Cite report

IEA (2021), Driving Down Methane Leaks from the Oil and Gas Industry, IEA, Paris https://www.iea.org/reports/driving-down-methane-leaks-from-the-oil-and-gas-industry, Licence: CC BY 4.0

Report options

Regulatory Roadmap

The following steps will help you choose a regulatory approach and implement a set of effective methane policies that match your particular situation. Across these steps, the process of implementing a new regulation unfolds in three distinct phases – understanding your setting (Steps 1-3), designing and developing your regulation (Steps 4-8), and implementation (Steps 9-10). If you are new to regulating methane, you might consider starting at Step 1 and working through the list. If your jurisdiction has already done work in this area, you could enter the steps further on, or skip steps based on work you have already done. Although presented sequentially here, these steps may be carried out in a different order, may take place concurrently, or may even be repeated once new data on emissions or new technologies become available. For example, depending on your institution’s capabilities, you may carry out step 3, “build regulatory capacity”, throughout the process, only at the implementation and enforcement stage, or not at all.

A ten-step roadmap for policy makers

Step 1: Understand the legal and political context

Step 2: Characterise the nature of your industry

Step 3: Develop an emissions profile

Step 4: Build regulatory capacity

Step 5: Engage stakeholders

Step 6: Define regulatory objectives

Step 7: Select the appropriate policy design

Step 8: Draft the policy

Step 9: Enable and enforce compliance

Step 10: Periodically review and refine your policy

Step 1: Understand the legal and political context

The first phase of the process takes place before any formal development of a regulatory proposal. It consists of an information-gathering exercise designed to help you gather information that will inform your selection of a regulatory approach. This includes exploring how your institutional circumstances, existing regulatory framework, market context and current emissions may impact your decision-making. This phase begins here with Step 1 and continues through Step 2, where you will characterise the nature of your local industry, and Step 3, where you will develop a detailed emissions profile.

What characteristics of the institutions in your jurisdiction should be taken into account when crafting a regulatory regime?

In this step, you will consider how regulating methane emissions from the oil and gas sector might fit your political and regulatory context. Understanding where legal authority and political power for action on methane sit can help activate the most promising institutions within your government. Reviewing existing policies can suggest where to amplify methane abatement efforts, or what to change to remove disincentives for action. By considering the following questions, you can identify who should be involved and design policies that fit your agency.

Agencies with relevant regulatory authority

From the outset, it is important to know which institutional actors have regulatory authority. The answer may depend on the ownership of the resource, the location of the resource, and the nature of the regulation (energy, environmental, economic). Many jurisdictions understandably focus on natural resource and environmental authorities, but other types of regulators can be engaged in this important work. Moreover, thinking through the approaches different groupings of regulators can take can help to settle potential jurisdictional disputes between ministries and suggest a more productive partnership going forward.

What is the agency’s area of jurisdiction, and how can that be leveraged to abate methane?

Considering how your agency’s jurisdiction might be deployed to tackle methane from oil and gas enables you to build on existing authority and think creatively about new applications of your regulatory tools and programmes.

A given agency may have jurisdiction over resource development, air quality, worker safety or economic expertise. The policy focus of the particular government body affects what strategies are available.

Actors with jurisdiction over natural resource extraction will likely pursue methane abatement strategies from a waste prevention (or product conservation) perspective. For instance, you might focus on the revenue owed to the government for production of the resource, requiring the installation of meters at production facilities and assessing royalties for methane that is vented and flared rather than captured and sent to market. Brazil has imposed this type of regime, as has the United States when production occurs on public lands.##1## Natural resources or energy agencies may also impose operational requirements like leak detection regimes or routine maintenance and replacement of leaking equipment, again with the primary aim of preventing or reducing waste of a strategic resource.

Environmental actors, by contrast, will focus on methane abatement as an air quality or climate mitigation strategy. In some instances, these agencies may regulate volatile organic compounds and benzene for their contribution to air pollution, and capture methane indirectly through these requirements. The US Environmental Protection Agency first regulated methane emissions from the oil and gas sector in this way, as have several US state environmental agencies, such as Wyoming and Pennsylvania, as well as Alberta, Canada. Rules targeting methane abatement as an air quality strategy may focus on larger sources of volatile organic compounds (including methane) located close to population centres, based on public health concerns. Environmental rules may also target methane as a greenhouse gas, taxing emissions based on a Social Cost of Carbon, or tying requirements to commitments previously made under the Paris Agreement, or to be made in the nationally determined contributions (NDCs) due in November 2020. For instance, national methane rules issued by the Environment and Climate Change Department in Canada and the Safety, Energy and Environmental Agency in Mexico were drafted with international climate goals in mind.

Labour agencies may have jurisdiction over methane-emitting oil and gas activities, where emissions create unsafe work environments. These agencies, for instance the Department of Treasury and Finance in South Australia and SafeWork in New South Wales, might focus on mitigating the threat of fire or explosion from methane leaks. Traditionally, safety agencies might have recommended release of methane gas to the atmosphere, for instance before welding a pipeline or mining coal, or to release vapours from an oil tank to prevent explosion. However, as understanding of the environmental risks posed by methane emissions grows, agencies are realising they can act to keep workers safe while also minimising the release of methane emissions. Labour agencies may focus on inspections, monitoring, maintenance of equipment, worker training and community education.

Finally, economic regulators can create financial incentives for methane abatement. In jurisdictions that approve natural gas rates set by natural gas producers or transporters, rate-making rules can be structured to incentivise the prevention of methane emissions. For instance, by capping the costs of “lost and unaccounted-for gas” that a company can pass on to customers, the US states of Texas and Pennsylvania hope to induce industry to plug pipeline leaks. Or, an economic regulator might take Quebec’s example and allow gas distribution companies to charge a premium for gas produced using leading management practices to control methane leakage.##2## Similarly, legislatures may invest in research and development, or award grant funds to innovative abatement practices. The US Department of Energy in the fall of 2020 requested information on new technologies to promote methane abatement. Finally, government actors may have economic development goals to meet, from universal electrification to advanced manufacturing. In these cases, requiring or encouraging oil producers to capture and sell co‑produced natural gas could reduce methane emissions while providing fuel for power plants or feedstock for chemical production. Nigeria’s 2017 Natural Gas Policy reflects some of these interests.

Regulatory scope

|

Question |

Relevance |

Examples |

|---|---|---|

|

How can your agency act to reduce methane emissions from oil and gas? |

Agencies with authority over mineral resources might use rents, royalties or concession payments to discourage waste of the resource. |

The National Oil, Natural Gas and Biofuels Agency in Brazil charges royalties for all flared gas; the federal Bureau of Land Management in the United States charges royalties for excessive flaring and waste of natural gas. |

|

Environmental agencies might use existing air pollution programmes or climate ambitions to tackle methane pollution. |

Canada’s (Environment and Climate Change Department) methane pollution abatement standards and Mexico’s methane regulations support each country’s international climate commitments. |

|

|

Labour or safety agencies might consider safety practices that also reduce methane venting. |

The Department of Treasury and Finance in South Australia and SafeWork in New South Wales have safety standards for gas fitting and coal mining; such standards can promote safety while preventing methane release. |

|

|

Economic regulators might consider disallowing “lost gas” costs to be passed on to customers, or creating business opportunities for capturing and marketing associated gas. |

Texas and Pennsylvania utility commissioners capped “lost gas” costs to customers at specified percentages of metered throughput. Quebec utility regulators authorised natural gas companies to charge premiums for “responsibly produced” gas (including robust methane abatement programmes). Nigeria’s 2017 Natural Gas Policy sought to catalyse a midstream market for natural gas. |

Who owns the oil and natural gas, and controls exploitation rights for these resources?

Generally speaking, regulation of a natural resource – and the pollution that its exploitation may cause – follows ownership. In countries where the national government owns and manages the mineral estate, including for instance Mexico, Indonesia, Kazakhstan, and Nigeria, the national government also decides who can produce oil or natural gas, and on what terms.

In other countries, such as Argentina and Canada, mineral resources may be owned and managed by the subnational governments where they are located. Those subnational governments also hold primary authority over the operation of oil and natural gas facilities, including activities that might cause or inhibit the release of methane to the atmosphere. Where provincial actors are the lead regulators, national agencies are more likely to play educational and supportive roles – in Canada, for instance, the national Natural Resources Ministry directs non‑regulatory research and development of non‑binding methane abatement equipment and practices, which provinces may adopt in their onshore oil and natural gas standards. The same ministry jointly manages and regulates offshore resources with the Maritime Provinces, underscoring that location of the target resource may shift the locus of regulation. (Meanwhile, as discussed in the next section, Canada’s national environment ministry exercises plenary authority to regulate air pollution from oil and gas operations.)

A handful of countries enable private ownership of minerals. For instance, in the United States, the federal government, state and local governments, or private parties may own oil and natural gas resources. The owner of the mineral estate sets the terms for royalty payment, including whether to charge royalties for gas that a producer leaks, vents or flares. Therefore, if a private entity owns the mineral estate, royalties are negotiated through private contract.

Natural resource rights

|

Question |

Relevance |

Examples |

|---|---|---|

|

Who owns the oil and natural gas, and controls exploitation rights for these resources? |

If the national government owns the resource, it likely can control activities that produce methane emissions and prevent or discourage venting and waste of the resource. |

In Mexico, the nation owns the mineral estate, and a collection of national agencies regulate this sector. Indonesia’s laws makes clear that oil and gas are national assets which are controlled by the state; the same document directs the government to establish a national regulatory entity. |

|

If subnational governments own the resource, they will enjoy more authority over exploitation (and methane). However, the national government may still exercise other authorities, e.g. over air pollution. |

In Argentina and Canada, subnational governments own the resources located within their borders, and take the lead on regulating exploitation including limits on venting and flaring of methane. |

|

|

If private actors own the resource, private contracts determine royalty terms, including whether royalties should be paid for vented or wasted gas. |

In the United States, many oil and gas deposits are privately owned. There, private leases can but do not have to include terms to prevent or limit methane venting. |

How is associated gas treated and permitted?

In some jurisdictions, gas that is co‑produced (or “associated”) with oil or coal is considered a waste product rather than a resource; governments may have to clarify that they own the associated gas and establish a separate permitting regime. For instance, Nigeria’s Petroleum Act treats associated gas as separate from a petroleum lease and authorises the government to take that gas “free of cost at the flare or at an agreed cost and without payment of royalty.” This enabled the Nigerian Ministry of Petroleum Resources to establish a permitting system to grant associated gas production to someone other than the oil leaseholder. Similarly, Kazakhstan made clear in 2010 that coal mines must reduce associated methane emissions, and authorised the leaseholder to use the methane on site or to separately secure the right to produce the gas for delivery to market. By contrast, in other countries the associated gas is considered part of the leasehold. As a result, the government may not separately lease the associated gas; on the other hand, the oil producer may be liable for royalties on unnecessary flaring and venting.

Associated gas regulation

|

Question |

Relevance |

Examples |

|---|---|---|

|

How is associated gas treated and permitted? |

If associated gas has been treated as a waste product, the government may need to clarify that it is a resource and enable legal ownership before regulating it. |

Nigeria’s Petroleum Act makes clear that the national government owns associated gas and may take it without paying royalties. Nigeria used this authority to grant associated gas production rights to companies focused on the recovery and sale of gas. |

|

If associated gas is not considered part of an oil or coal concession/leasehold, agencies can contract with third parties to exploit it. |

Kazakhstan requires coal companies to separately acquire the rights to capture and sell associated gas. |

|

|

If associated gas is considered part of the concession or leasehold, the governing documents can require companies to use the gas on site or to pay royalties on it. |

In the United States and Brazil, oil companies must pay royalties on some flared and vented associated gas. (In the United States, this is only for oil and gas owned by the federal government.) |

Who regulates air pollution?

Authority over air pollution may not be the same as for natural resources. Air pollution may be seen as exclusively either a national or local issue, or as a shared responsibility. Environmental authority may also differ depending on the pollutant, and whether methane is defined as a pollutant at all under the law.

These distinctions determine which government body has authority and how it might regulate methane emissions. For instance, while the Canadian constitution grants provinces and territories primary authority over the exploitation of natural gas and other resources, the national government enjoys plenary authority over environmental matters. Therefore, while Canadian provincial energy agencies issue rules for minimising the venting and flaring of methane as operational standards for natural resource exploitation, the national Ministry of the Environment has implemented air pollution rules targeting methane emissions from oil and gas facilities. The provinces then have to implement these directly or through rules that the national Minister of the Environment approves as “equivalent”, as set out in the Canadian Environmental Protection Act. Under this authority, Canada has determined that the methane regimes in Alberta, British Columbia and Saskatchewan##3## are equivalent to the national methane rule.

Air pollution regulation

|

Question |

Relevance |

Examples |

|---|---|---|

|

Who regulates air pollution? |

Sometimes, the governmental agency that regulates exploitation of resources sits at the same level of government as the agency that regulates associated environmental concerns. |

In many countries, the national government not only controls these resources but regulates air pollution from these activities. This includes Indonesia, Mexico, Nigeria and Norway. |

|

One level of government, or a particular agency, may regulate access to and exploitation of resources. A different level of government or agency may regulate environmental aspects of these activities. |

In Canada, despite the provinces taking the lead role in permitting the exploitation of oil and natural gas, the national government has a shared authority with the provinces over environmental matters. Therefore, while provinces such as Alberta and British Columbia have established flaring and venting rules in their capacity as resource regulators, Canada has issued methane pollution abatement standards for the whole country, which may be displaced by provincial regulations determined to be “equivalent”. |

Do worker or community safety institutions have authorities that might be implicated in methane abatement?

Depending on the country, national or subnational authorities may also focus on worker safety. In Mexico, the national agency ASEA issued guidelines in 2016 for the implementation of management systems for industrial and operational security and environmental protection in the hydrocarbons sector. These guidelines included a requirement to conduct risk analyses of operations. Similarly, the Minister of Petroleum Resources in Nigeria has issued safety regulations. Meanwhile, in Canada and Australia, subnational governments have issued work health and safety rules related to methane emissions. In most of these examples (except for Australia), the safety rules were a subset of operational/exploitation rules. In the United States, a stand-alone safety agency in the national Department of Labour, the Occupational Safety and Health Administration, sets safety standards for industries including those along the oil and natural gas value chain.

Safety regulation

|

Question |

Relevance |

Examples |

|---|---|---|

|

What other authorities might be implicated in methane abatement? |

Worker or community safety authorities could be engaged in the enterprise of reducing methane venting to the atmosphere. Currently, many safety rules do not prevent methane venting, and could be improved to achieve this goal while maintaining safety. |

Mexico’s and Nigeria’s oil and gas regulators have issued national safety standards for oil and gas activities. In Canada and Australia, subnational agencies take the lead on safety issues. The United States has a federal safety administration that issues rules applicable to different industries, including oil and gas. |

Are there staging considerations for when your agency should act in relation to other government actors?

Mapping the political landscape beyond your agency can be incredibly useful for determining the right time to act. If leadership in your legislature or the head of state wants to reduce methane emissions, you can seek new authority through statutes or executive decrees for a more optimal approach to methane abatement. If not, you may proceed using the powers that you already have. If national and subnational governments share jurisdiction, it may make sense to let the subnational actors with extensive oil and gas experience act first. The most effective solutions forged on that smaller stage can then be replicated or scaled up to the national level. Where multiple ministries share oversight of oil and natural gas activities – perhaps those regulating energy, environmental, safety and economic issues – they should attempt to co‑ordinate to avoid overlap and inconsistency. For instance, it may be useful for agencies that work more closely and co‑operatively with industry to jointly identify best practices and begin to work those into contracts and concession agreements, for later adoption by other agencies through regulation.

Pre-existing policies

The next grouping of regulatory characteristics to consider in Step 1 concern existing governmental capacities and policies that might be leveraged to achieve methane abatement. Building a regulatory regime that plays to your institutional strengths will help to ensure success. Meanwhile, once you identify pre‑existing authorities that directly target methane or indirectly affect decisions that drive methane emissions, you can step up their use, adapt their application, amend them or remove them for optimal methane outcomes.

What tactics or strategies does your agency typically deploy to achieve its policy missions?

Once you have established that your agency or ministry has the jurisdictional authority to tackle some aspect of oil and gas methane emissions, it is important to think about the tactics it most often employs to achieve its policy goals. If yours is a regulatory agency with experience enforcing standards, then it could make sense to proceed with regulation. If your agency tends to work collaboratively with large players in the oil and natural gas industry, perhaps by facilitating joint ventures and other contracts, then you might begin by adapting contract provisions on a going-forward basis, to incentivise or require methane abatement. If your agency is a research institution, you could partner with universities, industry and international organisations to test new methane abatement equipment or practices. Finally, if your entity is a data collection body, you might be trusted by the industry and by the public to enhance emissions monitoring and estimation. Build on your natural strengths and expertise to promote adequate measurement and reporting.

Do any pre-existing policies explicitly address methane emissions? Beyond this, are there existing policies that indirectly affect methane emissions?

Chances are, whether intentional or not, you will have policies in place that influence methane emissions from oil and gas producers in your jurisdiction. Sometimes, these policies directly apply to methane combustion or release of natural gas to the atmosphere, even if they were not implemented for climate reasons. For instance, Nigeria requires a permit for flaring and enables companies investing in equipment to capture and deliver associated gas to write these off as tax-deductible capital expenses. The Russian Federation (hereafter, “Russia”) assesses a fee for flared gas, but allows deduction for investment in associated gas infrastructure. The United States has imposed air quality standards that apply to volatile organic compounds (VOCs) and methane emissions from oil and gas facilities.

In many other instances, pre‑existing policies will not mention methane explicitly but nonetheless create opportunities for (or obstacles to) methane abatement. For instance, a country with a carbon tax may take inspiration from Norway and extend that tax to cover methane emissions from the oil and gas sector.

Policies indirectly affecting methane emissions can be more difficult to identify, but they are worth the search. Economic regulations may enable companies to charge customers for lost gas; production tax credits may incentivise a rush to complete wells and move on, perhaps undercutting the motive to perform low-emissions completions; environmental rules may require emissions monitoring that indicates methane leakage; safety regulations may require venting of methane to the atmosphere before conducting repairs or inspections.

Where an existing policy facilitates abatement, you might consider enhancing it – increasing the stringency, the length of time the requirement is in place or the level of subsidy – or ratcheting up enforcement to ensure more consistent compliance. Where an existing policy has the potential to facilitate abatement, you might consider applying it in new ways to realise that potential. Alternatively, you might leave an existing policy as you found it, but then know to avoid undermining it with any new policy.

Likewise, it may make sense to remove existing policies that create the wrong incentive structure. If an existing policy inhibits abatement, you might remove the policy, or change it so as to achieve the original policy goal without creating a disincentive for action on methane. For instance, when economic regulators enable natural gas utilities to pass the costs of “lost and unaccounted-for gas” on to customers, they may disincentivise pipeline maintenance. Some utility commissions in the United States have recognised this incentive problem and capped the amount of lost and unaccounted-for gas that can be included in customer rates.##4##

Step 2: Characterise the nature of your industry

How might the particular characteristics of the industry in your jurisdiction affect the types of policies you put in place?

In this step, you will continue the exercise of gathering information about your local context, focusing here on the nature of your industry. As you consider the questions outlined in this section, you should keep in mind the three categories of barriers to reducing methane emissions: information, infrastructure and investment incentives. Understanding the nature and shape of your industry will help you to identify where policy intervention can be most effective at addressing these barriers within companies. This may suggest particular regulatory strategies and focal points.

Analysis may also suggest which government bodies and personnel need to be involved in methane abatement policy making (see the last section), and help you predict where your “problem” sources of methane might lie (see the next section).

Industry segments

How much of the value chain is represented in-country?

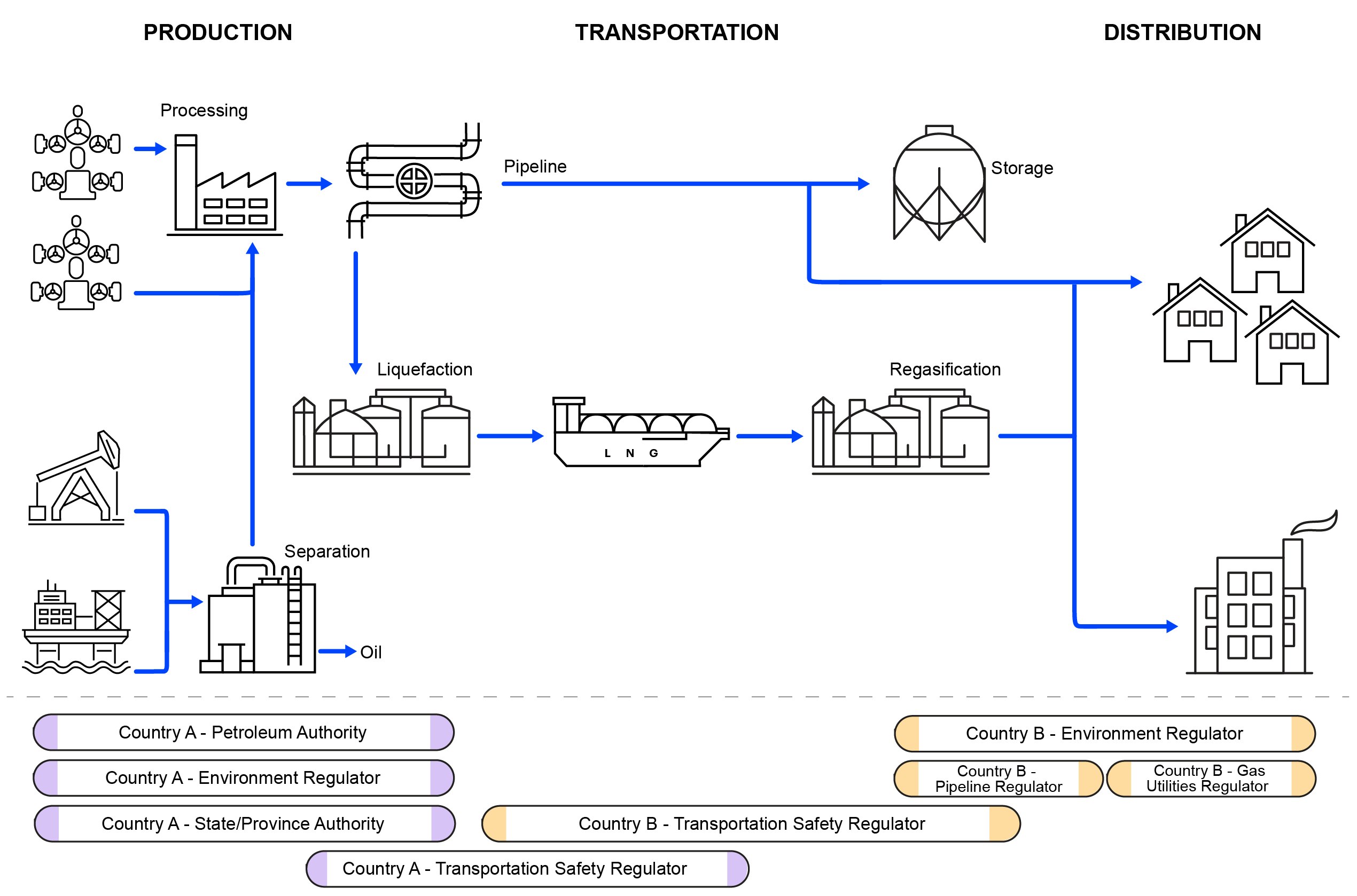

The natural gas value chain extends from the point of production to the final consumer. Along the way, natural gas is gathered, processed, transported by pipeline (or in its compressed or liquefied form, by truck or ship), stored, distributed and used in industrial, residential, electrical power and transportation applications. When natural gas is used for electricity production, this chain of industry segments is often described as “well to burner tip”. Each industry segment has a different set of methane emissions profiles, challenges and abatement opportunities.

Some countries will have all industry segments represented within their borders, such as the United States, Canada, Mexico and Russia. Others will have just a subset, as will be described below. It is important to identify which part of the value chain your country will regulate, to match the right policies to the particular challenges posed by each segment. Generally speaking, countries with all industry segments represented within their borders may have more policy levers at their disposal to target methane leakage and venting across the value chain.

Oil and gas value chain

|

Question |

Relevance |

Examples |

|---|---|---|

|

How much of the oil and natural gas value chain is represented in-country? |

Countries that have most or all industry segments represented have more policy levers at their disposal. They can regulate production, transportation and consumption of the commodity in a way that supports methane abatement. |

The United States, Canada and Russia have all industry segments represented within their borders, and a robust natural gas market (although access to market issues remain for associated gas across all three jurisdictions). |

|

In Russia, the industry is entirely regulated by the national government, while in Canada and the United States, different segments are regulated by national or subnational levels of government. |

Diagram of natural gas value chain and indicative division of governmental authorities

Open

{kind=link}

Sometimes, governmental jurisdiction may change by industry segment. In Australia and Colombia, the national pipeline regulator oversees transmission and distribution pipelines, while in the United States, states (such as Texas) separately regulate intrastate distribution gas lines while a federal agency regulates interstate pipelines.

Are there robust domestic markets for natural gas?

Many countries or regions that produce natural gas as a co‑product of oil or coal production may not have midstream or downstream natural gas industry segments because they lack domestic markets for natural gas. Without adequate pipeline and processing capacity, or end-use demand, these regions and countries may find it difficult to require or incentivise the capture of natural gas at production facilities. For this reason, countries such as Nigeria and Brazil are working to develop a midstream market and to drive domestic demand of natural gas, notably to electrify rural communities and support industrial growth. If your country faces this situation, policy will have to overcome both the infrastructure and investment incentive barriers to methane abatement.

Gas markets

|

Question |

Relevance |

Examples |

|---|---|---|

|

Are there robust domestic markets for natural gas? |

Countries that do not have domestic markets for natural gas will need to find export markets, to induce development of the infrastructure necessary to bring associated gas to market. |

Nigeria and Brazil have worked to develop a midstream natural gas market and drive domestic demand of natural gas, to make use of otherwise vented or reinjected associated natural gas (reinjection being a better outcome than venting, of course). |

Is your country a natural gas net importer or exporter?

Countries without all industry segments represented have more limited policy targets. For instance, the European Union has very little oil and natural gas production, meaning that a policy that directly regulates upstream methane emissions would have little effect. By contrast, nearly 44% of the world’s natural gas imports come to the European Union. Therefore, policies that aim to reduce consumption of natural gas, or to ensure that all gas consumed comply with certain standards, would be a more effective strategy for this jurisdiction. Procurement standards are emerging as a powerful policy tool. Large consumers of natural gas may demand a “low-leakage” supply chain as a basis for eligibility to bid or as a performance condition in a contract. Importing countries may impose similar methane intensity standards at the point of import, though there may be some legal risk. Importantly, you should consult with the trade authorities in your government, and you will need to establish a mechanism to judge the upstream emissions profiles of importers. Such a mechanism does not currently exist anywhere in the world (although the European Commission’s Methane Strategy contemplates eventually establishing one). As a first step, it may be more efficient and effective to work with your top importing countries, to seek assurances of their emissions profile or to encourage an effective regulatory regime upon their producing sources. Net exporting countries could anticipate these new rules with domestic methane abatement policies likely to meet importer standards, or gain a competitive edge if their cleaner product is subject to a small carbon border adjustment, or gives the exporter a marketing edge in climate-conscious markets.

International gas trade

|

Question |

Relevance |

Examples |

|---|---|---|

|

Is your country a natural gas net importer or exporter? |

Net importers of natural gas do not have direct regulatory authority over upstream activities beyond their borders and must leverage their consumer power to induce methane abatement outside of their borders. |

Nearly 44% of the world’s natural gas imports are delivered to the European Union. Methane abatement policies must be tied to consumption, or seek to apply methane-intensity standards at the point of import. |

|

Net exporters of natural gas may be driven to reduce methane emissions because of climate policies in the markets where they sell. Alternatively, export countries could be proactive in abating methane leakage, to achieve climate commitments and to distinguish their product in the world market. |

Countries that export natural gas to Europe and East Asia are tracking the climate policies of those countries and large industrial consumers in those countries to anticipate the methane abatement that may be demanded or preferred in these markets. |

Description of industry participants

One of the most important aspects of your industry is the makeup of its participants. A country dominated by one vertically integrated, state-owned enterprise working with a handful of other multinational corporations may call for a different regulatory regime than a segmented and heterogeneous industry landscape. Most notably, where regulatory requirements are implemented through contractual or concession terms, this may be the primary vehicle for imposing methane reduction requirements.

Is the industry vertically integrated or segmented?

The last section discussed the parts of the value chain represented in your country. Even where the full value chain is represented domestically, your natural gas industry may be vertically integrated – meaning the same firm controls natural gas across the value chain – or broken out by segment.##5##

Where the same firm controls most or the entire natural gas industry (or those segments existing in a country), it is more likely that regulation will be consolidated at the national level or within a single agency. This can create regulatory efficiencies. Vertical integration also facilitates flexible regulatory strategies such as industry-wide emissions goals, which enable a firm to find the most cost-effective reductions across the value chain. On the other hand, there are drawbacks to a single firm working with a single regulator. If either entity is resistant to change, or if the close working relationship leads to regulatory capture, regulation may be difficult to introduce. In addition, regulation of a few large actors can create transparency concerns. For instance, in jurisdictions with a few large actors, regulators are more able to negotiate specific terms in individual permits. While this enables tailored regulation, these permits are often not disclosed to the public. In Norway and Nigeria, therefore, it can be challenging to determine the stringency of requirements – or the leeway a permit writer has to weaken or waive requirements. Publication of the permits, as is done in Brazil, might be a way to enable better tracking and accountability.

A more segmented industry will by definition involve more industry actors. Regulation of these actors can be more decentralised and more complex. In this context, methane abatement policies are more likely to focus on a single segment and emanate from different agencies. For instance, in the United States, at least four federal agencies – the Department of Transportation, the Federal Energy Regulatory Commission, the Department of the Interior and the Environmental Protection Agency (EPA) – may regulate different upstream and midstream segments. In turn, the EPA issues distinct rules for each industry segment for stationary sources. Additionally, subnational and local governments regulate methane from wells, gathering lines, and distribution pipelines, often through a public safety, economic or consumer lens. (By contrast, offshore of the United States, the federal government owns the resource, is the sole regulator and oversees activities dominated by vertically integrated firms.) While decentralised operations and regulation may be less efficient, it may also allow for more experimentation in different jurisdictions and across companies, and lead to more policy innovation.

A single company or entity may dominate each segment. If so, within that segment, you may have the same close relationship as a regulator would have with a vertically integrated utility across the value chain. For instance, in Russia, different state-owned firms have strong positions in different aspects of production, refining and pipeline transportation of oil and natural gas. At the other end of the spectrum, segments of the US industry, including upstream oil and gas production, are quite competitive and involve many actors of varying sizes and levels of sophistication. This can foster opposition to regulation out of a fear of the excessive burden that might be placed on smaller actors. At the same time, a more opportunistic regulatory approach may work better in this context – the regulator can search for willing partners from among the firms to pilot new abatement technologies, inventory emissions or propose methane reduction standards. This opportunistic context does not require a competitive market such as the one in the United States; even having one or two multinational corporations working with and alongside a national company might spur these firms to take action.

Industry structure

|

Question |

Relevance |

Examples |

|---|---|---|

|

In the industry in your country vertically integrated or segmented? |

Countries with vertically integrated industry may centralise regulation of all methane-emitting activities. Moreover, vertically integrated firms may achieve economies of scale in methane abatement. That said, it may be harder to move a single regulator or industry actor that is resistant to change. |

Brazil, Colombia, Argentina, Russia and the United States (offshore) have an industry dominated by vertically integrated firms. |

|

Countries where the natural gas industry is broken out by segment may have more industry players to regulate, fewer cross-sector strategies to deploy, and more regulatory actors involved. But this context can also create opportunities for experimentation. |

The United States (onshore) has a highly segmented, diverse industry. |

Are the firms involved private or state-owned?

The companies operating in your jurisdiction may be privately held or state-owned – often known as national oil companies (NOCs). In many countries where oil or natural gas production is dominated by state-owned enterprises, government agencies do not have legal authority to regulate these activities (although there may be political or budgetary oversight). In a departure from this standard practice, some countries have begun directly regulating NOCs. For instance, Mexico recognised the need to create a separate regulatory authority over Pemex, the state-owned oil company, to tackle methane pollution and other sustainability issues.

Although state-owned enterprises may be more aligned with the public policy goals of your government’s leadership, easing implementation, they may also be viewed in the legal structure as co‑regulators or as self-regulated entities, which could make it more difficult for government agencies to impose methane standards. Alternatively, they may be legally bound to meet certain performance metrics that do not align with the goal of methane abatement. In these cases, it will be important for government agencies and NOCs to work closely together, and to identify other policies that might interfere with methane reduction activities.

In some countries with state-owned oil and gas enterprises, including Indonesia, Nigeria and Kazakhstan, oil and natural gas production can occur through joint ventures with, or concessions to, private firms. The state-owned enterprise may enter into contracts with those private firms, as a partner as a stand-in for the regulator (as in pre-2004 contracts in Colombia).##6##Including methane abatement provisions directly in these standard contracts may be an effective way to impose methane limits on those private partners.

If the private companies have operations in other countries, check to see if those other countries have implemented methane abatement policies, or have expressed interest in doing so. A company that has to comply with methane regulations elsewhere may be more willing to work co‑operatively with you to forge similar rules in your jurisdiction.

Industry type

|

Question |

Relevance |

Examples |

|---|---|---|

|

Are state-owned firms involved along the energy value chain? |

Countries with state-owned companies may or may not directly regulate those companies. Where they do, attention must be paid to the different motivations of state-owned firms to ensure methane abatement policies will be effective. |

In 2014, Mexico created a new regulator to oversee worker safety and environmental protection in the oil and gas sector, for the existing state-owned enterprise and private firms beginning to participate. |

|

Where both state-owned companies and private companies operate in a country, policies may apply differently (and in some cases, the state-owned company may be in the position to regulate the private entity). |

Indonesia, Nigeria, Kazakhstan and Colombia allow for joint ventures or concessions for private companies to develop resources with or alongside state-owned firms. |

|

|

Countries with exclusively private companies operating in this space will subject those firms to regulation. |

The United States and Canada have only private firms operating in the oil and gas sector. |

Resource targeted

Oil and natural gas production can both result in methane emissions.##6## Since natural gas is primarily composed of methane, the entire natural gas value chain is a potential source of methane emissions. By contrast, methane is processed out of oil, so methane ceases to be an issue as the product moves through to the midstream market. Therefore, methane abatement policies as applied to oil need to focus only on upstream activities up to and including refining.

Is the natural gas a by-product of oil production?

Methane abatement becomes more challenging when natural gas is not targeted as a resource. If your jurisdiction has a complete natural gas value chain, the requisite infrastructure and consumer demand should be there to incentivise the capture of methane for sale. This makes it more likely that the firms in your jurisdiction are already taking some voluntary measures to reduce methane venting or leakage and are more likely to be productive partners in any future regulatory venture.##7## However, if upstream producers are focused on oil production and lack the gathering infrastructure or markets to deliver natural gas, it becomes more costly and more difficult to make the case for methane capture. Finally, as already mentioned, how your legal system views “associated” gas may have large implications for your abatement policies. If treatment of this gas as a waste incentivises its release to the atmosphere, or makes it unclear who owns the associated gas, changing those policies may be an important threshold step to take to realise your methane emissions reduction goals.

What is the geochemistry of your natural gas?

More detailed inquiries into the type of natural gas that is produced or transported through infrastructure, including its geochemistry, may be useful. For instance, if the natural gas in your jurisdiction is particularly corrosive, a more robust leak detection and repair regime may be necessary. If produced gas is sour (i.e. contains significant amounts of hydrogen sulphide), then detection measures are probably already in place due to safety concerns and you can build onto these requirements.

Where is your natural gas production located?

The location of natural gas infrastructure may also suggest policies of different types and frequencies. Offshore oil and gas production wells generally take more abuse from the elements than onshore wells; valves on pipelines that experience extreme temperatures will be under more stress than pipelines through temperate zones. These remote facilities may be visited less often for inspection; use of remote sensing and continuous emissions monitoring may be more critical in these locations. Offshore facilities may also be far removed from natural gas gathering lines; here, gas reinjection might be encouraged as a climate policy as well as to stimulate offshore oil production. As we learn more about methane emissions profiles of different activities and types of infrastructure, these details may prove to be even more useful in designing relevant emissions standards.

State of energy development

Finally, it helps to understand your industry’s stage of energy development. This inquiry will be informative in two respects. First, it may indicate how much institutional expertise you have in your state-owned firms and agencies, which could be tapped for methane abatement efforts. Second, you may use different policies to address new infrastructure than to retrofit or replace existing facilities.

How extensive is your existing infrastructure? How old is it?

Where lower-emitting equipment is readily available (for instance, low-bleed and no-bleed valve controllers), regulators can dictate the use of this equipment for new construction. More challenging, by contrast, is the application of methane abatement standards to existing infrastructure. Payback times for methane abatement investments may extend beyond the remaining useful life of certain equipment. Retrofitting old equipment may be more difficult – and more expensive – than building a low-emission facility from a greenfield. Mapping existing infrastructure can be a good starting point for emissions inventories, while also suggesting where regulatory efforts should be focused. For instance, your regulatory framework might aim to replace ageing infrastructure over time, and in the meantime, inspect it more frequently for leaks. Some jurisdictions might contemplate phased regulation, applying methane abatement standards to new infrastructure and then setting deadlines further into the future for the replacement of older equipment. Establishing requirements to tag, meter and report emissions of existing infrastructure can also lead companies to voluntarily replace sources that represent a disproportionate share of their overall emissions.

If your jurisdiction has a long history of energy development, you may need a regulatory strategy to address methane emissions from abandoned wells. Pennsylvania, where the first American oil well was drilled in 1859, could have as many as 750 000 “orphan” wells, many of which could be releasing methane. Across the globe there are millions of abandoned wells, a number expected to increase in 2020 due to the Covid-19 pandemic and in the future once the world has passed peak demand.

The US-based Clean Air Task Force has created an online tool to help identify the abatement potential of your existing infrastructure; other resources may be available as well.

What are your country’s future resource development plans?

Today, your country may produce natural gas from onshore wells, but it may be eyeing a new offshore oilfield. Your industry may be focused on oil production, while you want to develop a domestic midstream and downstream gas industry to market associated gas. Look beyond today’s development and anticipate where the country may be headed when developing methane abatement policies. The IEA Methane Tracker is a good starting point to establish your past, current and future energy development patterns. The IEA publishes reported numbers on energy production and consumption for each country.

As momentum builds for global efforts to reduce emissions, many countries are also looking to scale up the use of low-carbon fuels, including biogases and low-carbon hydrogen. Depending on the production routes involved, these may also involve the risk of methane leaks to the atmosphere. The need for a robust approach to methane abatement can extend throughout energy transitions and beyond.

Step 3: Develop an emissions profile

Estimated level of emissions

More likely than not, you will need to develop an initial estimate of your emissions to use a reference point in setting your goal and tracking your progress. Moreover, by studying data about methane emissions from different sources and activities, going forward you can track general trends and adjust your policies accordingly.

Does your country already have estimates of oil and gas sector methane emissions?

As a member of the United Nations Framework Convention on Climate Change (UNFCCC), your country may compile greenhouse gas inventories. To support this or other regulatory programmes, your jurisdiction may already have reporting requirements in place, for some or all sources of methane. Canada and the United States are good examples of countries with national inventories that target methane emissions. Over time both jurisdictions have worked to estimate this pollution at a relatively granular level.

Initially, available information, even under a mandatory reporting regime, may be quite limited; that is expected and can be managed. As you learn more about methane emissions in your jurisdiction, you can amend inventory reporting rules to collect better information – and amend abatement policies to match reality on the ground.

How might you generate in-country emissions estimates?

As long as some of the sources are reporting, you may be able to derive country-specific emissions factors for a set of sources or activities. In addition, guidance created by the Intergovernmental Panel on Climate Change (IPCC), initially released in 2006 and refined in 2019, includes more generic emissions factors that could be applied to your industry. The IPCC’s fugitive emissions estimations document is particularly relevant to calculations of a methane baseline for abatement policies.

The IEA Methane Tracker offers country-by-country methane emissions estimates, which may inform your inventory. The tracker estimates methane emissions from the oil and natural gas value chain, using generic emissions factors (often those generated for North America). These are a good starting point; however, development of locally derived emissions factors should ultimately be the goal. In addition, companies in your jurisdiction may already be tracking their methane emissions for corporate governance purposes and might be willing to share what they have learned. If no such information already exists, you can look to emissions from similar installations elsewhere to get a sense for this information. Moreover, as satellites begin producing more publicly available data on methane emissions, you may be able to use those data to confirm and reconcile estimates you have developed based on an inventory of emissions factors.##9## See the Monitoring section of the Toolkit for more information on this.

To use emissions factors effectively, you will need to estimate the number of pieces of a particular type of equipment being used in your jurisdiction, or the number of times an activity (i.e. completing or cleaning out a well) takes place. These “activity factors” are often the most overlooked source of data. Activity factors help you estimate the magnitude of your emissions. They also suggest the policies that might be most successful to address your particular sources of methane by cataloguing the most prevalent activities and types of equipment represented in your industry.

How can you gather information about equipment and components used at a typical site?

If methane pollution is emitted by a relatively small number of somewhat homogenous large sources, run by large companies with adequate technical expertise and resources, you may be able to require more robust remote sensing and emissions tracking. Norway’s offshore oil and natural gas industry fits this model and indeed, that country has worked closely with the industry to craft highly granular emissions factors based on emissions monitoring and testing protocols on its offshore platforms. As a result, the Norwegian industry has published a number of highly useful emissions guidelines and handbooks.

Short of this, there are other ways to estimate activity information. You can collect initial numbers from companies operating in your jurisdiction as part of your national emissions inventory or through a data collection exercise. You might also refer to inventories done by countries with similar industry vintage and structure.

Sometimes, these data will have been collected by another agency. For instance, a government worker safety programme might track miles of pipeline and number of accidents along those pipelines. While the information was not collected with methane in mind, the miles of pipelines figure could be used to generate emissions estimates for pipelines, while accident data could point to large emissions events and inform root cause analyses to prevent future accidents.

If your country has a long history of energy development, you may want to embark on a survey to estimate the number and location of abandoned facilities that are emitting methane. Your jurisdiction may also have to think of creative ways to finance dismantling or shutting in these facilities, either because the industry is dominated by state-owned enterprises, or because, as in the United States, many of the private entities that operated these abandoned facilities no longer exist.

At this stage, your emissions profile will be incomplete and based on unconfirmed numbers. Over time, it will be important to build better data collection and reporting into your methane abatement regulatory regime. “Bottom up” emissions estimates that are based on generic emissions factors are useful as a starting point, but better data based on robust measurement – and over time, “top down” aerial surveys and satellites – can lead to more effective regulatory actions and better confidence in the outcome of specific emissions reduction efforts.

As regulators and companies alike become more adept at emissions estimations (and measurement technologies improve), you may find that your initial baseline overestimated some emissions and underestimated others. That is to be expected. You can maintain that initial baseline year but adjust total emissions from that year retroactively, to reflect the latest and best understanding of your emissions profile. You might also consider using error bands and discount factors to account for the uncertainty in the estimates.

In any case, having a sense of the scope and nature of the problem at the outset will help you build the case for action, show progress once your policy is implemented and suggest future adjustments of your policy to improve emissions outcomes. You need not and should not wait for a perfect dataset to act to abate methane.

Problem sources and abatement solutions

With the emissions information you now have, and by communicating with companies and regulators in other jurisdictions, you can begin to identify your problem sources.

Do you have a plan for identifying your biggest emission sources, over time?

Once again, the IEA Methane Tracker can be a good starting point for identifying large sources. The country-by-country emissions estimates are broken down by industry segment, component and activity. For instance, in Indonesia, the IEA estimates that most methane emissions come from onshore oil and natural gas facilities. Most methane emissions from onshore oil wells are from venting or incomplete flaring, while fugitives play a larger role in the emissions profile of onshore natural gas wells. Within those facilities, the IEA identifies vapour recovery units on tanks, leak detection regimes and replacement of emitting instruments as big potentially mitigating technologies.

Sources of methane emissions, Indonesia

OpenHow will you locate intermittent “super-emitters”?

Knowing the industry segments and type of equipment that dominate your emissions picture is useful, but not the end of the story. A major technical challenge for addressing methane from the oil and gas is the intermittent and variable nature of the emissions. Valves do not fail on a schedule, and when they do, they may deviate widely from an expected emissions rate based on system pressure, climatic variables, contemporaneous failures and other factors. Depending on company work practices, some crews may not complete a well blowdown in one session and instead may leave the well open overnight or until the next shift, producing many times the emissions for the same activity. Different geological formations and even the time of day affects emissions being released from equipment.

As a result, studies have suggested that at any given facility, or across a producing field or region, a small number of sources drive most of the emissions.##10## Much of this research has been done in North America, though early findings in other regions suggest similar patterns. In 2006, the US National Gas Machinery Laboratory found that the top ten leaking components in a facility containing thousands of potentially leaking components contributed 29-87% of overall emissions over time. A 2015 paper reported that in the Barnett shale gas-producing region of Texas, 10% of measured facilities drove 90% of emissions. These data also suggest that across-the-board command-and-control regulatory requirements may not be the most cost-effective way to address the largest sources.

In addition, “super-emitters” sometimes are the result of highly unpredictable process failures and accidents, from a heavily leaking compressor station in Turkmenistan to a failed natural gas storage well near Los Angeles, California. These events create a great amount of uncertainty in emissions estimates. Fortunately, new developments in satellite data acquisition and processing are increasingly providing ways to identify these type of sources. Companies such as Kayrros and GHGSat offer surveillance services that detect, quantify and can attribute emissions to oil and gas assets based on local information and satellite imagery resolution. Recently the IEA World Energy Outlook included global maps of methane hotspots associated with the energy sector, and GHGSat published an interactive global map of methane emissions showing areas with high concentrations of methane in the atmosphere that might be linked to super-emitting sources.

The goal should not be to try to have a perfect emissions set, but to collect enough initial data and then monitor over time sufficiently to characterise and anticipate your problem sources. Sometimes, by reviewing data, you might find surprisingly large sources of emissions – venting a pipeline before making repairs, perhaps, or forgetting to close a hatch on a collection tank – that require a tailored policy. Similarly, if other jurisdictions have reported that a particular activity generates a lot of emissions, but you do not yet have that data, you could design a policy that gives companies an option to measure emissions or control the source. That will give you a better idea of the magnitude of emissions from those sources, while beginning to clean some of them up. California took precisely this approach with liquids unloading. For sources that may become super-emitters based on data patterns, installation of remote sensors may be a good way to locate big emissions as they occur – setting up the ability to address them quickly.

Technological solutions

The final set of considerations that provide the basis for policy development relate to the available technologies and abatement strategies that match your regulatory, industry and emissions context. Where successful technologies and strategies have been identified, your policy could require their use or set performance standards that can be met through their adoption. For instance, once companies began implementing “reduced emissions completion” techniques at oil and gas wells in the United States, and established their feasibility and cost-effectiveness, the US Environmental Protection Agency required their use at all new gas wells and new oil wells. Where a technology is not yet available, a government might invest in research and development efforts or lead voluntary abatement programmes with the industry to find new mitigation strategies. Over time, regulators should monitor developments in abatement technologies to ensure that regulatory requirements do not inadvertently lock in old technologies and prevent uptake of new options.

The IEA Methane Tracker includes a list of existing abatement technologies. These are presented, on a global and country-by-country basis, along a continuum from least to most expensive per million British thermal units of methane avoidance. The chart also demonstrates at what point capturing and selling the natural gas, at current prices, pays for abatement. The Methane Guiding Principles initiative has published best practice guides that provide a summary of current known mitigation options, costs and available technologies covering leak detection, venting, pneumatic devices and other topics. These resources are a good starting point for identifying the most cost-effective interventions that policy might promote.

Some technologies relevant to methane abatement do not directly reduce emissions but help to find (and sometimes, measure) methane releases. Given the intermittent and stochastic nature of methane emissions, detection and measurement technologies are critical to tackling this pollution challenge. In fact, many existing methane abatement policies, including those in Mexico and Canada, include a leak detection and repair (LDAR) regime, directing companies to inspect and repair leaking equipment on regular intervals. In recent years, technological advances have enhanced detection and improved measurement precision and accuracy, while lowering costs. For more information, please refer to the improving methane data section of the IEA Methane Tracker.

Marginal abatement cost curve, Indonesia

OpenStep 4: Build regulatory capacity

After working through Steps 1, 2 and 3, you should have a good understanding of different characteristics of your local context that may inform your regulatory decision-making, including your legal and regulatory context, the nature of your oil and gas industry, and your jurisdiction’s emissions profile. With a firm grip on your jurisdiction’s setting, you are ready to start the regulatory development phase. The steps in this phase—Steps 4 through 8—will walk you through actually designing and drafting your regulatory proposal, taking care to enhance your institutional capacity and engage with internal and external stakeholders.

Do you have the institutional resources and expertise you need to design and implement your proposed regulation?

A good way to start is by considering your agency’s capacity, and how it might be most effectively deployed in the regulation of methane emissions from the energy sector. Then, depending on the results of your assessment, you will need to develop a plan to increase the institution’s capacity. By capacity, we mean the ability of an agency to understand the methane emissions challenge, to write rules to address that challenge, and to implement and enforce those rules. Capacity, then, encompasses four concepts: political support, trust, expertise and resources.

To the extent you identify deficiencies or areas for improvement, this does not mean that you must wait until you obtain new capacity before developing new policy. No regulator has ever acted under optimal conditions. But by understanding your limitations, you can take targeted steps to reinforce and build capacity, while in the meantime designing regulations that take account of your current situation.

Does your agency have the political support to act?

The level of political support your agency possesses will determine the path and prognosis for action. Institutional power may be a result of the legal framework for your government and where your agency sits in the formal structure. Much of it may also be situational – a relatively obscure agency may grow in power if its leadership or priorities are close to those of the government as a whole, while an agency with a lot of legal authority may nonetheless waste time and resources battling with another agency that has overlapping jurisdiction. If you do not have obvious political independence or support, this doesn’t mean you cannot act, but circumstances may counsel that you start small, perhaps launching pilot projects or co‑operative ventures with energy producers to prove a concept and engender political support for a broader methane abatement programme.

Is your agency trusted by the public or civil society?

Some of your power to act may derive from civil society or the general public. You may also have to earn their trust and convey that you can fairly implement and enforce methane abatement policies. Key stakeholders beyond the regulated community may include members of your own country’s civil society, international organisations working with your government, or oil and gas consumers in other corners of the world. You earn the trust and support of these stakeholders when they view your actions as promoting the public interest and achieving real emissions reductions. To build this trust, you may want to consider policies that feature transparency during rule development and throughout the regulatory process, third-party verification of company activities, and citizen suit or petition powers to encourage enforcement. Maryland addressed community concerns in its recent methane rule-making by requiring companies to publicly post the results of their LDAR inspections and notify the public before conducting blowdown events (controlled releases of methane to relieve system pressure or enable maintenance or repairs to take place without fear of explosion).

What relevant expertise resides in your agency?

It is important to inventory an agency’s expertise as well. Rules written to play to institutional strengths will be more effective, because staff will be better able to monitor and enforce compliance. Of course, an agency or ministry can always develop a particular expertise if you know that’s the regulatory direction you want to head, through targeted hiring, trainings and professional development. For instance, offering certifications in optical gas imaging and other leak detection methods could build confidence and competence on your enforcement or compliance assistance team. In addition, training may be available from professional societies, other companies or external sources. The Society of Petroleum Engineers offers technical workshops, and international organisations and energy companies have joined forces to offer courses as well.##11## An agency might also supplement its expertise by working with outside experts to understand emissions profiles, to write and implement methane abatement policies, forging partnerships with local universities and non‑governmental organisations, working with international organisations and institutions, or co‑ordinating with sister agencies with complementary skill sets.

Even if you may be able to supplement your expertise, your internal capacity and structure remain highly relevant; don’t set rules that agency officials won’t know how to implement or enforce.

Does your agency have sufficient resources to achieve the mission?

Resources will also have enormous impact on the type and complexity of your methane abatement rules. Resources may mean budget, number of enforcement personnel, access to sufficient basic information technology resources, or specialised methane detection technologies.

A lack of resources will not prevent you from acting, but it will suggest less resource-intensive approaches. An agency with tablets for each inspector may build a very different reporting regime than an agency without a modern computer system or consistent internet access. One regime is not necessarily better than another; problems arise from designing reporting or enforcement regimes without a realistic assessment of an agency’s resources. For instance, a small agency with very few personnel may run an effective regime by choosing to rely on remote sensors, third-party testing companies, or self-audits with steep penalties for incomplete or erroneous reporting to enhance enforcement efforts. For example, some countries, including Argentina and Mexico, have built third-party verifiers into their oil and gas regulations, to build confidence in company data without having to rely on government inspectors.

Step 5: Engage stakeholders

Before you take any formal action to regulate methane emissions, you should conduct outreach to the companies that will be subject to the regulation, the communities affected by oil and gas development, other regulators within your government, and other segments of civil society. Outreach at this exploratory stage need not be comprehensive, but it should be strategic. Are there allies to shore up for the road ahead? Are there sceptics whose concerns can be mitigated by sharing data or promising an open process? Are there domestic and international partners whose expertise and information can help you set aggressive but achievable policy goals? Are there interest groups who deserve a heads-up on your plan to regulate? Can you avoid bureaucratic turf battles later by co‑operating with other agencies today?

Engaging the firms active in your jurisdiction will be critical. You may be required or directed by political leadership to discuss your plans with a state-owned firm before proceeding. But as noted throughout this paper, some of the international companies working in your jurisdiction may have made commitments to methane abatement, and can provide information about methane emissions and abatement approaches based on operations in other countries and participation in international methane abatement alliances. Speaking to them and soliciting this information before any policy announcement can help to make your initial pledges appear more feasible and informed. Moreover, by sharing your intention with them before going public, you create an opportunity for firms to ask questions, seek assurances and become more positive about the endeavour by the time you go to press. Providing information to the public about these outreach efforts and soliciting input from other stakeholders, meanwhile, will build trust in the outcome.

Other industry players may also be good targets for outreach. Contractors who conduct many of the activities relevant to methane abatement, technology providers, third-party auditors, insurance firms and financial backers may also have important insights that could help you design a more effective policy.

Some communities or members of civil society may have been pushing you to act; ensure that your process engages with them, acknowledges their leadership and solicits their ongoing support. Other stakeholders – often the regulated community and industrial consumers of oil and gas – will have questions about the impact of policies on the cost of energy; to the extent you are able, you should try to commit to an open process with a transparent assessment of the policy’s costs and benefits.

In the early stages of your policy making, you are more likely to employ discreet methods of reaching out to stakeholders on an individual or small group basis. In some cases, you can pair these quiet meetings with a more public gathering. For instance, you might meet with leaders of a community to discuss your intention to act, and then agree to hold a town hall to listen to community concerns without publicly committing at that event to take action. For communities not well versed on the climate and safety risks posed by nearby methane releases or the steps you envision taking to mitigate those risks, an outreach strategy might include an educational component as well. In addition, you might seek out strategic opportunities for your agency or ministry staff to speak about methane abatement at conferences that key stakeholders might attend; even if staff do not formerly announce plans to regulate, their presence can signal that you find methane abatement an important issue.

You may also want to look further down the road, to predict and nurture the types of stakeholder engagement you will need for your policy-making process. In some jurisdictions, regulators may establish advisory boards that are consulted at particular points. In the United States, “negotiated rule-making” or “reg-neg” (for “regulatory negotiation”) has emerged as an administrative law trend that might also be applicable in the methane abatement context. Where a rule-making will affect only a few regulated entities, an agency may create a committee that fairly represents the different interests at stake and “negotiate” policy language with that committee through a collaborative process. In a less formal variation on the reg-neg approach, some regulators in the United States will conduct an informal information-gathering exercise or direct a diverse group of stakeholders to negotiate a policy solution before the regulators formally take up the issue. The regulators are not necessarily bound by that informal process, but they know the solution reflects consensus.

Stakeholder engagement will take valuable time and resources but these early interactions can help you anticipate opposition, tailor policies and save time later in the process.

Step 6: Define regulatory objectives

Now you can begin to design your regulation. Before you begin drafting, you will need to establish a set of regulatory objectives that you would like to achieve. In essence, this involves answering the question, “What problem are we trying to solve?” From this, you can map backwards to identify the preconditions that are necessary to solve this problem. As you do this, the information you have gathered in the previous steps will help you set objectives tailored to the specific source make-up and emissions of your industry.

There are many different forms a policy goal can take. Some methane abatement policies are based on an economy-wide methane reduction goal, as in California. Others include an industry-wide or sector-specific##12## goal. Mexico’s regulation, meanwhile, requires the setting of facility-specific reduction goals.

Goals may be expressed in tonnes of methane reduced, a percentage reduction below historic emissions or a declining ratio of methane emissions over volume of production. The Global Methane Alliance (established by the UN Environment Programme and the Climate & Clean Air Coalition) has called on countries to set targets of at least 45% reduction from 2005 levels by 2025, and 60-75% by 2030. Targets may also be set in terms of the average “methane intensity” of natural gas, such as that announced by companies in the Oil and Gas Climate Initiative to reduce their methane intensity to “near zero” – defined as between 0.25% and 0.2% – by 2025.

Rather than setting a high-level goal for the whole industry, you may wish to set more granular goals (or sub‑goals) for different segments of the industry – e.g. upstream versus downstream, onshore versus offshore, conventional versus non‑conventional. You may also consider whether to establish separate objectives for emissions from new facilities than for emissions from existing facilities and whether to establish a plan for addressing abandoned wells in your jurisdiction.

Abatement regulations that do not set an explicit volume, percentage or intensity goal (for instance, a rule to replace leaking valves across a system) still implicitly have reduction as a goal even if it is not a specific quantity or rate of emissions. Prescriptive regulations in particular might reflect a bottom-up engineering goal; for instance, to eliminate all high-emitting pneumatic devices from existing oil and gas infrastructure by a date certain. LDAR requirements reflect a desire to identify and address new sources of emissions as they arise.

You might also have a few regulatory objectives that are not focused on emissions reductions. For instance, when designing a greenhouse gas inventory requirement, you might set a goal of having a certain percentage of companies complying with the law within one year. As another example, for a new environmental assessment requirement, you might set a goal of ensuring that all projects approved in the next six months include a specific estimate of the project’s impact on methane emissions. Still another policy objective might be to stimulate the development of an auditing industry, or a midstream gas sector that can purchase associated gas. Some of these objectives might work in concert; for instance, following development of a midstream gas sector, you might set out to eliminate flaring and venting of associated gas.