiles required by companies and refineries operating in Southeast Asia

|

Country |

Mandatory operational oil stockpiles (as of March 2019) |

|---|---|

|

Brunei |

31 days for refineries |

|

Cambodia |

30 days for companies importing oil |

|

Indonesia |

14 days (crude oil) and 23 days (oil products) by the national oil company |

|

Lao PDR |

21 days for companies importing oil and 10 days for distributers |

|

Malaysia |

30 days by the national oil company |

|

Myanmar |

6 days for oil companies |

|

Philippines |

30 days for refineries (crude) and 15 days (oil products) for companies importing oil |

|

Singapore |

90 days (oil products) for power companies |

|

Thailand |

21.5 days (oil crude) and 3.5 days (oil products) for refineries and traders |

|

Viet Nam |

10 days (oil crude) and 40 days (oil products) for oil companies |

Well-managed energy transitions will shield Southeast Asia from the impacts of volatile international markets, but energy security during transitions does not come for free

Russia’s invasion of Ukraine has had profound consequences for energy markets, leading to high and volatile prices for fossil fuels and greater near-term competition for non-Russian supplies. The market turbulence has shone a spotlight on the energy security vulnerabilities of Southeast Asian countries and their mechanisms in place to weather supply disruptions.

The region has been an aggregate oil importer since the mid-1990s and high oil prices put significant strains on consumers and the broader economy. In 2020, the region imported around 2.6 mb/d of oil (Thailand and the Philippines accounted for 40% of total oil imports to the region), mainly from the Middle East and Africa. In the STEPS, oil imports continue to rise to 4.6 mb/d in 2030 and 6.2 mb/d in 2050. Based on today’s policies, the region becomes a net natural gas importer by 2025, importing more than 130 bcm per year by 2050. However, the 2021 price increases – further accentuated by the invasion of Ukraine – may have long-term repercussions for the role of natural gas in the region, by changing perceptions on affordability and policy attitudes towards investments in gas import infrastructure.

Accelerating clean energy transitions is the key way to reduce today’s energy security vulnerabilities. In the SDS, for example, both oil and gas imports in 2050 are 50% lower than in the STEPS. This occurs because of the enhanced efficiency measures that are deployed in the SDS.

Targeted investments in energy security remain critical throughout energy transitions. Electricity demand rises rapidly in all our scenarios, as does output from variable renewables (wind and solar PV). Ensuring electricity security under these circumstances requires large-scale investments in networks, demand side management, digitalisation, enhanced cyber resilience as well as inter‑regional planning. Even as the region takes policy steps to move away from oil, oil stockpiles remain an important mechanism to protect against supply disruptions. There are a number of mandatory operational oil stockpile regimes for companies operating in Southeast Asia. These are generally equivalent to fewer than 40 days of oil use (and in some cases as few as 6 days). Many countries in Southeast Asia have studied or discussed establishing strategic reserves, and a reserve in Viet Nam has already started operation. International cooperation can also play a role by helping to build oil-sharing arrangements with neighbouring countries.

Southeast Asia must attract much higher levels of energy sector investment to accelerate its clean energy transition and meet the rising demand for energy services

Average annual energy investment in Southeast Asia, 2016-2030

OpenEnergy investment: attracting finance requires upgrading clean energy policy and regulatory frameworks and addressing a wide range of financial hurdles across the sectors

Southeast Asia faces the twin challenges of increasing total investment in the energy sector while increasing the share of this investment going to clean energy technologies. Between 2016 and 2020, annual average energy investment in Southeast Asia was around USD 70 billion, of which around 40% went to clean energy technologies – mostly solar PV, wind and grids. Energy investment in the STEPS reaches an annual average of USD 130 billion by 2030 and in the SDS it reaches USD 190 billion.

Improving regulatory and financing frameworks would help Southeast Asia reduce the costs of clean energy projects. For example, the levelised cost of energy (LCOE) of solar PV in Indonesia could be around 40% lower if its investment and financing risks were comparable to advanced economies. Boosting investment in clean energy technologies requires strengthening clean energy policy and regulatory frameworks and addressing a wide range of financial hurdles.

Well-designed frameworks – including clear policy targets, independent regulation, least-cost system planning and cost recovery tariffs – are crucial to attract investors. There has been progress on policy and regulation in many parts of Southeast Asia, including more ambitious climate targets announced by Indonesia, Malaysia, Thailand and Viet Nam, updated expansion plans for renewables, and changes in power purchasing agreements (PPAs). However, uncertainties remain in many countries over remuneration mechanisms and tariff levels for renewable output, which affect risk perceptions and the cost of capital for clean energy projects. Commitments and policies to phase out unabated coal plants and deploy low-carbon fuels would send important long-term signals to investors.

Cross-cutting issues such as unpredictable regulatory frameworks, restrictions on foreign direct investment and currency risks all hamper investment flows. Many countries have shallow financial and capital markets, and domestic banks have limited experience in financing clean energy assets. Long-term, low-cost debt is often not available and access to international private capital can be a challenge. Sustainable debt issuance by countries in Southeast Asia comprises around 3% of the global total, less than half the region’s share of global GDP (more than 80% of sustainable debt is issued in advanced economies).

International development finance has a key role to play in catalysing private funds, especially for projects at early stages of development, new technologies (e.g. CCUS, or carbon capture, utilisation and storage), and technologies with specific risks (e.g. exploration risk in geothermal). Improving access to finance would enhance investment by households and small-and-medium enterprises (e.g. establishing credit ratings for end-users and bundling small transactions).

Low emissions fuels: a key part of transitions in Southeast Asia…

…as the region is well-placed to tap into significant resources of bioenergy and hydrogen as well as CO2 storage potential

Southeast Asia’s energy transition depends primarily on the rollout of renewables, improvements in efficiency and the electrification of end uses; together, these close well over 50% of the emissions gap between the STEPS and SDS in 2050. There is also a significant role for low emissions fuels, such as modern bioenergy, hydrogen, hydrogen-based fuels, and CCUS. Including natural gas – when it replaces coal and oil – low emissions fuels close 30% of the emissions gap between the STEPS and SDS in 2050.

Modern forms of bioenergy can displace fossil fuels in transport, industry, clean cooking and power generation. Several countries in Southeast Asia have robust mandates to blend transport biofuels and policies to support co-firing, biogas and biomethane, as well as modern cookstoves. To ensure the environmental benefits of bioenergy, feedstocks need to be sustainable, and avoid competition with food production and negative impacts on biodiversity.

Low-carbon hydrogen and hydrogen-based fuels such as ammonia and synthetic hydrocarbons can help reduce emissions from long-distance transport and heavy industry. Co-firing ammonia in thermal power generation can also help provide a dispatchable low-carbon generation fuel. Brunei Darussalam has started exporting small quantities of hydrogen to Japan, while Indonesia, Malaysia, the Philippines and Thailand are piloting green hydrogen and fuel cell systems for power provision. Malaysia and Indonesia are conducting feasibility studies to co-fire ammonia in coal power plants, and there are plans to do so in Singapore, Thailand and Viet Nam.

CCUS can reduce CO2 emissions from the production of low-carbon hydrogen from natural gas and during fuel production or combustion. At least seven large-scale CCUS projects are in planning in Southeast Asia, including several linked to enhanced oil recovery and natural gas processing with offshore storage.

In the SDS, the share of low emissions and abated fuels reaches 50% of total liquid, solid and gaseous fuel demand by 2050. Investment in these fuels averages around USD 10 billion per year to 2050, around half of the level of today’s investments in fossil fuels.

Several regulatory hurdles and market risks must be addressed in order to scale up the deployment of low-carbon fuels in Southeast Asia. Even with higher fossil fuel prices, affordability remains a concern and several low emissions technologies and fuels are not yet mature or cost competitive. International collaboration and support are crucial to encourage investment and mitigate financial risks. Indonesia and Malaysia are cooperating with Japan to develop hydrogen, ammonia and CCUS supply chains. Similar initiatives are underway in Thailand and Singapore. Some major oil and gas players, such as Petronas, Pertamina and PTT have formulated plans to invest in hydrogen supply chains and carbon capture projects, often in partnership with international oil companies.

Power flexibility: growing deployment of wind and solar will require a more flexible power system – this must be a higher priority for governments and regulators

Power generation and shares of variable renewables in Southeast Asia in the Sustainable Development Scenario, 2020-2050

OpenPower flexibility: less rigid contracts for power generation and fuel supply can play a vital role, alongside strengthened and more integrated regional grids

Electricity demand is set to grow rapidly in the coming decades in Southeast Asia and an increasing share will be met by variable renewable sources. In the SDS, for example, the generation share of variable renewables increases from 2% in 2020 to 18% in 2030. The need for flexibility outpaces electricity demand growth.

Coal and gas-fired power plants are the region’s main sources of electricity today but they can also play key roles in providing flexibility. Achieving this role change requires changing existing contracts. There is a heavy reliance on physical PPAs in Southeast Asia, especially in vertically integrated power systems such as Indonesia and Thailand, where many plants were financed with physical PPAs with large capacity payments and/or take-or-pay obligations. If assets or entities have a contract that ensures operators a minimum daily load, the assets have no incentives to act flexibly.

Most of these PPA contracts extend beyond 2030. In Thailand, for example, minimum-take capacity in all contracts decreases by only 10% to 2030. Without any changes, it will not be easy to repurpose existing assets to offer flexibility, even as the share of variable renewable capacity increases. Further policy efforts to increase the flexibility of PPAs and fuel contracts are needed, for example through voluntary auctions.

The IEA analysed contractual flexibility issues in Thailand and found that cost savings from shifting towards more flexible PPAs and fuel contracts could be significantly greater than the savings from investing in technical flexibility resources. Designing contracts with sufficient flexibility leaves headroom for lower operational-cost variable renewables, and technical assets that provide critical system services to participate in the market, resulting in overall cost savings.

Regional integration and multilateral power trading can also help increase power system flexibility in Southeast Asia. This would expand balancing areas, allowing for efficient resource sharing, particularly for renewable resources. ASEAN has a major programme devoted to developing multilateral power trade – the ASEAN Power Grid (APG) – encompassing both building physical infrastructure and creating markets for multilateral power trade

Global demand for critical minerals in clean energy technologies is set to grow rapidly, providing a big opportunity for Southeast Asia to make the most of its large mineral resources

Potential revenue from selected minerals in Southeast Asia in the Sustainable Development Scenario, 2020-2050

OpenCritical mineral resources can be successfully and sustainably exploited by enhancing capacity building across the region and attracting investment in a wide range of projects

Southeast Asia is set to play a major role in clean energy supply chains, both as a consumer of low-carbon technologies and as a key supplier of critical minerals. Today, Indonesia and the Philippines are the two largest nickel producers in the world; Indonesia and Myanmar are the second and third largest tin producers; Myanmar accounts for 13% of global rare earth elements production; and Southeast Asia provides 6% of global bauxite production.

The mining sector has historically been an important contributor to government revenues, GDP and employment in Southeast Asia. Yet investment in mineral exploration has declined in recent years: the region’s share of the global mineral exploration budget has halved since 2012. This trend will need to be reversed if Southeast Asia is to realise its potential in the critical minerals sector, and offset likely future declines in coal mining jobs.

Investment in processing and manufacturing to develop critical-mineral based industries can help extract additional value from Southeast Asia’s natural resources. Malaysia and Viet Nam are the world’s second and third largest manufacturers of solar PV modules. Thailand is the 11th largest vehicle manufacturer in the world and could also become a key hub for the manufacturing of EVs. Indonesia is implementing policies to attract mid to downstream battery industries. If the region can develop domestic value chains for multiple industries, the revenue from the production of nickel, tin, copper and rare earth elements in Southeast Asia could grow by almost 2.5-times to nearly USD 60 billion by 2050 in the SDS.

Ensuring high environmental, social and governance (ESG) standards is crucial for the region as consumers and investors increasingly demand that manufacturers use minerals that are sustainably and responsibly produced. For example, high-pressure acid leaching (HPAL) projects are expected to supply battery-grade nickel products in this region, but these projects need to resolve concerns over their high levels of emissions and water consumption. In the downstream sector, encouraging recycling is key: secondary production of aluminium accounts for just 2.5% of total refined consumption in the region, compared with 25% globally.

Enhancing capacity building efforts across the region is central to ensure the sustainable development of mining industries and to attract investment in a wide range of projects. This includes technical capacity building (e.g. geological surveys, reserve estimation, sustainable mining practices) and institutional capacity building (e.g. regular ESG assessments) for sound governance and transparent regulations.