The Middle East and Global Energy Markets

Key facts on the Strait of Hormuz, oil and gas markets, and the IEA’s response

The IEA is responding to the energy market impacts of the conflict in the Middle East and continues to closely monitor the latest developments.

The disruption to oil and gas flows through the Strait of Hormuz and attacks on energy infrastructure across the region have major implications for energy security and affordability – and for the world economy.

The IEA's Executive Director has said the combined impacts amount to "the greatest threat to global energy security in history." The war in the region that began on 28 February has impeded energy trade flows through the Strait, creating the largest supply disruption in the history of the global oil market. Global gas markets have also been affected, with about 20% of the world's supply of liquefied natural gas (LNG) having moved through the Strait in 2025.

On 11 March, IEA Member countries unanimously agreed to carry out the Agency’s largest-ever release of emergency oil stocks to help address the market disruptions. Read the latest update on the stock release here.

Current market backdrop

Oil and natural gas prices have increased significantly since the war started. In the wake of the largest oil supply disruption in history, Brent futures, the global benchmark for crude prices, were roughly one-third above their pre-conflict levels in late May. Physical crude prices have seen even stronger gains, reflecting acute supply tightness as refiners scramble to replace Middle Eastern cargoes with other supplies available on the market.

Some markets for oil products have also been particularly affected, including those for diesel and jet fuel. And Dutch TTF, the European benchmark for natural gas prices, rose by more than 40% between late February and late May.

With Hormuz tanker traffic still restricted, cumulative oil supply losses from producers in the Middle East now exceed 1 billion barrels, with more than 14 mb/d of oil production shut in.

Saudi Arabia and the United Arab Emirates (UAE) have successfully redirected some exports to terminals loading outside of the Strait. Even so, mounting supply losses from the Strait of Hormuz are depleting global oil inventories at a record pace. Observed global inventories, including oil on water, were drawn down by 250 million barrels over March and April, or by 4 mb/d – underpinned by the historic stock release anounced in March by the IEA. Producers outside of the Middle East have also pushed output higher and lifted exports to record levels in response to the crisis.

Our latest monthly Oil Market Report, published 13 May, has more. It notes that resuming flows through the Strait of Hormuz remains the single most important variable in easing the pressure on energy supplies, prices and the global economy.

Our Maritime Chokepoints Shipping Monitor also shows how flows for oil, gas and other cargoes have evolved since the start of the war, based on ships' automatic identification system (AIS) data:

The Gulf region is a key source of exports of refined oil products to global markets, notably for middle distillates such as diesel and jet fuel. Gulf producers exported 3.3 mb/d of refined oil products and 1.5 mb/d of liquefied petroleum gas (LPG) in 2025. Nearly 3 mb/d of refining capacity in the region has shut due to attacks and a lack of viable export outlets. Refiners outside the region are also curtailing refinery runs due to concerns over feedstock availability.

Globally, markets for middle distillates have been relatively tight compared with those for other products, leaving little flexibility for refineries outside the region to increase their output of diesel and jet fuel to compensate for sustained supply losses.

End users of oil and oil products are curbing consumption in response to higher prices. For now, the steepest losses have been seen in the petrochemical sector, where feedstock availability has become increasingly constrained. Aviation activity is also running well below normal levels, helping to ease some of the pressure on jet fuel prices, which nearly tripled after Middle Eastern exports were cut off.

The war has also disrupted both regional and global gas supply dynamics, reversing a trend of market rebalancing observed during the 2025/26 heating season. The disruption of transit via the Strait of Hormuz has reduced LNG supplies from Qatar and the United Arab Emirates by over 300 million cubic metres per day since 1 March – which translates into a loss of over 2 billion cubic metres (bcm) of gas supply every week.

The Ras Laffan facility in Qatar, which is the largest liquefaction facility in the world, has been offline since it was first attacked on 2 March. Regional gas production is also affected by the shut-in of oil fields, which has cut the output of gas associated with oil production.

Natural gas prices in Asian markets have risen sharply since the start of the war to attract more LNG cargoes, reflecting the region's greater exposure to supply disruptions via the Strait. Higher prices and supply constraints have also prompted demand-side adjustments, including gas rationing in some countries.

The conflict has significantly altered the medium-term global natural gas market outlook. According to our latest quarterly Gas Market Report published in April, damage to LNG liquefaction infrastructure in Qatar is set to reduce projected supply growth, delaying the anticipated global LNG supply wave by at least two years. Short-term supply losses and slower capacity growth could result in a cumulative loss of around 120 bcm of LNG supply between 2026 and 2030. While new liquefaction projects in other regions are expected to offset these losses over time, the impacts of these disruptions could be felt through 2026 and 2027.

Our 2026 Energy Crisis Policy Response Tracker catalogues government actions to curb demand and support consumers in response to the energy market impacts of the conflict, while our new interactive tool shows the reliance of different countries on oil and gas supplies from the Middle East.

IEA’s role and oil stock release

Ensuring energy security has been at the centre of the IEA’s mission since its founding in 1974 following the major oil crisis the year before. A critical aspect of this work has been to help coordinate collective responses to major oil supply disruptions by providing additional oil to the global market on a short-term basis.

Each of the IEA’s 32 Member countries has an obligation to hold oil stocks equivalent to at least 90 days of net oil imports and to be ready to collectively respond to severe supply disruptions affecting the global oil market.

On 11 March, IEA Member countries unanimously agreed to take emergency collective action to respond to the major disruptions in oil markets, making 400 million barrels of emergency oil stocks available – the largest-ever release coordinated by the Agency.

The stock release largely consists of crude oil, while in Europe, the contributions are primarily taking the form of refined oil products. This is being complemented by additional production from countries in the Americas. The latest details are available here.

The coordinated stock release is the sixth in the history of the IEA. Previous collective actions were taken in 1991, 2005, 2011, and twice in 2022.

The IEA continues to assess the energy security implications of the situation in coordination with governments around the world. A new report, Sheltering from Oil Shocks, also outlines demand-side measures that governments, companies and households can take to help ease price pressures on consumers.

And the IEA, International Monetary Fund and World Bank have formed a coordination group to maximise their responses to the energy and economic impacts of the war. They held their first meeting on 13 April.

IEA Director of Energy Markets and Security Keisuke Sadamori puts the release of 400 million barrels of oil from members' emergency stocks in context and answers key questions about the decision and its implementation

Why is the Strait of Hormuz so important?

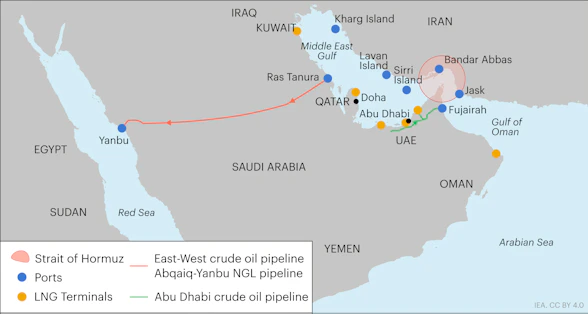

The Strait of Hormuz is a narrow sea passage, separating the Arabian Peninsula and Iran, and connecting the Persian Gulf with the Gulf of Oman and the Arabian Sea. A crucial trade artery, it is the primary export route for oil and natural gas produced by Saudi Arabia, the UAE, Kuwait, Qatar, Iraq, Bahrain and Iran.

Traffic through the Strait has been essentially halted by the conflict, putting pressure on the trade of a wide range of energy products.

Around 25% of the world’s seaborne oil trade transited the Strait in 2025, and options for oil flows to bypass the Strait of Hormuz are limited. Only Saudi Arabia and the UAE have operational crude pipelines that could potentially reroute flows to bypass the Strait, with an estimated 3.5 mb/d to 5.5 mb/d of available capacity. Other countries, including Iran, Iraq, Kuwait, Qatar and Bahrain, rely on the Strait to deliver the vast majority of their oil exports.

Alternative routes

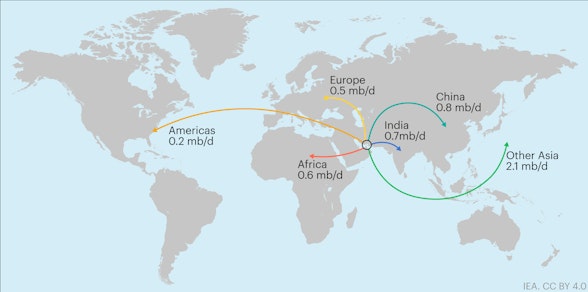

About 80% of oil and oil products transiting the Strait in 2025 was destined for Asia.

In addition, over 110 bcm of LNG passed through the Strait of Hormuz in 2025. About 93% of Qatar’s and 96% of the UAE’s LNG exports transited through the Strait, representing almost one-fifth of global LNG trade. There are no alternative routes to bring these volumes to market.

Most LNG from Qatar and the UAE goes to Asia. In 2025, almost 90% of the total volumes exported via the Strait of Hormuz was destined for the Asian market – accounting for more than a quarter of the region's total LNG imports. Just over 10% went to Europe.

Crude oil exports transiting the strait of Hormuz by destination, 2025

Total does not match sum of adding individual numbers due to destinations not indicated. Source: IEA analysis based on Kpler.

Oil products transiting the strait of Hormuz by destination, 2025

Total does not match sum of adding individual numbers due to destinations not indicated. Source: IEA analysis based on Kpler.

More information about the Strait of Hormuz

Impact on other key commodities

Various other commodities markets have also been affected by disruptions to shipping in the Strait of Hormuz, with implications for energy and beyond.

Fertiliser supply is particularly exposed. More than 30% of global trade of urea moves through the Strait, along with about 20% of trade of ammonia and phosphate. This creates risks for food prices and security. Moreover, disruptions in this sector could have indirect effects on energy markets, since some countries use imported LNG to run domestic fertiliser plants.

Additionally, the Gulf region produces around 8% of the global supply of aluminium, which is used in numerous energy technologies, as well as in construction and manufacturing. About 5 million tonnes of the metal are shipped each year through the Strait from smelters in Bahrain, Qatar, Saudi Arabia and the United Arab Emirates.

Around half of global seaborne sulphur trade also moves through the Strait of Hormuz. Sulphuric acid is used not only to produce fertiliser and chemicals, but also in the refining of petroleum and critical minerals such as copper, nickel and zinc.