Cite commentary

IEA (2021), Managing the water-energy nexus is vital to India’s future, IEA, Paris https://www.iea.org/commentaries/managing-the-water-energy-nexus-is-vital-to-indias-future

The development of India’s power sector over the next two decades will take place against a backdrop of increasing water stress

With just 4% of the world’s water supply but 18% of its population, India counts as one of the world’s most water‐stressed countries. And India’s rapid economic ascent in recent years has only increased demand for both energy and water, putting these interconnected resources under increasing pressure and making the nexus between them central to the country’s energy security and transition goals.

Agriculture accounts for 80% of India’s water demand, but water is also critical to its energy sector, particularly for electricity generation. The development of India’s power sector over the next two decades will take place against a backdrop of increasing water stress, climate change and rising water demand from its agricultural, residential and industrial sectors. A continuation of current trends in water usage would put projected demand for water far ahead of the available supply and threaten the country’s energy output.

But India has an opportunity. Based on today’s policy settings, over 70% of electricity generation in 2040 is projected to come from power plants that have not yet been built. Technologies are already available that can meet this demand while reducing pressure on the country’s precious water resources.

India’s challenge to meet its growing demand for both electricity and water is why, as part of the India Energy Outlook 2021, the IEA, in partnership with the Council on Energy, Environment and Water (CEEW), analysed the vulnerability of India’s power sector to water availability under different development pathways.

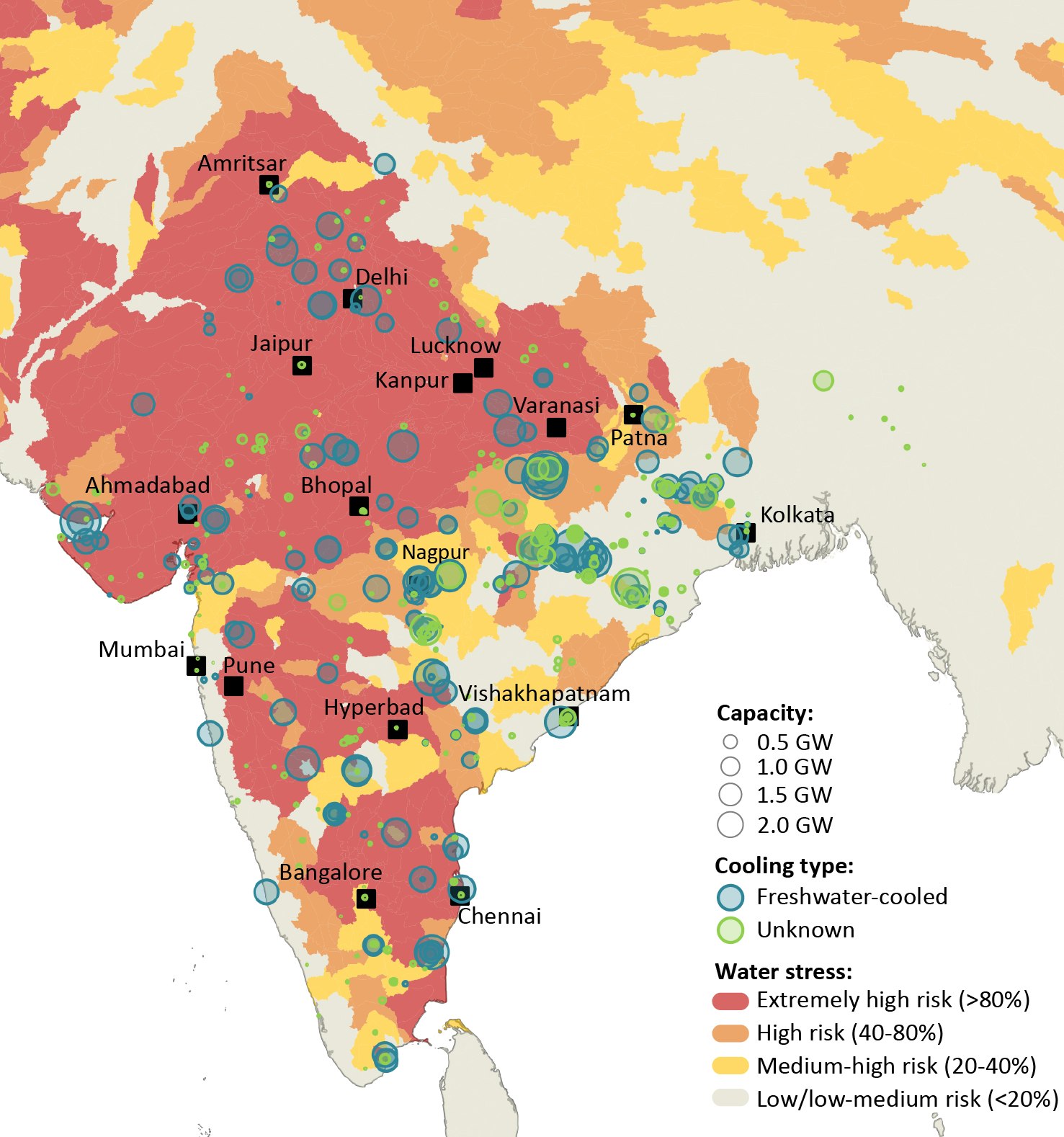

Water availability has already had an impact on India’s electricity supply: droughts and water shortages caused India to lose 14 terawatt hours (TWh) of thermal power generation in 2016. Our analysis, which mapped existing and under-construction capacity against water stress, found that over half of India’s existing coal plants are in areas experiencing high water stress.

Location of existing coal plants and baseline level of water stress in India

Open

{kind=link}

Recognising these risks, the Indian authorities have put in place measures to reduce the power sector’s water withdrawals. All existing and new power plants have been mandated to shift away from once-through freshwater cooling systems (which require high water withdrawals) and to cap their water consumption. Freshwater scarcity has also lead to a greater focus on the use of non-freshwater cooling and, to a lesser extent, on the use of dry cooling. As a result, the share of plants using freshwater cooling is set to drop – from 90% today to less than 65% in plants under construction.

A growing economy will intensify water management challenges in India’s power sector

A comparison of two potential pathways for India’s power sector development reveals the impact that different policy choices can have on the amount of water used by the power sector in the future.

- The Stated Policies Scenario (STEPS) provides a balanced assessment of the direction in which India’s energy system is heading, based on today’s policy settings (including the 450 gigawatt (GW) target for renewable capacity by 2030) and constraints.

- The Sustainable Development Scenario (SDS) goes even further in mapping out a sustainable vision for India’s energy sector. In this scenario, a surge in clean energy investment produces an early peak and rapid subsequent decline in emissions, consistent with a longer‐term drive to net zero, while accelerating progress towards a range of other sustainable development goals.

In both scenarios, electricity demand more than doubles before 2040, but the STEPS sees higher growth rates, reaching almost 5% per year in the outlook period.

India’s energy sector currently withdraws roughly 30 billion cubic metres of water (bcm) (the volume of water removed from a source) and consumes almost 6 bcm (the amount withdrawn but not returned to a source). Coal-fired power generation, responsible for close to 70% of electricity generation in India today, accounts for 80% of the energy sector’s water withdrawals.

The STEPS sees a significant decrease in water withdrawals by the power sector, from nearly 25 billion cubic metres in 2019 to less than 7 bcm in 2040, largely due to increases in the share of electricity coming from renewables with low water intensity and regulations on water use in thermal power plants. However, the long-lasting nature of coal infrastructure combined with the increased deployment of nuclear capacity after 2030 prevent water withdrawals from falling further and result in a slight rebound by the end of the outlook. Furthermore, water consumption grows by 45% to 2040, as a result of India’s policy requiring all thermal power plants to use tower cooling. While water withdrawals act as a first barrier to electricity production when water availability is limited, water consumption reduces the overall amount of water that is available to satisfy all users’ needs. This would be particularly problematic given the likelihood of rising water stress in many parts of India.

In the SDS, water withdrawals fall even further, to less than 3 bcm in 2040. This is mainly the result of a major reduction in coal‐fired power generation and a greater reliance on solar PV and wind, which have low water requirements. By 2040, these renewables’ combined share in generation grows to 60%, from less than 10% today. The decline in coal‐fired power also means that water consumption falls by around 40% by 2040, despite minor increases related to added capacity from modern forms of biomass, nuclear and concentrating solar power.

Strategies to ensure a more resilient power sector

Policy makers will need to contend with a more uncertain future in terms of water availability as climate change is expected to alter the frequency, intensity, seasonality and amount of rainfall. Climate change is also likely to change patterns of energy demand, with greater demand loads due to temperature extremes. The policy actions taken today will determine whether or not water will be a major constraining factor for the reliable and sustainable development of electricity supply. Two key strategic priorities emerge from our analysis.

Shifting to dry and non-freshwater cooling to improve the thermal fleet’s resiliency to water stress

Coal is the incumbent fuel for India’s power generation, and the existing plants (including those under construction) are set to remain a major element in India’s power mix even as renewables dominate new capacity additions. The average age of coal plants in India is around 15 years. Given that the lifespans of these plants normally run to about 50 years, most existing power plants could continue operating for over 30 years in the absence of a major additional policy push. To avoid additional strains on the system arising from water stress, it is essential that operators increase the share of dry or non‐freshwater cooling in new thermal plants, retrofit old ones and make better use of water-recycling.

India is already using non-freshwater cooling in some of its plants. Its third‑largest coal power plant, Mundra UMPP, was built in a drought prone area and uses desalinated seawater for cooling and other applications to avoid aggravating water stress.

The use of wastewater for cooling is another alternative. India’s government has mandated coal plants to use sewage water if they are located close to municipal treatment plants. However, just 5-8% of all coal plants in India have access to treated wastewater and are able to use this water source to completely or partially meet their cooling water needs. Even where wastewater is available, using it can be challenging. In 2016, the government of Maharashtra directed NTPC Solapur to switch to treated wastewater from Solapur town instead of freshwater from the Ujani reservoir. However, water quality concerns, the lack of an existing wastewater treatment facility and competition from farmers using the wastewater for irrigation led to the cancellation of the project. This underlines the importance of engaging different users and taking an integrated approach to water management.

Shifting to dry cooling, or air‐cooled condenser technology, eliminates the need for water. In India, the feasibility of dry-cooling installations, especially in areas with acute water stress, is under exploration. That said, there are important trade-offs to consider: dry cooling has a higher capital cost and reduces the power production by 7-8% as well as the efficiency of the plant. Thus, only 2% of capacity today uses the technology. Its upscaling would require supporting policies, such as dedicated government financing or an adjustment of power prices in water-stressed areas. Another option would be to spread the additional cost of dry cooling across all power plants in the country, favouring the deployment of this technology while causing only a marginal increase in retail power prices, given its low share in the generation mix.

Fully integrating water-energy linkages in India’s technology choices and policies

A preference for clean energy technologies can go hand-in-hand with strategies to alleviate water stress, but these linkages are not automatic and require careful design. Not all low-carbon technologies and fuels have low water requirements. Nuclear, bioenergy and concentrating solar power, all of which play a role in helping India meet its sustainability goals in the SDS, could, depending on the cooling technology deployed, be limited by water availability. Thus, energy planning efforts need to take into account competing water demands today and in the future when considering plant design and location – for example, by prioritising water-stressed areas with ample solar irradiation and wind for the development of new renewable capacity.

Managing water use patterns in other sectors can also support India’s power system development. Agriculture, in particular, can serve as an important power sector balancing tool. In Gujarat, agricultural pumping accounts for more than 20% of the state’s electricity demand, and shifting this load to the daytime would help align peak demand with solar output. This is possible because the state has a dedicated agricultural feeder system, which allows the interruption of agricultural supply without impacting other consumers. Shifting today’s predominantly night‐time scheduling to the day would reduce the start‐up needs from thermal generation sources by around 40%, and cut operating costs by about 10%.

Another promising option for power sector balancing is pumped-storage hydroelectricity, which involves pumping from a reservoir at a lower elevation to an upper storage facility during periods when there is excess power generation. When this trend reverses and there is demand for electricity, the upstream reservoir releases the water for generation purposes. In India, about 2.6 GW of pumped hydro storage are already operational, with another 3.1 GW under construction and proposals for further 8.9 GW on the drawing board. This technology can constitute a cost-effective way of providing storage capacity, with limited energy losses, and help to manage power supply both for peak demand hours and longer duration needs.

Our analysis in the new India Energy Outlook underlines that India’s energy choices have to take into account water availability and competing water demands. The same applies to its broader development priorities, given the strong synergies that exist between the UN Sustainable Development Goals 6 (water and sanitation for all) and 7 (energy for all). India’s energy future is tied to its water future. The existing and potential future water needs of the energy sector have to be an integral part of India’s energy strategy.

The IEA would like to thank the Council on Energy, Environment and Water (CEEW) for its collaboration on the energy-water analysis and acknowledge the contribution of Kangkanika Neog and Surabhi Singh to this work.

Managing the water-energy nexus is vital to India’s future

Molly Walton, Former Consultant and World Energy Outlook Analyst

Vaibhav Chaturvedi, Economist at the Council on Energy, Environment and Water Commentary —