Attracting private investment to fund sustainable recoveries: The case of Indonesia's power sector

World Energy Investment – Country focus

About this report

Introduction

Emerging economies, like Indonesia, have an opportunity to support recovery...

On the back of the worldwide shock caused by the Covid-19 pandemic, economic recovery will depend largely on the ability of countries to finance and implement supportive fiscal packages. The crisis also marks an opportunity to promote development aligned with longer-term sustainability goals, with the energy sector central to these efforts.

A number of governments, primarily in advanced economies, have announced large programmes to address the impacts of confinement measures and stimulate the economy. France’s fiscal package is around 5% of gross domestic product (GDP), the United States close to 11% and Japan above 20%. However, many emerging and developing economies – which account for the majority of the world’s population and future energy investment needs – have lower fiscal capacity and ability to raise long-term, low-cost debt. In addition to a steep reduction in aggregate demand, investment uncertainties have prompted capital outflows and rising borrowing costs in a number of markets. Many of these countries also depend heavily on foreign direct investment, which is expected to fall by up to 45% in developing Asia this year17.

Emerging economies will need to structure recovery packages wisely and be innovative in attracting capital from different sources. Solutions that work in advanced economies may not be feasible, nor the right fit, for emerging economies. When it comes to energy investments, the cost of financing – a major determinant of the economics of more capital-intensive clean energy technologies – remains high in most emerging countries. Public support, including from international development institutions, is often critical to enhance the investment proposition of renewables. With emerging and developing countries expected to account for 90% of global power demand growth over the next decade, there is a large untapped potential for cleaner sources to play a more prominent. This is particularly true in Indonesia – the largest economy in Southeast Asia and an International Energy Agency (IEA) association country – where the electricity sector lies at the heart of sustainability and economic development goals.

Despite Indonesia’s good progress in electrifying nearly all its population and increasing investment, current power sector trends are not aligned with stated policy ambitions and are out of step with what would be required to meet energy-related Sustainable Development Goals in full (namely the goals of the Paris Agreement and the push to dramatically reduce energy-related air pollution). More than 100 million people have obtained access to electricity since 2010, a major achievement. However, while economic growth has brought benefits, such as increased ownership of vehicles and appliances, it has also created new environmental pressures.

Power-related carbon dioxide emissions have increased by two-thirds since 2010. Fossil fuels account for nearly half of power investment; of that, about 85% is in coal generation. Indonesia has a young but relatively inefficient fleet of coal power plants, with additional capacity under construction. Investment in renewables remains far below its potential.

Policy signals will shape future investments and Indonesia’s ability to meet a target of 23% renewables in primary energy by 2025. To this end, the government is set to announce a revised renewables policy framework, with a new remuneration scheme. Its success will depend upon addressing investment conditions and policy design aspects that are critical to the mobilisation of signficant new capital to the sector.

... in a manner that attracts private capital for development and a sustainable energy transition

The current global economic crisis makes the implementation of this renewables policy framework and the mobilisation of finance potentially more challenging, but it also presents an opportunity to chart a new direction for the economy, with new sources of capital and expertise in a sector with high growth potential. In addition to clear and predictable policy reforms, public sources of finance, including from domestic and international development institutions, will be critical to help address investment risks and crowd-in international sources of private capital. The existing fiscal space needs to be used wisely, while an improved policy, regulatory and investment framework can help mobilise a more diverse pool of sources of funding, especially from new investors and private-sector industry players.

This report aims to analyse the investment and financing factors influencing Indonesia’s shift towards a more sustainable power system and potential implications for government decision making. First, it tracks the investment and financing trends in Indonesia’s power sector, quantifying capital expenditures and assessing future spending needs under a sustainable pathway. It characterises the availability of funds from public and private sources, mapping the sources of finance by provider, origin and instrument. The report then identifies key issues affecting investment decisions in renewable power generation, as well as in key sources of flexbility, such as electricity networks. Finally, it details three key factors for consideration in policy making:

- Attracting higher levels of capital would be improved by strengthening the funding model for state-owned utility PLN, the owner and financier of most of the power sector assets and counterparty to all private generators. A financially sustainable PLN would mean a lower burden on public finances and would allow PLN to continue focusing on investing in enabling infrastructure (particularly transmission and distribution, where the private sector is very limited). It would also help reduce the perceived revenue risk.

- Improving investment framework for renewables, including:

- Clearly addressing issues on procurement and tariff levels, as in the envisaged presidential decree on renewables, in line with the market consultations already undertaken.

- Setting a programmatic approach for auctions with standard, bankable power purchase agreements (PPAs), to help achieve volume while addressing land acquisition barriers.

- Avoiding boom-and-bust cycles.

- If applied, industrial policy should be formulated taking into account Indonesia’s comparative advantages. A support for renewables could help create high-quality jobs in areas of engineering and project finance, which can have positive effects in others parts of the energy and infrastructure sector.

This report is part of a broader engagement between the Ministry of Energy and Energy Resources (MEMR) of Indonesia and the IEA to provide policy support and tailored analyses to tackle key power system challenges, including also system integration and flexibility. IEA-MEMR collaboration has been strong since 2015 and was further solidified in December 2019 with the signing of a robust Joint Work Programme covering key energy issues.

Reliable electricity supply is crucial as Indonesia’s economy recovers from the Covid-19 crisis, and there is a huge opportunity to boost sustainable investment as part of the recovery

Power investment trends in Indonesia

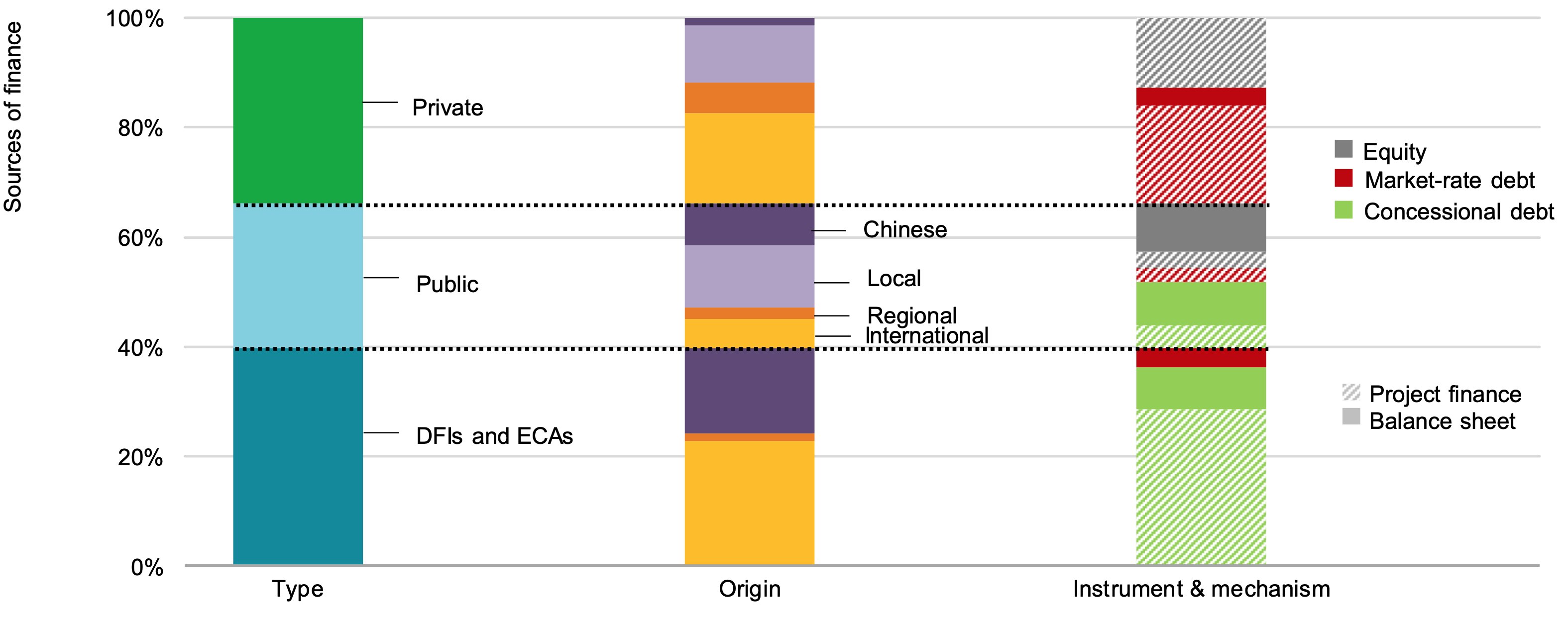

OpenInternational funds and concessional debt have played a key role in financing power investments

Share of sources of finance in the power generation sector of projects commissioned in 2016-2019

Open

{kind=link}

Public sources and SOEs have played a bigger role in financing fossil fuel power compared with renewables, where private sources accounted for around half of the funds invested

Sources of finance of projects commissioned in 2016-19 by type of funds

OpenThe coal-fired fleet is young and growing, with most of the financing coming from within Asia and lower-cost debt accounting for nearly a quarter of funds

Indonesia’s progress in modernising its power sector could be set back by the pandemic; mobilising new private sources of finance, especially for renewables, will be critical

Around 100 million people have obtained access to electricity in Indonesia since 2010. Investment in power also increased over the period; according to IEA estimates from the World Energy Investment report, annual investment grew by almost 50% since the early 2010s, compared with 15-20% in all developing economies overall. However, at below USD 12 billion, capital spending slowed in 2019 and is set to decrease again in 2020 due to the Covid-19 pandemic.

Almost three-fifths of annual power investment in 2019 was on generation. Fossil fuel power continued to represent the majority of spending in generation (80%) – especially coal power, where over 60% of the existing fleet is ten years old or younger. For every dollar invested in renewables, more than three dollars was spent on coal-fired plants. Investment in renewables has been held back by an uncertain regulatory environment – despite ambitious renewable targets – with the majority (around 80%) in hydropower and geothermal. The medium- to large-size nature of these projects has helped attract funding and reduce transaction costs.

Investment in electricity grids remained flat compared with 2018. Higher grid investment will be key to ensure full electricity access, to connect islands and interconnect with neighboring countries. While today’s penetration of renewables remains low, future spending in grids will also be needed to ensure a balanced and secure power supply as renewables begin to play a greater role in generation, and to avoid local hotspots, especially given the challenging, dispersed topography.

An analysis of the sources of finance gives an indication of the ability of the sector to raise different types of funds and its level of maturity and risk. More advanced economies generally have access to diverse funds, and public funds are less prominent. In Indonesia, around a third of the funds for plants commissioned between 2016 and 2019 came from private sources. Around 40% came from DFIs and ECAs (this also includes export-import banks). The majority of public sources (mainly from SOEs) were used to finance fossil-based power.

Three-fourths of the assets were financed with debt and a quarter with equity. Almost half of the debt was concessional, mainly from DFIs and ECAs. In terms of origin, almost half of the debt was provided by banks based in the People’s Republic of China or in Southeast Asia with the majority of their operations also in the region (e.g. Bank of Malaysia). Debt from local banks accounted for less than a tenth of the total.

International sources represented almost half the finance to the power plants commissioned over 2016 19. However, they accounted for only 10% of the financing for coal-fired generation; the rest came from Chinese (43%), regional (20%) and local entitites (26%). Private international sources were more limited, though; they accounted for less than 20% of the total financing, and less than 5% for coal power.

Given constraints on public budgets, private actors are likely to be key to scaling up capital, especially for renewables, to align with a more sustainable investment pathway. Attracting such financing is likely to become more challenging in 2020 given the global economic crisis, reinforcing the importance of reforms to improve Indonesia’s power sector investment framework and enabling environment, which is currently a key priority for policy makers.

Renewable power costs are relatively high in Indonesia, in part due to persistent risks

Average levelised cost of electricity for new utility-scale solar PV commissioned in Indonesia, 2019 versus benchmark

OpenInvestment in renewable power currently faces challenges, which has slowed progress in growing the sector and making renewables more affordable in Indonesia …

Renewable power installed capacity was around 10 GW in Indonesia by the end of 2019, a third of the coal-fired installed capacity and a sixth of the fossil fuel capacity. Half the installed renewable capacity was hydropower and a fifth geothermal. In contrast to the international situation, where solar PV and wind have grown rapidly, supported by persistent cost reductions, these dynamic technologies accounted for less than 5% of the installed capacity in 2019 in Indonesia..

Solar PV activity has generally been in the form of small- and medium-size projects, except for a large public-funded project under preparation, while other renewable projects have been mostly medium to large scale. Three 7 MW plants were commissioned in West Nusa Tenggara in 2019, as well as the largest solar PV project, a 21 MW plant, installed in North Sulawesi; a 72 MW wind project came online in 2019 (and another of similar size was commissioned in 2018) and much larger geothermal projects started operation that year and before. The four solar PV projects, as well as the 72 MW wind plant, were all financed on a project finance basis through a combination of debt provided by the Asian Development Bank and equity provided by a developer with experience in the region. In addition, PLN completed the tendering process for two 25 MW solar PV plants in 2019 and PJB, a subsidiary of PLN, recently signed a PPA with Abu Dhabi-based Masdar (a public entity) to develop a 145 MW floating solar PV plant on the Cirata Dam in West Java.

Despite falling over time, relatively high costs remain a key impediment for renewables development in Indonesia. For example, the average cost per megawatt of solar PV capacity is 65% higher than in India and 10% higher than in Thailand. In the case of onshore wind, costs remain much higher than other regions (though this also reflects a lower domestic potential). Clear policies and regulation, and competitive procurement, were key to cost reductions in the countries depicted.

Concerns around the bankability of PPAs (the way risks are allocated among actors) combined with low remuneration incentives have also hampered the ability to raise finance for projects. More than a third of the 75 renewable PPAs signed between 2017 and 2018 had not reached financial close by the end of 2019, and five were terminated9, many of which were for small-scale projects with higher transaction costs. In early 2020, the IEA talked with developers, investors and financiers based in Indonesia, who noted various investment risks challenging the scalability and affordability of renewables in Indonesia today, translating into high financing costs. These have been driven by three main types of perceived risks:

- country risks (issues around the country’s macroeconomic situation, including high benchmark interest rates, though this group of risks has been declining in recent years due in part to prudent fiscal policy and strong economic growth)

- policy and regulatory risks (permitting and project preparation barriers; local manufacturing capacity still in early stages to meet local content requirements; evolving regulatory landscape which makes long-term planning difficult; complex tariff design; etc.)

- revenue risks (or uncertainty of payment, which adds the largest premium to financing costs, arising from PLN’s financial situation and its history of renegotiating contracts in the past); high exploration risk in the case of geothermal projects.

… but improved investment frameworks, supportive policy design, and clear and predictable implementation of reforms could help attract the capital at scale needed for the sector

An improved policy and regulatory framework can help reduce some of the perceived risks and improve project bankability. With this in mind, the government of Indonesia (GoI) released a decree in early 2020 (regulation 4/2020) that included changes such as removing the requirement to develop projects on a build, own, operate and transfer (BOOT) basis – which caused difficulties for developers in terms of land ownership and ability to obtain financing – and allows projects on a build, own and operate basis. The decree also requires PLN to take renewable generation on a “must run” basis. However, other critical issues were not addressed, such as the remuneration mechanism and tariff level for renewables. These factors are expected to be included in an awaited presidential decree to be published later this year, which will set a (higher) feed-in-tariff for renewable projects below 20 MW and competitive auctions for larger projects (this would apply to solar PV, wind, hydropower, biomass and biogas). A clear and transparent final regulation would be critical to send a positive signal to the market, especially as investors are currently extra cautious given the overall uncertainty and the economic outlook in emerging economies.

In addition to an updated remuneration mechanism, some of the revenue-related risks could be reduced through risk mitigation instruments, such as guarantees, though these are generally not yet widely available in Indonesia. For example, the GoI offers two types of guarantees: a Business Viability Guarantee Letter (BVGL), to improve PLN’s ability to fulfill its off-taker and borrower obligations; and an Indonesia Infrastructure Guarantee Fund (IIGF), to cover political and public-sector risks. However, neither IIGF nor BVGL (which is not exclusive to renewable projects; e.g. almost 13 GW of coal-fired generation had benefited from it by the end of 2018) had been widely used for renewable projects4, in part because these guarantees are applied only to public-private partnerships (PPP).

Similarly, other instruments are ready to improve the risk-return profile of projects, such as contingent equity, mezzanine and blended finance, green bonds, and viability gap funding (to cover upfront project funding), to name a few6. Yet implementation is low. For example, PT SMI – an SOE under the Ministry of Finance created in 2009 to catalyse infrastructure investments – houses a geothermal fund that provides concessional loans to project developers (to reduce early-stage exploration risk), but its project portfolio is still limited. Plus, viability gap funding is also available only for PPP projects, which tend to be large-scale projects and limited.

A broader set of considerations – such as the permitting and licensing process, the credibility of the renewable targets, the ability of the grid to integrate increasing amounts of renewables, and the bankability of the underlying PPA – is also part of the overall investment framework that investors and financiers take into account.

A stregthened investment environment for renewables would help lower perceived risks and in turn reduce financing costs. If financing conditions in Indonesia were those of a benchmark advanced economy, the LCOE of solar PV would be around 40% lower. More confidence in the sector could also help develop supply chains and achieve economies of scale, pushing costs down. As competition intensifies, costs could reduce even further.

Investment in transmission and distribution – mostly publicly financed – flattened in 2019 after continuous growth. The government aims to attract private capital to bridge the “last mile”

Investment in transmission and distribution networks in Indonesia, 2015-2019

OpenKey differences between centralised and decentralised segments of electricity access

| On-grid access | Decentralised | |

|---|---|---|

| Asset type | Extension of existing distribution network | Mini-grids and stand-alone solutions (e.g. SHS) |

| Average annual investment to achieve and maintain full electricity access (2020-2030) | USD 100 million | USD 190 million |

| Sources of finance | Public (i.e. PLN) and DFIs | Public, private and DFIs |

| Average project size | Large | Small |

| Revenues and tariffs | Regulated tariffs (collected through electricity) | Prices not regulated for SHS; regulated for mini-grids only if developed under subsidy scheme |

More investment will be needed to expand and maintain the existing grid, and support the expansion of decentralised solutions, to achieve 100% electrification

Investment in electricity networks in Indonesia, at USD 5 billion in 2019, remained flat compared with 2018. Almost two-thirds was destined for transmission, with the rest to distribution.

The 2018 19 level of investment in transmission and distribution is impressive compared with previous years (about twice the level of the early 2010s). However, more capital will be needed to connect the different islands and ensure the system is reliable and able to integrate renewables successfully – which will play a major role in providing 100% electrification, especially in the least developed regions. As seen in other countries, an efficient and co ordinated expansion of the grid – which generally takes longer to develop than generation – is needed to ensure the timely commissioning of renewable technologies, some of which have short lead times. On average, 50% more spending would be needed per year over the 2025 30 period to meet the conditions of the Sustainable Development Scenario. Plus, capital will be needed to enhance storage and cross-country lines such as the planned Indonesia-Malaysia interconnector (which will enable power trade, including exports from a planned large hydro dam in North Kalimantan). PLN currently finances most large network investments, supported by long-term and concessional loans from DFIs and ECAs.

Capital will also be needed to provide and maintain electricity access to the entire population. According to IEA analysis, multiple approaches would be required in order to achieve universal electricity access by 2030. A quarter of the population gaining access by 2030 would do so via an expansion of PLN’s grid, while more than half would be through mini-grids and the rest through other decentralised solutions (i.e. stand-alone alternatives such as SHS).

The characteristics of the on-grid and decentralised access-related solutions are quite different. For example, the on-grid distribution sector is a regulated business, while mini-grid end-customer tariffs are regulated only when managed by PLN and using a state-backed subsidy scheme. For mini-grids managed by communities, the tariff is based on agreements among the community, which still need to be approved by MEMR. In addition, even if not using a subsidy, mini-grid projects must comply with conditions set by the state (e.g. on local content). The price of stand-alone systems are not regulated and competition among SHS suppliers is quite high in most countries across the world.

In addition, while the state has a legal monopoly on the transmission and distribution sector, the private sector can participate in the decentralised sector. In fact, the GoI is looking to attract private companies to help reach access to the “last mile”. Yet the majority of the decentralised assets were funded by the government with DFI support, and the private sector plays a role mainly as a service provider and not a financier15.

Uncertainty over the enabling environment (licensing, permitting, tariff setting, options when the centralised grid arrives) and the high cost to reach remote populations hamper increased privately financed remote electrification. Combined with broader institutional questions, Indonesia is regarded as a relatively nascent market for off-grid solutions, despite having significant potential. For example, Indonesia is one of the ten countries with the largest potential market of stand-alone systems, making up 4% of the global market13.

In terms of macroeconomic environment, Indonesia’s fiscal management has improved considerably, with debt levels that compare favourably to other emerging economies …

… but growing subsidies place a burden on the public budget and there are considerable constraints on capital availability from both the public and private sectors

PLN plays a crucial role in Indonesia’s investment framework, yet contractual burdens and lack of cost-reflective retail tariffs pressure its balance sheet and create a drag on public finances

IEA scenarios show that a much higher level of power investment and a major shift in its allocation will be essential to ensure reliable, affordable and sustainable electricity supply

Power sector investment in Indonesia in 2019 versus 2025-2030 average annual investment needs in the Sustainable Development Scenario

OpenIndonesia’s economy has performed well in recent years, but low access to long-term finance and high reliance on public entities are still key challenges to scale up power investments...

Indonesia’s economy, the largest in Southeast Asia, has performed relatively well in the recent years. The annual real GDP growth has been above 5% since 2015, and inflation stable at around 3%. Public debt management since the Asian financial crisis at the end of the 1990s has also been commendable. The budget deficit has been below the 3% limit (as a share of GDP) set in 2003, and the government debt-to-GDP ratio has been below the 60% limit. The government’s foreign reserves have also increased by 3.5 times since the early 2000s – providing some buffer amid financial outflows from emerging markets since the start of the Covid-19 pandemic and as local currencies devaluate, including the Indonesian rupiah.

Despite this progress, capital is relatively constrained in Indonesia, from both the public and private sides. Given the long-lived nature of power projects, the availability of long-term finance is crucial to ensure investment in the sector and a more sustainable power mix. Government revenues in Indonesia (as a share of GDP) are low compared with other economies, despite the high level of public participation and financing in the energy sector. According to the International Monetary Fund (IMF), “low fiscal revenues have also resulted in reliance on SOEs” and there are increasing fiscal risks from sovereign guarantees extended by SOEs11. In addition, government revenues are expected to decline in 2020 given the global economic crisis and the drop in oil and gas prices, putting more pressure on public finances.

On the private side, the ability to raise long-term financing is also quite limited. Banks are the largest actors, holding about 75% of the financial sector assets, but the level of private credit to GDP is considerably below that of peer countries. In addition, most banks limit the duration of loans to eight years1. The bond market, which can be a good complement, is also small. It represents only around 18% of Indonesia’s GDP, compared with much higher figures in other countries in the region (e.g. Malaysia 101% or Thailand 76%) 2. Other investors, such as insurance companies and pension funds, also have a relatively limited participation in Indonesia’s financial sector.

Growing energy subsidies to consumers put additional pressure on the public budget. Fuel and electricity subsidies lowered over 2015 17, given the oil crisis, but climbed up in 2018, driven mainly by an uptake of fuel subsidies related to frozen tariffs. As part of the fiscal package created to respond to the crisis, the GoI broadened coverage of electricity subsidies and announced that PLN would provide free electricity to 24 million people (those in the lowest tariff category) and a 50% discount to another 7 million people (those in the second-lowest category) over three months. For 2020, PLN recently announced a 13% increase in the subsidy requirement compared with the 2019 level (relative to a 4% increase planned before the crisis) – though these could be optimistic estimates according to our calculations.

Apart from low retail tariffs, subsidies to support PLN’s balance sheet stem largely from a increasing costs of power and ambitious expansion planning (based on overly optimistic load forecasts). In particular, PLN’s take-or-pay contract obligations with thermal IPPs, which require the payment of fixed capacity charges, are set to continue growing.

Conclusion

An enhanced investment framework for renewables and reforms that attract higher levels of private capital would help support sustainable economic recovery in Indonesia

Overall, the fiscal response announced by the GoI in March (around USD 25 billion and 2.6% of the GDP) focuses, understandably, on increasing benefits for lower-income households and supporting the most affected sectors, such as health and tourism. This includes expanding testing and treatment capability and increasing unemployment benefits and tax relief. Apart from the government’s own funds, part may be financed with support from international finance institutions such as the IMF or DFIs, or the bond market. For example, in April the GoI raised USD 4.3 billion to fund the recovery, including a 50-year tranche worth USD 1 billion.

The power sector will be important for Indonesia’s economic recovery and given the pressing investment needs across the economy, the public funds available for the power sector should be used prudently, creating the enabling environment for private funds to bridge the gap.

Attracting higher levels of capital will first require a reliable funding model for PLN, the owner and financier of most of the power sector assets and off-taker to all private generators. Effective planning and better governance would help improve the financial and operational efficiency of the company. A strategy to reduce the burden of legacy assets would likely be needed too, and there are initiatives designing refinancing solutions to tackle this. A financially sustainable PLN would mean a lower burden on public finances and would allow PLN to focus on investing in enabling infrastructure (particularly transmission and distribution, where the private sector is not allowed to participate) while ensuring the electricity supply remains reliable and secure. It would also help reduce perceived revenue risks for generators.

Second, an improved investment framework for renewables could help increase competition and achieve generation at lower cost. Indonesia is a large and growing untapped renewables market with the scale to attract international players. If the conditions are right, capital will come. In practical terms this means:

- Publishing the presidential decree on renewables in a timely manner and clearly addressing issues on procurement and tariffs levels, in line with market consultations. Market players are eager to see this.

- Setting a programmatic approach for auctions (e.g. programmes of several small-scale projects that can be bundled together, following and learning from cases such as the four solar PV and wind projects commissioned in 2019) with standard, bankable PPAs. This could help developers achieve volume while reducing the barrier of obtaining large areas of land.

- Avoiding boom-and-bust cycles by adjusting incentives over time according to market conditions. This approach would also help to target limited public funds more efficiently, for financial risk mitigation and finance intermediation that catalyses private funds, through for example a stronger role for PT SMI, complemented by DFI support and expanded use of existing instruments.

Finally, a push for renewables would help create jobs while reducing emissions. If applied, industrial policy should be formulated taking into account Indonesia’s comparative advantages. The renewables market is competitive, with experienced manufacturers worldwide. Trying to create domestic competitors to global companies may prove hard, but there are comparative advantages across the supply chain to explore and benefit from; e.g. renewables could help create high-quality jobs in engineering and project finance, which can have positive effects in other parts of the energy and infrastructure sector

Acknowledgements

This report was prepared by the investment team in the Energy Supply and Investment Outlook (ESIO) Division of the Directorate of Sustainability, Technology and Outlooks (STO). The report was authored by Lucila Arboleya. Tim Gould (Head of ESIO) and Michael Waldron (Head of Investment) provided key guidance.

The report benefited greatly from contributions from other experts within the IEA: Kieran Clarke, Pablo Gonzalez, Peggy Hariwan, Randi Kristiansen and Nathaniel Lewis-George. The report also benefited from valuable inputs from Mechthild Wörsdörfer (Director of STO).

The work could not have been achieved without the support and co operation provided by the European Commission and European Union’s Horizon 2020 research and innovation programme funding under grant agreement No 952363, and the IEA Clean Energy Transitions Programme (CETP), particularly through the contribution of the United Kingdom, supported this analysis.

The report also benefited from valuable inputs, comments and feedback from experts at the MEMR of Indonesia as well as PLN.

In addition, many experts from outside of the IEA provided input, commented on the underlying analytical work and reviewed the report. Their comments and suggestions were of great value. They include:

Thomas Capral Henriksen (Danish Embassy, Indonesia)

Aang Darmawan (Organisation for Economic Co operation and Development [OECD])

Jeremy Faroi (OECD)

Florian Kitt (Asian Development Bank [ADB])

Lazeena Rahman (International Finance Corporation [IFC])

Cecilia Tam (OECD)

Fabby Tumiwa (Institute for Essential Services Reform [IESR])

Muhammad Ery Wijaya (Climate Policy Initiative [CPI])

The individuals and organisations that contributed to this study are not responsible for any opinions or judgements it contains. All errors and omissions are solely the responsibility of the IEA.

References

ATKarney (2019), Indonesia’s energy transition: A case for action, www.kearney.com/documents/20152/2789427/2019+-+Indonesia%27s+Energy+Transition+A+Case+for+Action.pdf/3eba51da-43d3-7756-ca31-b5b6dbcc5b5b?t=1558915028402.

CBI (Climate Bond Initiative) (2018), ASEAN state of the market 2018, www.climatebonds.net/2019/01/asean-green-finance-new-climate-bonds-reports-asean-green-finance-state-market-2018-asean.

CEP (Clean Energy Pipeline) (2020), database, London, https://cleanenergypipeline.com/.

CPI (Climate Policy Initiative) (2018), Energizing renewables in Indonesia: Optimizing public finance levers to drive private investment, https://climatepolicyinitiative.org/wp-content/uploads/2018/11/Energizing-Renewables-in-Indonesia-Optimizing-Public-Finance-Levers.pdf.

CPI (2015), Slowing the growth of coal power outside China: The role of Chinese finance, https://climatepolicyinitiative.org/publication/slowing-the-growth-of-coal-power-outside-china-the-role-of-chinese-finance/.

GGGI (Global Green Growth Institute) (2019), Product Analysis of Diverse De‑Risking Financial Instruments Available in Indonesia’s Market, http://greengrowth.bappenas.go.id/wp-content/uploads/2019/12/Product-Analysis-of-Diverse-de-Risking-Financial_Report-1.pdf.

IEA (2019), World Energy Outlook 2019, Paris, www.iea.org/topics/worldenergy-Outlook

IEA PV PS (International Energy Agency Photovoltaic Power Systems Programme) (2018), National survey report of PV power applications in Thailand 2018, https://iea-pvps.org/wp-content/uploads/2020/01/NSR_2019_Thailand_draft_Complete.pdf.

IESR (Institute for Essential Services Reform) (2019), Indonesia clean energy outlook, http://iesr.or.id/wp-content/uploads/2019/12/Indonesia-Clean-Energy-Outlook-2020-Report.pdf

IJGlobal (2020), Transaction data (web page), https://ijglobal.com/data/search-transactions (accessed May 2020).

IMF (International Monetary Fund) (2019a), World Economic Outlook, General government revenue (database), https://www.imf.org/external/pubs/ft/weo/2019/02/weodata/download.aspx (accessed March 2020).

IMF (2019b), Indonesia 2019 Article IV consultation, Indonesia, www.imf.org/en/Publications/CR/Issues/2019/07/30/Indonesia-2019-Article-IV-Consultation-Press-Release-Staff-Report-and-Statement-by-the-48535.

Lighting Global (2018), 2018 Global off-grid solar market trends report, www.lightingglobal.org/2018-global-off-grid-solar-market-trends-report/.

S&P Global Platts (2020), Global Olefins Outlook, S&P Global Platts, New York.

Tenenbaum, B., Greacen C. and Vaghela, D. (2018), Mini grids and the arrival of the main grid: Lessons from Cambodia, Sri Lanka, and Indonesia, Energy Sector Management Assistance Program, Washington, DC, https://openknowledge.worldbank.org/handle/10986/29018

Thomson Reuters Eikon (2020), database (accessed multiple times during March-May 2020), https://eikon.thomsonreuters.com/index.html

UNCTAD (United Nations Conference on Trade and Development) (2020), World Investment Report 2020, https://unctad.org/en/pages/PublicationWebflyer.aspx?publicationid=2769.

World Bank (2020), Public Participation in Infrastructure (PPI) Database, https://ppi.worldbank.org/en/ppi (accessed April 2020).

World Bank (2019), Global Financial Development Database (GFDD), https://datacatalog.worldbank.org/dataset/global-financial-development (accessed December 2019).

Reference 1

ATKarney (2019), Indonesia’s energy transition: A case for action, www.kearney.com/documents/20152/2789427/2019+-+Indonesia%27s+Energy+Transition+A+Case+for+Action.pdf/3eba51da-43d3-7756-ca31-b5b6dbcc5b5b?t=1558915028402.

Reference 2

CBI (Climate Bond Initiative) (2018), ASEAN state of the market 2018, www.climatebonds.net/2019/01/asean-green-finance-new-climate-bonds-reports-asean-green-finance-state-market-2018-asean.

Reference 3

CEP (Clean Energy Pipeline) (2020), database, London, https://cleanenergypipeline.com/.

Reference 4

CPI (Climate Policy Initiative) (2018), Energizing renewables in Indonesia: Optimizing public finance levers to drive private investment, https://climatepolicyinitiative.org/wp-content/uploads/2018/11/Energizing-Renewables-in-Indonesia-Optimizing-Public-Finance-Levers.pdf.

Reference 5

CPI (2015), Slowing the growth of coal power outside China: The role of Chinese finance, https://climatepolicyinitiative.org/publication/slowing-the-growth-of-coal-power-outside-china-the-role-of-chinese-finance/.

Reference 6

GGGI (Global Green Growth Institute) (2019), Product Analysis of Diverse De‑Risking Financial Instruments Available in Indonesia’s Market, http://greengrowth.bappenas.go.id/wp-content/uploads/2019/12/Product-Analysis-of-Diverse-de-Risking-Financial_Report-1.pdf.

Reference 7

IEA (2019), World Energy Outlook 2019, Paris, www.iea.org/topics/worldenergy-Outlook

Reference 8

IEA PV PS (International Energy Agency Photovoltaic Power Systems Programme) (2018), National survey report of PV power applications in Thailand 2018, https://iea-pvps.org/wp-content/uploads/2020/01/NSR_2019_Thailand_draft_Complete.pdf.

Reference 9

IESR (Institute for Essential Services Reform) (2019), Indonesia clean energy outlook, http://iesr.or.id/wp-content/uploads/2019/12/Indonesia-Clean-Energy-Outlook-2020-Report.pdf

Reference 10

IJGlobal (2020), Transaction data (web page), https://ijglobal.com/data/search-transactions (accessed May 2020).

Reference 11

IMF (International Monetary Fund) (2019a), World Economic Outlook, General government revenue (database), https://www.imf.org/external/pubs/ft/weo/2019/02/weodata/download.aspx (accessed March 2020).

Reference 12

IMF (2019b), Indonesia 2019 Article IV consultation, Indonesia, www.imf.org/en/Publications/CR/Issues/2019/07/30/Indonesia-2019-Article-IV-Consultation-Press-Release-Staff-Report-and-Statement-by-the-48535.

Reference 13

Lighting Global (2018), 2018 Global off-grid solar market trends report, www.lightingglobal.org/2018-global-off-grid-solar-market-trends-report/.

Reference 14

S&P Global Platts (2020), Global Olefins Outlook, S&P Global Platts, New York.

Reference 15

Tenenbaum, B., Greacen C. and Vaghela, D. (2018), Mini grids and the arrival of the main grid: Lessons from Cambodia, Sri Lanka, and Indonesia, Energy Sector Management Assistance Program, Washington, DC, https://openknowledge.worldbank.org/handle/10986/29018

Reference 16

Thomson Reuters Eikon (2020), database (accessed multiple times during March-May 2020), https://eikon.thomsonreuters.com/index.html

Reference 17

UNCTAD (United Nations Conference on Trade and Development) (2020), World Investment Report 2020, https://unctad.org/en/pages/PublicationWebflyer.aspx?publicationid=2769.

Reference 18

World Bank (2020), Public Participation in Infrastructure (PPI) Database, https://ppi.worldbank.org/en/ppi (accessed April 2020).

Reference 19

World Bank (2019), Global Financial Development Database (GFDD), https://datacatalog.worldbank.org/dataset/global-financial-development (accessed December 2019).

Cite report

IEA (2020), Attracting private investment to fund sustainable recoveries: The case of Indonesia's power sector, IEA, Paris https://www.iea.org/reports/attracting-private-investment-to-fund-sustainable-recoveries-the-case-of-indonesias-power-sector, Licence: CC BY 4.0