Cite report

IEA (2020), Energy Efficiency 2020, IEA, Paris https://www.iea.org/reports/energy-efficiency-2020, Licence: CC BY 4.0

Report options

Buildings

A complex interplay of factors will determine how the Covid-19 crisis influences energy intensity in the buildings sector in the coming years.

In the short term, three trends are visible:

- a partial shift in energy demand from commercial to residential buildings, as social distancing measures and teleworking reduce people’s use of commercial buildings and increase energy using activities in the home; on some metrics, this will increase the overall energy intensity of the buildings sector

- an increase in the share of energy use from more energy-intensive sub-sectors, leading to higher energy intensity per unit of activity in commercial buildings

- restrictions in professional contractors’ access to residential properties, delaying technical efficiency upgrades; in some markets, however, increased rates of do-it-yourself renovations may be boosting technical efficiency.

Crisis-induced factors that could affect energy intensity in buildings

| Type of effect | Factor | Potential impact on energy intensity improvement |

|---|---|---|

| Activity and structural | More activity in residential buildings; less in commercial buildings. | |

| A greater share of services sector energy use comes from more energy-intensive services sub-sectors. | ||

| Commercial building ventilation rates are increased for health reasons. | ||

| Technical efficiency | Economic recession and job losses lead to lost income for owners (partly due to lower rental payments) and tenants, and lower rates of building renovation and stock turnover. | |

| Continuing low fuel prices prolong the payback period for building energy efficiency upgrades. | ||

| Continued health risks prevent professional energy efficiency contractors from accessing residential buildings, delaying building upgrades. | ||

| Energy services companies lose revenues and possibly default, starving the market of providers. | ||

| Government stimulus spending targets building retrofits and efficient new buildings. | ||

| Higher residential energy bills due to increased time at home encourages homeowners to invest in efficient building upgrades. | ||

| Commercial building owners take advantage of the absence of tenants and building users to upgrade buildings without inconveniencing tenants. | ||

| More time spent at home encourages do-it-yourself renovations as people invest in increasing their comfort. |

In the longer term, the duration of the health and economic crisis will have a significant impact on energy intensity in buildings. A lasting health crisis could continue to limit commercial building use, prolonging energy intensity trends seen in 2020. As more people return to work during the pandemic, demands for higher ventilation rates in commercial buildings for health reasons could lead to spikes in energy intensity. If the economic recession deepens, households and businesses may reduce spending on building upgrades, which will slow technical efficiency improvements. Current forecasts suggest the pandemic has dampened growth expectations for the buildings and construction sector.

However, the buildings sector will soon benefit from increased government investment, as buildings have been the primary target for energy efficiency stimulus spending announcements to date. In some regions, the scale of this investment could be large enough to significantly boost technical efficiency.

Activity and structural impacts

Energy use grows in residential buildings and falls in commercial buildings

On average, people across major economies reduced visits to workplaces by over 60% in April, with visits still down 20% to 30% from June to September, as teleworking appeared to become more normalised. Time spent at home had increased by nearly 30% at the height of the lockdowns and was still 5% to 10% higher between June and October. The increase in time spent at home is being used to conduct activities that consume energy, leading to significant and complex shifts in energy demand.

In some parts of the United States, average residential electricity use on weekdays was up by 20% to 30% in late March and early April, particularly for cooling homes in warmer climates. In India, electricity demand also rose as residential cooling loads increased, while in Europe heating energy use contributed to 40% higher electricity consumption year-on-year in March and early April.

In contrast to the residential sector, energy consumption in commercial buildings has declined. Electricity demand in the commercial and service sectors in the People’s Republic of China (“China”) decreased by 3% during the first two months of the year as the Covid-19 pandemic began but has since rebounded. In the United States, commercial electricity demand was 8% below last year’s levels between April and September, as shops were closed or operated under limited hours and offices remained partially occupied or empty.

However, even when commercial buildings such as offices remain unoccupied, most continue to consume energy, for maintenance of heating, ventilation and air conditioning (HVAC) systems, or to power computing servers, for example. Working from home has net benefits for energy use and emissions, but these come mainly from reduced commuting.

While the net effects of the shift from commercial to residential buildings will vary by country and by fuel, minor decreases in buildings sector electricity use as a whole have been observed in some countries. In Australia, electricity demand was about 2% lower after residential demand growth nearly entirely offset falls in commercial demand. In Europe, after a 13% decline below the five-year average in April, cross-sector electricity demand partly recovered during the summer months. As coronavirus cases started to increase again in autumn, however, power demand slightly dropped, for example in Italy and Belgium in October.

At least on some metrics (such as energy use in buildings per unit of economic output), the shift from commercial to residential buildings will increase the energy intensity of the buildings sector.

Working from home can save energy and reduce emissions. But, how much?

A day of working from home could increase daily household energy consumption by 7% to 23% compared with a day working at the office. The magnitude of the change depends on regional differences in the average size of homes, heating or cooling needs, and the efficiency of computers and other IT equipment and appliances used at home. In most parts of the world, the extra demand in winter is larger than in summer, due to space heating, while the energy mix in winter also typically shifts more towards fossil fuels.

Change in global final energy consumption by fuel and CO2 emissions in the “home-working” scenario

OpenA day working from home would, on average, reduce energy consumption and CO2 emissions by cutting time and fuel spent commuting by car. For workers who normally make only short commutes by car, however, or mainly take public transport, working from home could lead to a small net increase in energy demand and emissions from higher residential energy use, depending on the residential fuel mix.

Globally, nearly one job in five could be done from home. If all of these people were to telework for just one day a week, around 1% of global oil consumption for road passenger transport would be saved each year. Accounting for the corresponding increase in household energy use, global CO2 emissions could fall by 24 million tonnes annually. Reduced use of computers and other IT equipment at work leads to additional, though minor, reductions in electricity consumption that are not reflected in this estimate.

Overall, this is a notable decline but small in the context of the emissions reductions that would be necessary to put the world on a path towards meeting key long-term sustainable energy and climate goals. Over time, a more significant shift to home working could further reduce demand for office space and energy for commercial buildings, leading to a greater overall reduction in energy consumption. However, energy demand reductions from office buildings and avoided commutes could be partly cancelled out if habitual home working leads workers to consume more energy by moving to larger homes outside cities that require more heating and cooling energy, and opting for more energy-intensive transport.

In addition to enabling teleworking, the use of video conferencing could also reduce jet fuel demand as well as emissions by substituting long-haul business trips. Based on current aircraft efficiencies, halving business trips to destinations further than six hours flight away would be likely to reduce the annual number of flights by less than 1% but would save around 50 million tonnes of CO2.

A higher share of energy use from energy-intensive essential services

Reduction in energy demand under stay-at-home orders and average energy intensity by building type, in two United States regions

OpenWhile the pandemic has generally reduced energy demand in commercial buildings, decreases have varied widely across business sizes, customer segments and regions. Smart meter data from two regions in the United States show that larger businesses have been less affected than smaller businesses, with essential businesses and services such as supermarkets and hospitals being the least affected.

While many commercial buildings have resumed a more “business as usual” level of service since the height of lockdowns, the crisis appears to have stimulated bigger falls in energy use in commercial buildings that are less energy intensive (such as services, religious worship or education buildings). Commercial buildings that are more energy intensive – such as restaurants, supermarkets and hospitals – have experienced less severe declines in demand. While global data are limited, available data suggest that energy intensity in commercial buildings may have increased on an energy per unit of service basis.

”Urban flight” has affected energy intensity less than longer-term urbanisation

Reports of “urban flight” – migration of city dwellers to less densely populated areas – have emerged since the onset of the Covid-19 crisis, leading to suggestions that energy intensity in buildings could increase. As buildings in less densely areas tends to be larger, they often use more energy, particularly for heating or cooling.

A survey in the United States suggested some temporary migrations have been observed but was inconclusive on cause, which was also the case in analysis of real estate and moving companies’ data. In Europe, there were also some temporary moves from cities to less dense areas in 2020 but no evidence of permanent migrations.

Ultimately even if reports of people moving from primary to secondary cities in developed economies becomes a trend, and result in higher energy use per occupant, the global pattern of increasing urbanisation is unlikely to reverse, which will have a bigger impact on energy demand and intensity than Covid-19 driven migrations.

How could Covid-19 affect the use of heating, cooling and ventilation systems in buildings?

Concerns over the spread of Covid-19 via airborne particles, and a possible correlation between air quality and health impacts of the virus, are drawing increasing attention to ventilation systems in buildings.

Guidance by ASHRAE (formerly the American Society of Heating, Refrigerating and Air-Conditioning Engineers) outlines best practice approaches to minimising the risk of transmission of airborne infectious disease. The recommendations include inspection and maintenance of heating, ventilation and air-conditioning (HVAC) systems, filtration using MERV 13 filters or better for filtration, and higher rates of outdoor air exchange. The Federation of European Heating Ventilation and Air Conditioning Associations (REHVA) recommends supplying as much air to buildings as possible by opening windows and increasing the use of outdoor air, while avoiding the use of energy-savings settings on demand-controlled ventilation systems.

Under normal conditions, 30% of energy delivered to buildings is dissipated in the air that leaves buildings through ventilation and exfiltration, so increasing ventilation rates will also increase the energy used by buildings’ heating and cooling systems. It is therefore important for HVAC systems to operate as efficiently as possible. Installing, recommissioning and upgrading HVAC systems will enhance building performance as well as protecting health.

Some HVAC engineers already foresee that increased demand for ventilation (such as requiring the purging of an entire building’s air once every 24 hours) will have significant costs for energy efficiency. Reducing these costs, while meeting the health imperatives for increased ventilation rates, will require innovative technologies such as smart HVAC control systems, more advanced filtration systems and novel dehumidification technologies for energy recovery.

Technical efficiency impacts

Predicting the impact of the Covid-19 crisis on progress in the technical efficiency of buildings is difficult due to poor data availability. However, lockdowns are likely to have delayed technical efficiency improvements in the buildings sector in the short term, despite some countries reporting increased rates of home renovation.

Longer term, a deepening recession could dampen consumer and business confidence, discouraging efficiency investments in buildings. However, governments have been quick to recognise that energy efficiency upgrades for buildings can deliver economic growth and employment. In countries that are targeting stimulus spending at the buildings sector, the technical energy efficiency of the building stock could improve significantly in the next few years.

Lockdowns prevented access to residential buildings, delaying efficiency improvements

In residential buildings, physical distancing has limited the installation of equipment and systems requiring professional installation. For energy-efficient renovations, reports suggest limited access to properties in the first half of 2020 is likely to have delayed the installation of equipment such as insulation, glazed windows, and efficient heating and cooling systems, such as heat pumps.

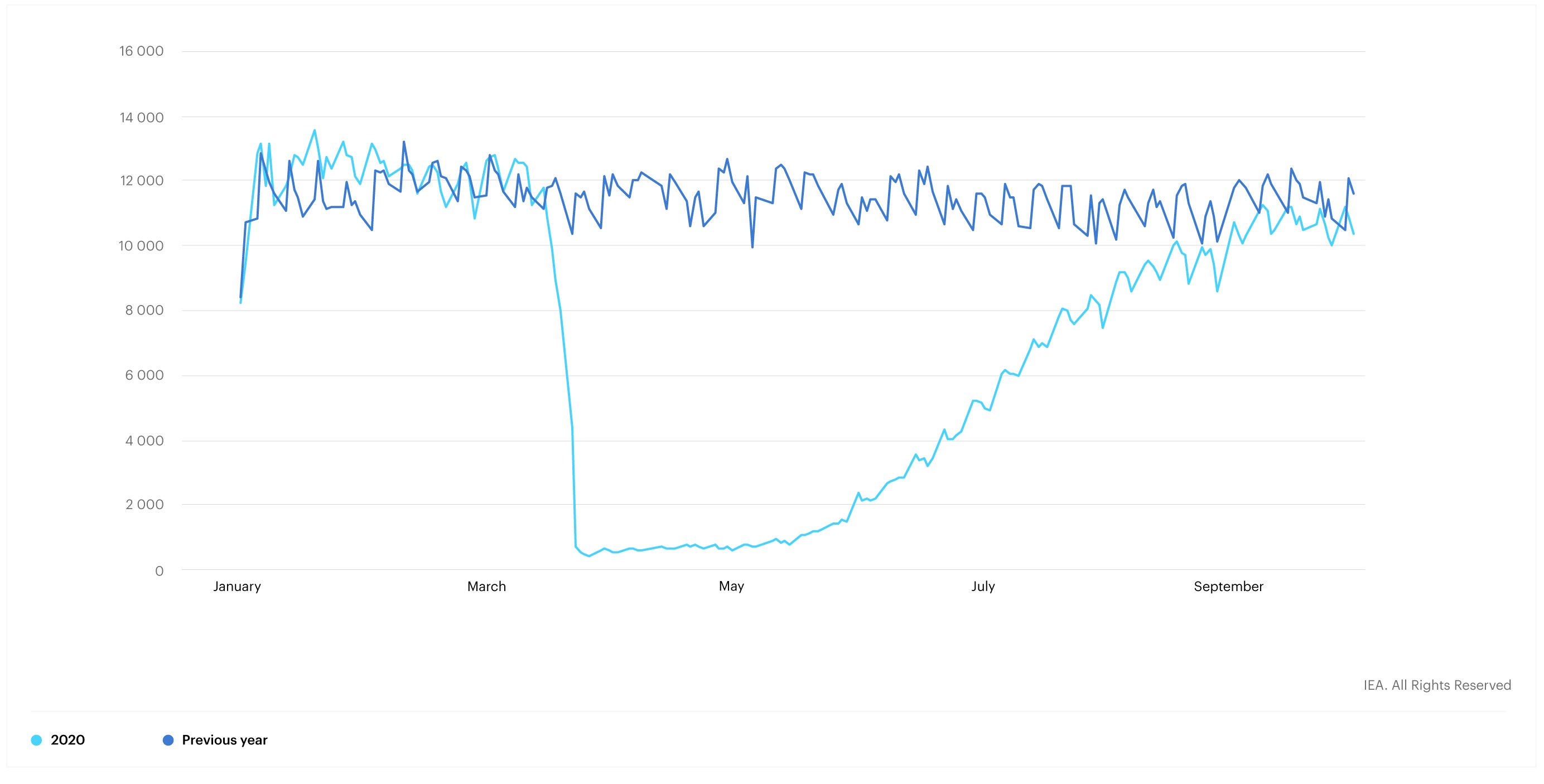

The impact of physical distancing on professional installers’ access to properties is reflected in smart meter installations in the United Kingdom. Installations fell from around 12 000 per day to less than 1 000 per day at the height of the lockdowns. A similar trend was reported in India, where Energy Efficiency Services Limited reported a drop in installations to around 2 000 per day, from 10 000 per day under normal conditions.1

Daily smart electricity meter installations, United Kingdom

Open

{kind=link}

As with smart meter installations, which had returned to 2019 levels by September in the United Kingdom and elsewhere, other professional equipment installers also reported increased access to properties by the third quarter of 2020. Energy efficiency professionals have also adapted by offering virtual consultations. However, new lockdowns, in response to the second wave of the virus that has affected several parts of the world, could lead to more delays in efficient equipment installations in residential buildings.

A spike in renovations may increase residential buildings’ technical efficiency in some wealthy countries

Data from some countries suggest that the increased time spent at home has encouraged homeowners to undertake work on residential properties, including energy-efficient renovations. With professional tradespeople denied access to some buildings for health reasons, homeowners appear to be adapting by turning to do-it-yourself (DIY) renovations, or commissioning tradespeople to work on upgrades where health concerns are lower (such as installing underfloor insulation).

For example, interviews with energy efficiency product and service providers in Australia2 suggested that demand had increased for lower-cost energy efficiency measures, with increases of 15% in LED lighting sales and 145% in online sales of DIY draught-proofing. One company reported a 30% increase in sales of DIY insulation products, and in March an insulation installer noted a 270% month-on-month increase in customer inquiries. However, some interviewed noted significant declines in more expensive residential energy efficiency products and services.

The United States has seen a similar increase in home improvement activities in 2020. DIY builders are thought to have contributed to a 50% increase in wholesale lumber prices, while a Bank of America survey of over 1 000 people on consumer attitudes during the Covid-19 crisis found that over 70% of households have intentions to make home improvements in 2020, with more planned for next year. Major US home improvement chains Home Depot and Lowe’s, which combined operate close to 4 300 stores, recorded over USD 65.4 billion in net sales in the three months to the end of July 2020, a 26% increase on the same period last year.

In addition, wealthy households may have redirected some of the increase in disposable income – gained by not spending in other sectors of the economy, like travel – to energy efficiency improvements, to benefit from the gains in comfort such investments can deliver. For example, anecdotal evidence from the United States suggests that sales of higher‑efficiency residential HVAC systems have increased since the Covid-19 crisis began. Some consumers are investing in high-efficiency air conditioners with a seasonal energy efficiency rating of 16 to 20; normal purchasing trends tended towards systems with a rating of 13.

Weaker outlooks for global construction hint at lower rates of efficient building construction and upgrades

Covid-19 is expected to severely curtail global construction industry investment. The latest estimates anticipate annual year-on-year growth of only 1.2% from 2019-2020, down from 3.1% at start of 2020. Dramatic contractions took place in some major regional markets: 4.4% in Germany and 7% in Canada from 2019 levels, as well as 2.2% in India and 7.7% in Malaysia. Despite the slowdown, overall construction in China is expected to increase by 1.9% from 2019. Given the size of China’s market, this helps to keep the global estimate on a slight upward trend.

The building construction industry is expected to follow similar trends to those of overall construction (which includes non-building construction such as bridges and roads). Some projections suggest a recovery that sees pent-up demand pushing annual growth rates above pre-pandemic levels, but these remain highly uncertain. US data suggest that newly completed privately owned houses that have sold or are for sale have increased by 8% in August 2020 compared to the previous year.

The “green” building materials market is expected to achieve an annual growth rate of 8.6% by 2027, down from 11.7% in 2019. Demand for green building is projected to continue to grow by 11.6% in China and 13% in Latin America by 2027. The energy efficiency glass market is expected to reduce in size by around 6% to 2027 compared with pre-pandemic growth rates. Despite falls in residential sales in the first half of 2020, demand for thermal insulation is estimated to maintain its growth rate at around 4% per year, with demand for these products in high-income northern climates boosted by continued government support. This trend reflects anticipated demand for residential cooling and a shift to home working.

Policy responses to the crisis will strongly influence whether these forecasts for the buildings sector – and the technical efficiency of buildings – prove to be accurate. Analysis of buildings sector policies to date gives some reason for optimism, particularly in Europe, where large-scale building renovation policies have been announced. However, in other regions, policies to support high levels of building renovation are yet to reach the same scale.

Covid-19 impact on efficient building products: Insulation sales dip, but bright spots remain

The effect of the crisis on the technical efficiency of the building stock can be seen in the balance sheets of major energy efficiency building equipment producers, which reflect the impact of lockdowns, physical distancing and a weak economy.

For example, insulation producers globally reported falls in sales of 5-20% in the first half of 2020, with sales particularly low in the second quarter, during the height of lockdowns.

Regional differences suggest demand-side factors have inhibited insulation sales, with sales higher in regions with smaller health and economic impacts from the virus. For example, in the second quarter of 2020 some companies reported stable sales in Nordic countries, Canada and Australasia, where incomes are high, the impacts of Covid-19 have been less severe and insulation is important for thermal comfort.

In Australia, DIY renovations have reportedly spurred an increase in sales for residential insulation products, with some companies reporting year-on-year growth of 20% to 40% in the first half of 2020.3

References

Information provided to the IEA from Energy Efficiency Services Limited.

Unpublished analysis by the Energy Efficiency Council of Australia, shared with the IEA.

Australian information is from unpublished analysis by the Energy Efficiency Council of Australia, shared with the IEA. For Australasia, see Kingspan 2020 Interim Results.

Reference 1

Information provided to the IEA from Energy Efficiency Services Limited.

Reference 2

Unpublished analysis by the Energy Efficiency Council of Australia, shared with the IEA.

Reference 3

Australian information is from unpublished analysis by the Energy Efficiency Council of Australia, shared with the IEA. For Australasia, see Kingspan 2020 Interim Results.