Cite report

IEA (2022), How Governments Support Clean Energy Start-ups, IEA, Paris https://www.iea.org/reports/how-governments-support-clean-energy-start-ups, Licence: CC BY 4.0

Report options

Six reasons governments support clean energy start-ups

Government support for start-ups, including sector-specific support, is not new, but targeting clean energy start-ups is a relatively recent phenomenon. A number of factors initiated this trend, including greater ambition by some of the world’s largest economies to transition to clean energy, and higher expectations for new market entrants to disrupt markets, redirecting them towards more sustainable products. In addition to policy support, this trend to support clean energy start-ups is also manifest in the larger number of incubators and accelerators that focus on clean energy solutions at universities and in the private sector, as well as in dedicated venture capital funds and stakeholder networks.

1. Without more innovation, energy and climate goals will be out of reach

There is wide agreement that meeting the climate challenge will depend on accelerating clean energy technology innovation, as the energy sector is the source of around three-quarters of global greenhouse gas emissions. However, rising demand for energy services is inseparable from a growing global population with aspirations for a better quality of life.

Almost half of the emissions the world needs to avoid to achieve net zero emissions by 2050 cannot be tackled with technologies on the market today. Rather, cutting these emissions will require technologies that are still at the demonstration or prototype stage, mostly in sectors such as heavy industry and long-distance transport. Even in other sectors, however, it is difficult to imagine low-carbon energy penetrating all corners of the global economy without continued performance improvements, cost reductions and adaptation to diverse local contexts.

This concerns the use of renewable energy in new applications, for instance in industry, heating and transport, and for enabling technologies that connect energy supplies to end uses, such as batteries, grids and hydrogen technologies. Despite some encouraging signs in the past three years, patenting activity in low-carbon energy technologies has largely plateaued since 2013 instead of resuming the rapid growth rate of earlier this century.

One oft-overlooked challenge is the development of affordable high-quality technologies appropriate for companies and individuals in emerging market and developing economies. In the IEA Net Zero Emissions by 2050 Scenario, more than 40% of global energy investment is in these countries, and many clean energy technologies also promise the added benefits of reducing air pollution and enlarging energy access.

Global CO2 emissions changes by technology maturity category in the Net Zero Scenario

Open2. Energy innovation is expanding thanks to start-ups

Much past energy innovation originated from large companies that benefit from considerable market power. These companies, mostly in energy supply sectors but also in industry and transport, operate sizeable research facilities and control extensive infrastructure and markets for deploying new technologies. This innovation model was attractive because it offered the economies of scale and precision engineering necessary to develop and market nuclear energy, fuel processing and combustion technologies; entrepreneurial start-up firms have therefore played a smaller role historically.

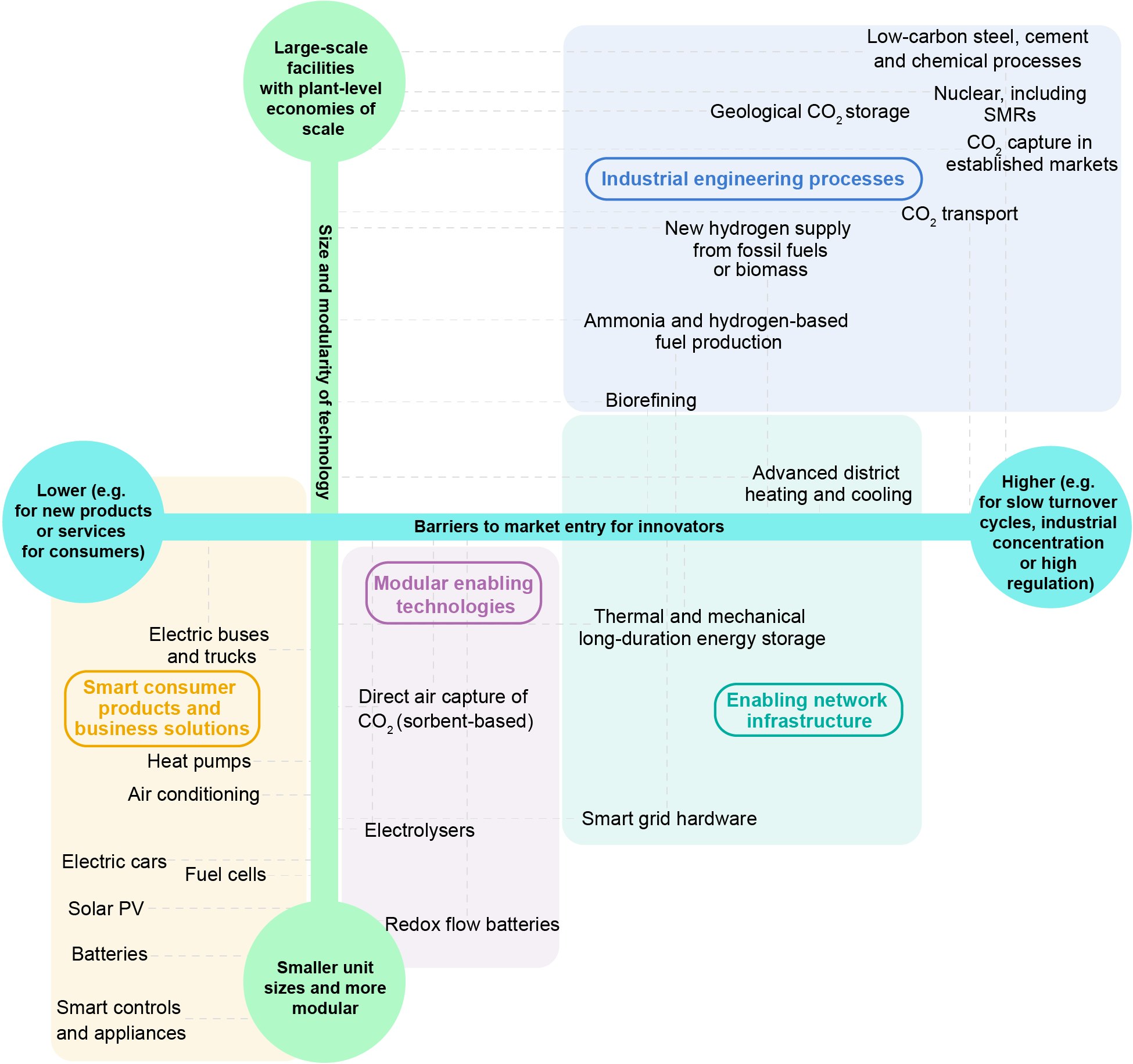

However, with regulations leading to market decentralisation and greater attention being paid to environmental performance, the scope of energy innovation has broadened. A wider range of energy sources, smaller-scale technologies and their associated energy system challenges have now become mainstream.

Technologies that have a small unit size, replacement cycles of less than 20 years and high levels of standardisation, modularity and mass production (e.g. solar photovoltaics and batteries) are increasingly present in numerous areas of the energy system. In terms of packaging for end users, they lend themselves to greater product differentiation (i.e. they can be branded according to their distinct characteristics) and are generally unsuited to vertical value chain integration and horizontal monopoly ownership. Barriers to market entry for start-ups also tend to be lower for these technologies.

Furthermore, since energy technologies increasingly rely on digital and “deep-tech”1 advances, fast-growing start-ups are playing more important roles. But regardless of the technology, healthy conditions for start-ups tend to spark new ideas and facilitate the transfer of solutions to new applications and societal challenges.

Low-carbon energy technologies by unit size and modularity vs market entry barriers

Open

{kind=link}

The policy imperative to accelerate energy transitions means that governments must take an increased interest in start-ups. Large incumbent firms typically prefer incremental innovation that realigns their existing practices with market trends to the greatest extent possible. This results not so much from a philosophical outlook as from the reality of needing to account for the net present value of existing assets, skills and political alliances.

Conversely, start-ups carry more risk, with investors taking a portfolio approach to bet on possibly high future returns and having greater tolerance for failure than corporate shareholders do. Nevertheless, large corporations continue to be very important in getting new technologies to market, acting as innovators, customers, investors in start-ups and acquirers of start-ups. Corporate venture capital investments in energy technology start-ups have been rising since 2018, amounting to over USD 5 billion in 2020.

3. Energy technology companies are underfunded by private capital

Clean energy technologies are not always well suited to the prevailing venture capital model, which emerged primarily to support information technology start-ups. There is a mismatch between the short time horizons of most venture capital funds (which promise to return capital to investors in around five years) and the longer timelines and large upfront investments needed by developers, particularly of energy hardware. Furthermore, energy technology developers must often overcome many technical, commercial and regulatory hurdles to become sustainable businesses.

One of these obstacles is the lengthy process of creating and implementing the essential government market-creation policies that most of these start-ups will eventually rely on to attract customers. Moreover, since the cleantech bust of around 2011, when investors in early-stage clean energy start-ups lost money because of these mismatches, many venture capital funds have focused on asset-light business models in the energy sector, leaving hardware developers with fewer options for raising capital.

4. Nurturing start-ups to maturity creates local economic prosperity

Economic renewal and growth are usually core policy objectives of government support for energy innovation. Governments (including local ones) therefore aim to help the originators of new technological ideas (who have often benefited from public grants) expand their business to a critical mass of operations in the region. Before attaining this critical mass, a limited number of jobs are typically created for well-educated R&D engineers and business developers. At this stage, there is a risk of investors moving their start-ups out of the region, for example to be closer to an investor’s own ecosystems or to where innovation support is already strong.

Only after the critical mass is reached and sales begin to scale up does the community begin to benefit from employment opportunities in manufacturing, sales and after-sales service. At this stage, start-up owners are more likely to let companies grow where they are, or even make them into strategic divisions of global operations, instead of relocating activities and key people. In addition to offering direct support to individual entrepreneurs, successful regions cultivate a variety of local attributes to create innovation ecosystems that are competitive in their technology areas.

In the clean energy domain, many governments seek inspiration in the success stories of BYD, Northvolt, Plug Power, Tesla and, further back, Vestas. Ten years after its founding in California in 2003, Tesla’s Fremont factory in that state was employing 3 000 people. On the other side of the Atlantic, it has been estimated that Denmark’s early leadership in wind energy in the 1980s, through innovative technology firms such as Vestas, has created a local ecosystem that supports 9 000 jobs in Denmark for every 1 GW of offshore wind capacity installed in the European Union.

However, the balance between maintaining both domestic innovation support policies and competitive international markets is often delicate. This balance, which is a focus area of the Global Commission on People-Centred Clean Energy Transitions, can be fostered by stronger international co‑operation to address social objectives such as equity, inclusion and gender equality.

5. Clean energy transitions will be a major market opportunity for all countries, all century long

Achieving net zero emissions will require an unparalleled increase in clean energy investment. In fact, the IEA Net Zero Emissions Scenario indicates that annual investments in clean energy must more than triple to USD 4 trillion by 2030. Although mobilising such a considerable sum will be challenging, this investment will not only ensure clean energy transitions but also offer unprecedented market opportunities for equipment manufacturers, service providers and developers, as well as engineering, procurement and construction companies along the entire clean energy supply chain.

Indeed, the markets for wind turbines, solar panels, lithium-ion batteries, electrolysers and fuel cells combined represent a cumulative (i.e. up to 2050) market opportunity of USD 27 trillion. In the Net Zero Emissions Scenario, the Asia Pacific region is home to 45% of the estimated market for clean energy technologies up to 2050. This is a momentous opportunity for the best innovators from all over the world to become part of emerging value chains that have enormous future potential. However, some innovators in emerging market and developing economies will have to overcome or reshape the existing networks of knowledge and capital that have led technology developments in the past.

For start-ups working on clean energy technologies, welcome attention from sustainability-oriented investors and customers will also entail pressure to meet certain criteria. Increasingly, capital allocations to energy companies and projects involve scrutiny for compatibility with environmental, social and governance (ESG) goals. Start-ups may be well positioned to meet this growing demand for ESG-aligned equity, products and services, and opportunities to partner with established firms that need to address their emissions profile will expand further in upcoming years. However, as young companies have only limited resources to measure and document their performance to the required standards, targeted tools or support may be needed to prevent this from becoming an additional barrier to market entry. (The chapter Policy Insights contains more information on estimating the potential emissions impacts of start-ups.)

6. Clean energy entrepreneurship emerged as an economic recovery opportunity during the Covid-19 pandemic

The lockdowns and slowdowns in economic activity accompanying the Covid-19 pandemic have hit SMEs particularly hard. Small firms have insufficient capital buffers, with start-ups often surviving by raising small amounts of financing at frequent intervals. In early 2020, a number of governments extended bridging capital to start-ups in this position to avoid losing high-potential companies and their knowledge. This action also reflects the philosophy that economic recovery can be stimulated by investing in fledgling companies that could seed local economic growth. Since mid-2020, government plans have included investments in clean energy technology areas that aim to redirect and sustain recovery over the longer term.

In parallel, clean energy venture capital investments have not contracted and have become more evenly distributed internationally. Investors are increasingly convinced that energy transitions are happening, and that they will be underpinned in the near term by proactive government recovery policies and robust corporate demand. Compared with traditional sectors, investors are attracted to the higher return potential of technology companies. However, most venture capital and private equity capital targets companies that already have products to demonstrate and sell (TRL 8-9), meaning that only a relatively small portion of the sizeable capital available to invest in sustainable innovation-led recovery is being allocated to early-stage start-ups looking for investment.

While company valuations have risen in the past year and several high-profile recent start-ups have been listed on stock exchanges despite not yet being profitable, the sustainability of this momentum is uncertain. Governments could fortify their role as supporters of pre-commercial technology ideas through R&D funding and could also help any resulting early-stage companies quickly become attractive to venture capital and private equity investors. Governments may also need to look ahead to the possibility that, depending on how the economy evolves, the follow-on funding rounds of some start-ups securing large capital investments today may be smaller, slowing their growth and harming investor perception of the sector.

While virtual working environments have generally helped internationalise the matching of funds with start-ups, this may exacerbate challenges for governments seeking to establish manufacturing and hardware centres in their regions. Governments can work with innovators and investors to identify how to reconcile this conflict, including through R&D funding, support to start-ups and regulatory changes. As venture investment in clean energy spreads around the world, more regions will have the chance to participate and compete with the United States, which has been the primary source and destination of early-stage private capital. This could raise the overall pace of innovative activity, to the benefit of all.

Global early-stage venture capital investments in energy technology start-ups

OpenReferences

Deep tech refers to applying advances in basic science areas to engineering and societal challenges to generate new classes of solutions to improve existing technologies, outside the scope of more incremental R&D. Advanced materials, advanced manufacturing, artificial intelligence, biotechnology, blockchain, robotics, photonics and quantum computing are all typically considered deep tech fields.

Reference 1

Deep tech refers to applying advances in basic science areas to engineering and societal challenges to generate new classes of solutions to improve existing technologies, outside the scope of more incremental R&D. Advanced materials, advanced manufacturing, artificial intelligence, biotechnology, blockchain, robotics, photonics and quantum computing are all typically considered deep tech fields.